|

MINTH GROUP(425)

Analysis¡G

Minth Group primarily engages in the research, development, production, and sales of automotive parts and tooling molds. Its automotive parts business includes products such as metal and decorative strips, plastic components, aluminum parts, and battery casings. The tooling mold business encompasses various molds, gauges, and fixtures used in the development, processing, and production of automotive exterior and body structural components. As a global supplier, the group has established a network for R&D, design, production, and sales in countries including China, the United States, Mexico, Germany, the United Kingdom, Serbia, the Czech Republic, Thailand, Japan, South Korea, France, and Poland.The group is actively exploring new growth avenues and products, focusing on developing a second growth curve. This includes forward-looking investments in autonomous driving and future charging technologies, such as electric vehicle wireless charging systems. Minth has signed a strategic cooperation framework agreement with Siemens of Germany to collaborate on wireless charging projects. Additionally, in response to market and policy trends, the group is venturing into the low-altitude economy and bionic robotics sectors, leveraging its expertise in lean manufacturing from the automotive industry to prepare for large-scale commercialization. In the low-altitude economy sector, Minth focuses on the design, R&D, and production of airframe and rotor systems for low-altitude aircraft. It has completed the design, development, and sample delivery of over 100 components for a client`s first aircraft model. The group is also deepening partnerships with leading Chinese flying car/eVTOL (electric vertical takeoff and landing) manufacturers, actively participating in projects and certification processes for airworthy models.In the bionic robotics sector, Minth focuses on independent R&D of integrated joint designs, motor drive technologies, intelligent electronic skins and masks for robots, wireless charging systems for robots, and limb structural components. It has established strong cooperative relationships with multiple robot clients, engaging in synchronized design and delivering small-batch samples. In March this year, Minth signed a strategic cooperation agreement with Zhiyuan, an intelligent productivity company dedicated to integrating AI and robotics, to advance innovation in AI and humanoid robotics. The partnership will focus on developing ¡§intelligent exterior and electronic skin¡¨ technologies for embodied intelligence and humanoid robotics to enhance tactile and interactive capabilities. They will also collaborate on wireless charging technologies, joint assembly techniques, and optimized lightweight limb structures to improve humanoid robots` motion performance and endurance. Leveraging its advanced manufacturing experience in automotive parts and global network, Minth will work with Zhiyuan to advance secondary development and application of humanoid robots in automotive parts manufacturing, enhancing production efficiency and flexibility through AI-driven industrial automation upgrades for global expansion.(I do not hold the aforementioned stock.)

Strategy¡G

Buy-in Price: $23.00, Target Price: $25.00, Cut Loss Price: $22.00

|

3SBIO(1530)

Analysis¡G

The company is a leading biopharmaceutical enterprise in China, specializing in recombinant proteins, monoclonal antibodies and other biopharmaceuticals, covering fields such as kidney disease, tumors, autoimmune diseases, etc. With nearly 30 years of industrialization experience, the company has built a full industry chain platform from early research and development to commercial production, and actively expanded its contract research and development production (CDMO) business, consolidating its leading position in the industry. In May, the company reached a heavyweight authorization transaction with Pfizer for its self-developed PD-1/VEGF dual antibody SSGJ-707, with a total transaction amount of up to 6.05 billion US dollars, verifying the drug development capability of the company`s self-developed platform. By the end of 2024, the company has 30 products under research and development, and its rich R&D pipeline is expected to gradually enter the stage of realization.

Strategy¡G

Buy-in Price: $24.05, Target Price: $27.50, Cut Loss Price: $22.20

|

|

Xinquan(603179.CH) - Accelerating globalization

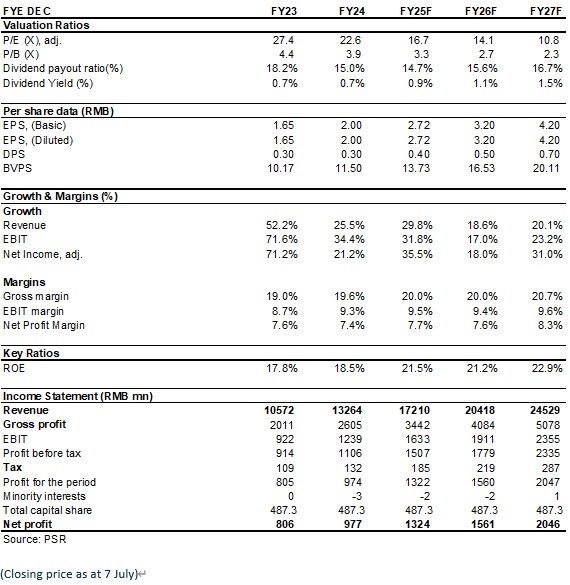

Company ProfileXinquan Co., Ltd., founded in 2001, offers a full range of interior and exterior trim assembly products for both commercial vehicles and passenger vehicles. With industry-leading process competence, cost control capability and technical strength, the Company is capable of simultaneous development with OEMs. In 2024, the Company reported revenue of RMB13,264 million (RMB, the same below), up 25.5% yoy; and net profit attributable to the parent company of RMB977 million, up 21.2% yoy. In Q1 2025, the Company reported total revenue of RMB3.52 billion, up 15.5% yoy; and net profit attributable to the parent company of RMB210 million, up 4.4% yoy. Investment SummaryStable growth in results

In 2024, the Company reported revenue of RMB13,264 million, up 25.5% yoy, mainly driven by the ramp-up from key downstream customers. Net profit attributable to the parent company was RMB977 million, up 21.24% yoy. Sales to the top five customers amounted to RMB9,889 million, up 38.16% yoy. In Q1 2025, the Company recorded revenue of RMB3,519 million, up 15.5% yoy. Among key downstream customers, the global production volumes of Chery, Geely, Li Auto and Tesla in Q1 2025 increased by 17%, 48%, and 16%, and decreased by 13% yoy, respectively. Net profit attributable to the parent company was RMB213 million, up 4.4% yoy. The gross margin was 19.5%, up 2.0 ppts yoy, showing stable performance, while the net profit margin fluctuated in the short term mainly due to: 1) Overseas business being in the capacity ramp-up phase, resulting in a mismatch between personnel expenses and per capita output; 2) An increase in employee welfare expenses during the period. Continuous expansion of product portfolio and enhancement of per-vehicle value

While focusing on interior and exterior trim products such as automotive instrument panel assemblies and bumper assemblies, the Company is actively developing its automotive seat business, continuously enriching and expanding its product portfolio to meet existing customers¡¦ demand for integrated interior and exterior system solutions. In 2024, the interior business achieved steady growth, with revenue from instrument panel assemblies, door panel assemblies, and interior accessories reaching RMB8,348 million, RMB2,167 million, and RMB416 million, up 19.6%, 23.9%, and 12.4% yoy, respectively. The exterior business saw rapid volume growth, with bumper assemblies and exterior accessories generating revenue of RMB474 million and RMB229 million, up 415.0% and 29.0% yoy, respectively. The Company is currently accelerating capacity deployment for its seat business, with planned seat back panel capacities of 400 thousand sets in Mexico and 500 thousand sets in Slovakia. Additionally, the Company recently acquired a 70% equity interest in Anhui Ruiqi to accelerate seat business expansion with Chery Automobile. The new business is expected to further enhance the per-vehicle value contribution and lay a solid foundation for the Company¡¦s long-term development. Accelerated globalization with strong contribution from the North American market

The Company has invested in and established production bases in Malaysia, Mexico, and Slovakia, and set up subsidiaries in the United States and Germany to cultivate the Southeast Asian, North American, and European markets, thereby promoting global expansion. In 2024, the overseas markets made rapid progress, with revenue in Southeast Asia, North America, and Europe all achieving high yoy growth. Among them, the North American market was the standout performer, with revenue reaching RMB700 million, up 89.14% yoy, and a gross margin of 26.37%, up 2.1 ppts yoy. This was mainly driven by the Company¡¦s channel expansion and acquisition of new customers in North America, including a significant increase in orders from internationally renowned electric vehicle brands. Looking ahead to 2025, the production base in Slovakia is expected to commence operations, which will further expand the Company¡¦s channels and customer base in the European market. Investment ThesisXinquan is a promising domestic automotive interior and exterior decoration enterprise. With the continuous expansion of the clients base and production capacity, it is expected to maintain sustained growth. We are optimistic about the long-term development of the Company and expect EPS to be 2.72/3.20/4.20 yuan respectively for 2025/2026/2027, a yoy increase of 35.5%/18.0%/31.0%. We offer a target price of 54.37 yuan, respectively 20/17/12.9 P/E for 2025/2026/2027, and an "Buy" rating. (Closing price as at 7 July)

Risk Factors1) Progress of new production line is below expectations

2) Electric vehicle sales fall short of expectations

3) Macroeconomic downturn affects product demand

4) Sharply rising raw material prices or sharply falling product prices Financial Data

Download PDF version...

| Recommendation on 14-7-2025 | | Recommendation | BUY (Upgrade) | | Price on Recommendation Date | $ 45.270 | | Suggested purchase price | N/A | | Target Price | $ 54.370 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|