|

LIVZON PHARMA(1513)

Analysis¡G

Livzon Pharmaceutical actively responds to China`s ¡§Innovation-Driven Development¡¨ strategy, steadfastly implementing a dual-driven approach of ¡§independent R&D + business development (BD).¡¨ The company focuses on ¡§innovative drugs + high-barrier complex oreparations¡¨ as its core strategy, targeting unmet clinical needs, expanding product lines in its dominant fields, and exploring new accessible areas. The group has established a comprehensive product portfolio in key areas such as gastroenterology, assisted reproduction, and neuropsychiatry, while actively expanding and strengthening its presence in chronic disease areas like metabolic, anti-infective, and cardiovascular diseases to enrich its R&D pipeline and consolidate its platform advantages.In the gastrointestinal field, the group`s innovative potassium-competitive acid blocker (P-CAB) product, JP-1366 tablets, has officially entered Phase III clinical trials, and JP-1366 for injection has been approved for clinical trials, further enhancing the gastrointestinal R&D pipeline. In assisted reproduction, the new indication for triptorelin acetate microspheres for injection¡Xendometriosis¡Xhas been approved for market launch, and recombinant human follitropin Alfa solution for injection was submitted for market approval in late January 2025 and accepted. In the neuropsychiatry field, aripiprazole microspheres for injection, applied for production in 2023, successfully submitted supplementary materials last year and is planned for market approval in the first half of 2025. Injectable aripiprazole has completed bioequivalence (BE) trials, and paliperidone palmitate injection is undergoing BE trials, both planned for market application in 2025. In the autoimmune field, the recombinant anti-human IL-17A/F humanized monoclonal antibody injection has completed Phase III patient enrollment for psoriasis and ankylosing spondylitis indications, with plans for market application in 2025. In the metabolic field, the semaglutide injection for type 2 diabetes has been accepted for market approval, and the weight-loss indication has completed Phase III patient enrollment.In 2024, the group`s overseas sales revenue from drug preparation products grew by 65.98% year-on-year. In the assisted reproduction field, cetrorelix acetate for injection was approved by the U.S. FDA in 2024, marking international recognition of Livzon`s products. The group recently announced the acquisition of a 64.81% stake in Vietnam`s IMP Company, a pharmaceutical company engaged in the R&D, production, and sales of drugs, primarily antibiotics and cardiovascular medications. The group believes this acquisition lays a solid foundation for further expanding its overseas market, supporting its long-term strategy for internationalization and sustainable development in the pharmaceutical sector.As of December 31, 2024, the group`s R&D pipeline includes 45 preparation product projects, with 23 being innovative drugs, high-barrier complex drug preparations, or high-clinical-value products. (I do not hold the aforementioned stock.)

Strategy¡G

Buy-in Price: $30.50, Target Price: $32.50, Cut Loss Price: $29.40

|

ZA ONLINE(6060)

Analysis¡G

On the news front, on July 8, the People`s Bank of China and the Hong Kong Monetary Authority announced multiple Bond Connect enhancement measures at the "Bond Connect Anniversary Forum 2025" in Hong Kong. These include improvements to the Southbound Connect mechanism, with plans to expand eligible mainland investors to four types of non-bank institutions: securities firms, funds, insurers, and wealth management companies. In recent years, insurers have faced persistent low-interest rates and asset scarcity pressures on the investment front. The expansion of Southbound Connect will open new channels for insurance capital to access overseas markets. Against the backdrop of relatively higher interest rates in the US markets, allocating to foreign bonds with diversified currencies and higher yields will help alleviate investment pressures for insurers. Market savings demand remains robust. Simultaneously, under continuous regulatory guidance and insurers` proactive transformation, liability costs are expected to gradually decline, easing spread compression pressures. The 10-year government bond yield recently stabilized around 1.64%. Should long-term rates continue to recover and rise alongside domestic economic recovery, pressure on new fixed-income investment returns for insurers will further ease.

Strategy¡G

Buy-in Price: $18.56, Target Price: $20.42, Cut Loss Price: $16.80

|

|

ENN Energy (2688.HK) - Value-added Business has Great Potential for Growth, Privatization Plan is Progressing Steadily

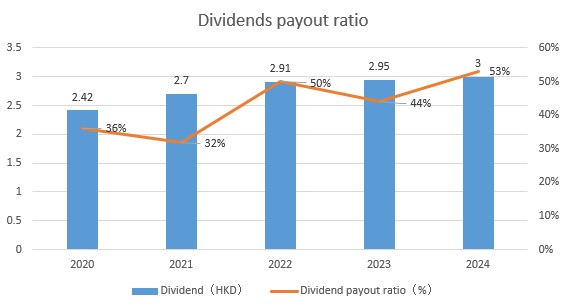

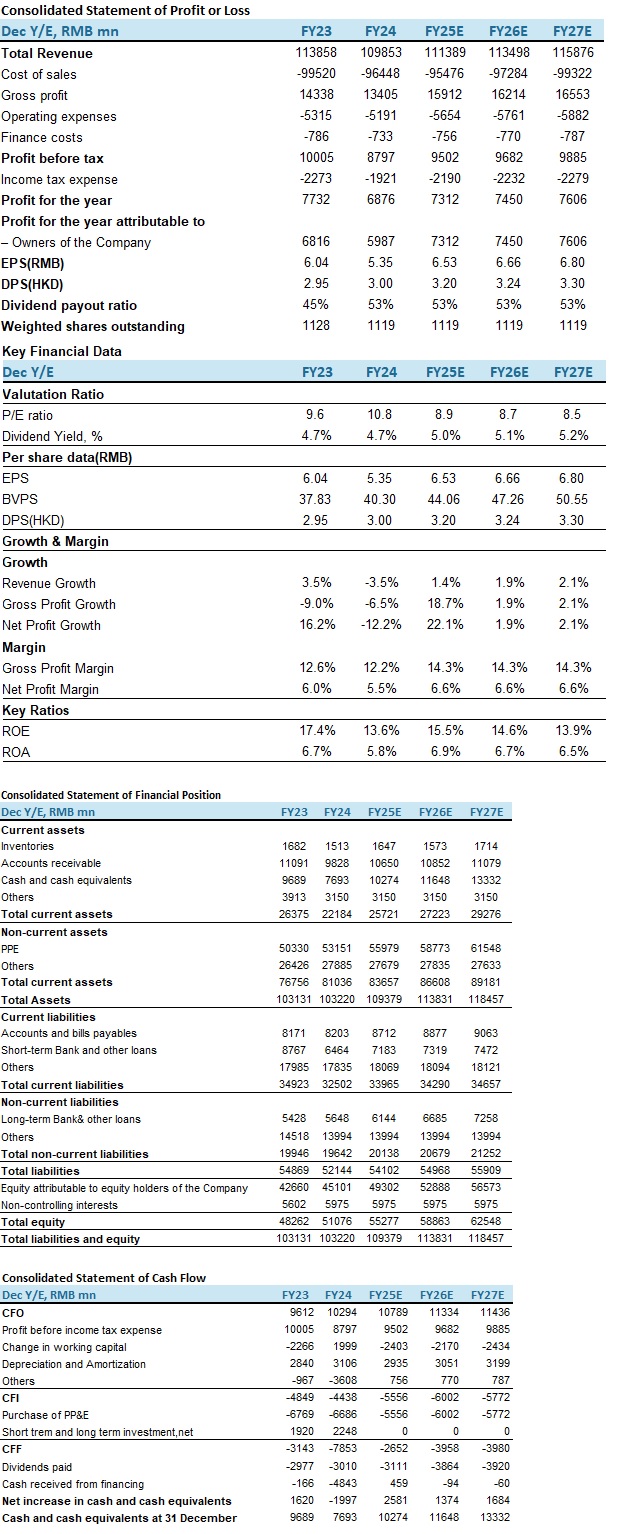

Investment SummaryIn 2024, the company's revenue was 109.85 billion yuan (RMB, the same below) with a year-on-year decrease of 3.5%, mainly due to the company's gas wholesale business focusing more on the domestic market and the engineering installation business being affected by the continuous bottom adjustment of the Chinese real estate market. In terms of business, the revenue of retail gas sale business was 60.75 billion yuan, basically keeping the same compared with the same period of last year; the revenue of integrated energy business was 15.27 billion yuan with a year-on-year increase of 5.2%; the revenue of gas wholesale business was 25.14 billion yuan with a year-on-year decrease of 15.3%; the revenue of engineering installation business was 4.1 billion yuan with a year-on-year decrease of 23.3%; the revenue of value-added business was 4.59 billion yuan with a year-on-year increase of 24.1%, the comprehensive customer unit price increased to 612 yuan/household, the comprehensive customer penetration rate reached 23.9%, and the city gas business has accumulated 31.38 million household users. We believe that this business has a large potential for growth, and it is expected that the revenue growth rate will remain above 20% in 2025. The sales and administrative expense rates were the same as last year, showing that the company has successfully carried out cost control. Thanks to the continuous promotion of the gas price adjustment policy, the profits of associates and joint ventures improved significantly, reaching 912 million yuan with a year-on-year increase of 90.8%. Net profit attributable to the parent company was 5.99 billion yuan with a year-on-year decrease of 12.2%; EPS was 5.35 yuan with a year-on-year decrease of 11.6%. In 2024, the company paid a dividend of HK$3 per share. The company has been paying dividends since 2004, and the dividend amount has been steadily increasing for most of the time, and the shareholder return is attractive.

Resources: Annual Report, PSHK

2025 Q1 Operating ResultsRetail Gas Sale Business

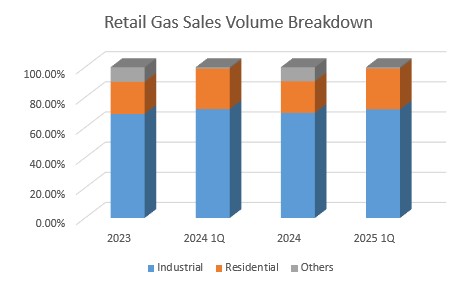

In the first quarter, the company's retail gas volume was 7.26 billion cubic meters with a year-on-year increase of 0.3%, of which the gas sales volume to industrial and commercial users were 5.23 billion cubic meters with a year-on-year increase of 0.1%, and the sales volume for people's livelihood was 1.97 billion cubic meters. The daily gas volume of newly developed industrial and commercial users was 2.5 million cubic meters, and the number of newly developed household users who completed engineering installation was 287,000, all of which remained stable. The company continued to expand its gas volume base. The company actively signed contracts with the three major oil companies to increase gas volume and steadily obtained long-term contract resources from PetroChina to meet customer needs. At the same time, the company continued to optimize the transfer of resources from cooperative manufacturers Accumulate CMP HK$63.4 (Closing price as of 10 Jul) Target 72.86 HKD (+14.9%) COMPANY DATA O/S SHARES (MN): 1131 MARKET CAP (HKD bn): 72.74 52 - WK HI/LO (HKD): 67.4/41.80 SHARE HOLDING PATTERN, % ENN Natural Gas Co., Ltd 34.89% PRICE VS. HSI Source: Phillip Securities (HK) Research KEY FINANCIALS Source: Company reports, Phillip Securities Est.

Resources: Annual Report, PSHK

Integrated Energy Business

As of March 31, 2025, the company has put into operation 367 large-scale integrated energy projects and 73 large-scale projects under construction, with a maximum energy consumption of more than 63.9 billion kWh. The company's cumulative integrated energy sales volume is 10.04 billion kWh with a year-on-year increase of 9.9%. The cumulative grid-connected photovoltaic + under-construction installed capacity reached 1,029 MW; the cumulative grid-connected energy storage + under-construction installed capacity reached 200 MWh. Value-added Business

The penetration rate of existing customers of the value-added business was 3.7%, and the penetration rate of new customers was 49.8%. A total of 12 new projects were put into operation (including 1 urban gas project), with 287,000 new household customers, and the business base continued to expand. Privatization Plan is Progressing SteadilyIn May 2025, the parent company of the company, ENN Natural Gas (600803.SH), announced that the shareholders' meeting had approved by a high vote that ENN Natural Gas intended to privatize ENN Energy by way of an arrangement, and that ENN Natural Gas would be listed on the main board of the Hong Kong Stock Exchange by way of introduction. The evaluation company gave a total consideration of HK$80.00 per share for the privatization plan of ENN Energy, corresponding to a market value of HK$90.5 billion, which still has room for an increase of about 24% compared with the current share price. After the completion of this transaction, the parent company ENN Natural Gas can give full play to its advantages in natural gas resource pools and the storage and transportation capacity of LNG receiving stations, providing effective support for ENN Energy to cope with changes in downstream customer demand. At the same time, ENN Natural Gas can match upstream gas sources with ENN Energy's customer needs, further expand the resource pool, and improve the efficiency of Zhoushan LNG receiving stations, forming a growth model of "internal and external double loops" of coordinated development. Investment ThesisIn Jun,2024, the National Development and Reform Commission released the National Natural Gas Operation Express Report for May 2025. According to the statistics, in May 2025, the apparent consumption of natural gas nationwide was 36.42 billion cubic meters with a year-on-year increase of 2.4%. From January to May 2025, the apparent consumption of natural gas nationwide was 176.89 billion cubic meters with a year-on-year decrease of 1.3%. China Petroleum Economics and Technology Research Institute predicts that China's natural gas demand will continue to grow in the future, and China's natural gas demand will be 610 billion cubic meters in 2035. In 2023, the National Development and Reform Commission issued the "Guiding Opinions on Establishing and Improving the Upstream and Downstream Price Linkage Mechanism for Natural Gas." Under this guidance, different cities have continuously introduced and improved local natural gas upstream and downstream price linkage mechanisms based on the development of the local natural gas industry and economic conditions and have launched or accelerated price linkage reforms. The company has actively followed the reform trend and promoted price adjustments for residents. As of the end of December 2024, the company¡¦s cumulative completion rate for gas price adjustment was approximately 63% of residential gas volume. Since 2025, the old-for-new policy had continued to gain momentum, involving more and more products, and consumers' enthusiasm for participation had been high. The company has continuously consolidated its basic products and services. We believe that as the old-for-new policy continues to gain momentum, the value-added business is expected to become an important business growth engine for the company. We predict that the company's operating income will be 111.39 billion yuan, 113.50 billion yuan and 115.88 billion yuan respectively in 2025-2027. EPS will be 6.53/6.66/6.80 yuan, corresponding to the P/E of 8.9x/8.7x/8.5x. The slight increase in the company's gas sales in the first quarter was mainly due to the warm winter. We believe that the company's gas sales are expected to improve in the winter of 2026. We give the company a target price of HK$72.86, corresponding to a P/E of 10 times in 2026., and we maintain our investment rating of" Accumulate ". (Current price as of Jul 10) Risk Factors1) Supply and demand adjustments

2) Real estate industry downturn

3) Natural gas price fluctuations

4) National policies Financial Data

Current Price as of: 10 Jul 2025

Source: PSHK Est. Download PDF version...

| Recommendation on 15-7-2025 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 63.400 | | Suggested purchase price | N/A | | Target Price | $ 72.860 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|