Overview

Jiangxi Copper (358.HK) is China's largest copper cathode producer and supplier of a full range of copper processing products. The diversified business includes mining development of copper, gold, silver, lead, zinc, tungsten, rhenium, tellurium and other types products. It has established mining bases in China, Peru, Kazakhstan, Afghanistan and other countries, and has four smelting plants in production, five operating mines and eight modern copper processing plants. In addition, the company owns 44.48% of the shares of the listed company Shandong Humon Smelting Co., Ltd.

The company's net profit increased slightly in Q3 yoy

In the first three quarters of 2023 (January to September), the company's total operating revenue was 399.56 billion yuan (RMB, the same as below), a year-on-year increase of 8.53%; the total operating cost was 393.48 billion yuan, a year-on-year increase of 8.83%; operating profit was 6.49 billion Yuan, a year-on-year increase of 4.16%; of which the net profit attributable to shareholders of the parent company was 4.94 billion yuan, a year-on-year increase of 4.54%. Basic earnings per share was 1.43 yuan, a year-on-year increase of 4.54%. The company's total operating income in the third quarter was 132.03 billion yuan, a year-on-year increase of 16.93%; the net profit attributable to shareholders of listed companies after deducting non-recurring gains and losses was 1.44 billion yuan, a year-on-year increase of 30.03%. The performance mainly due to the relatively active domestic policies and demand from real estate and new energy sectors are strong, which keeps copper inventories at a low level and provides certain support for copper prices.

China's copper consumption is expected to grow, which will contribute a mid- to long-term recovery in copper prices

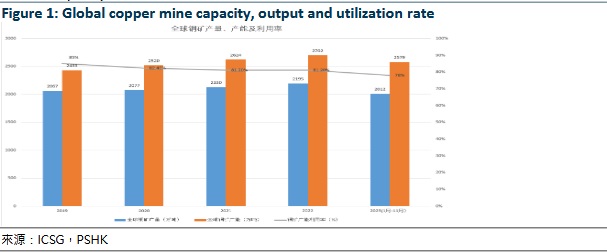

According to relevant data from the International Copper Study Group (ICSG), global copper mine production from January to November 2023 was 20.12 million tonnes, a year-on-year increase of 0.8%, mainly due to the lower base during the epidemic period in last year and the impact of some large-scale copper mine expanding projects in production. Chile copper mine output decreased by 1.5% annually, Indonesia copper mine output decreased by 7.5% annually, and U.S. copper mine output decreased by 9% annually; Peru copper mine output increased by 14% annually, and Congo copper mine output increased by 6% annually. Global copper mine production capacity is 25.79 million tonnes, with a capacity utilization rate of 78%. Looking at the global copper mine production and capacity in the past five years, we can find that copper mine production has been increasing and capacity has been expanding, but the capacity utilization rate has decreased.

From January to November 2023, the global refined copper market was in short supply of 130,000 tonnes, compared with a shortage of 440,000 tonnes in the same period last year. From January to November, global refined copper production increased by 5.5% year-on-year to 24.48 million tonnes. China's refined copper production increased by 13% annually, Chile refined copper production decreased by 2.7% annually, U.S. refined copper production decreased by 10% annually, and India refined copper production decreased by 5% annually. In terms of consumption, global refined copper consumption increased by 4% annually to 24.61 million tonnes, China's consumption increased by 9% annually, and consumption outside China decreased by 2.5% annually. The ICSG report shows that from 2023 to 2027, the annual global copper mine production capacity is expected to grow at an average annual rate of 3.4%, which is significantly faster than the average annual growth rate of 1% during 2017-2020, mainly due to driving of some large-scale copper mine projects in production, especially China's investment in Africa copper mines.

China is still the largest copper consumer country, and the supply of copper has an important impact on China's economy. Currently, China's dependence on foreign copper is about 70%. In the future, China's copper consumption will still be in a growing stage, but China domestic copper supply will be seriously insufficient. According to the ൖth Five-Year Plan for the Development of Raw Materials Industry", China will continue to increase the exploration of scarce mineral resources such as copper to achieve mineral exploration and increase reserves. Supporting the construction of key domestic mines such as copper mines and copper mine construction is included in strategic resource security projects. In the next few years, as the trend of electrification continues to increase, it is believed that the demand for copper will continue to grow, and copper prices are expected to gradually recover.

The company's output of most products increased in the first half of 2023

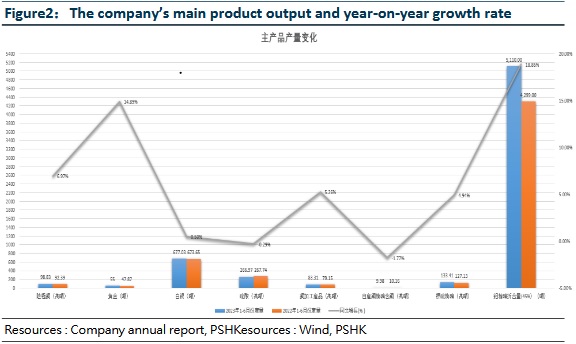

The main product output in the first half of 2023 is shown in Figure 2: cathode copper output was 988,300 tonnes, a year-on-year increase of 6.97%; gold output was 55 tonnes, a year-on-year increase of 14.89%; silver output was 677.03 tonnes, a year-on-year increase of 0.5%; copper processing Product output was 833,100 tonnes, a year-on-year increase of 5.26%.

Through rapid development, the company has formed a certain scale advantage. The group is China's largest copper production base, the largest associated gold and silver production base, and an important sulfur chemical industry base. The company currently owns the largest Dexing copper mine in China and several copper mines in production. As of December 31st, 2022, the company's 100% owned resources are approximately 8.99 million tonnes of copper metal; 275.9 tonnes of gold; 8,626 tonnes of silver; and 210,000 tonnes of molybdenum. Based on the resources controlled by the company and other joint companies, the amount of metal resources calculated based on the company's equity is approximately 4.44 million tonnes of copper and 52 tonnes of gold. Humon Smelting, a controlled subsidiary of the Company and its subsidiaries have 150.38 tonnes of proven gold reserves which have completed reserve registration.

The company has established its industrial chain with core businesses in mining, ore dressing, smelting and processing of gold and copper, as well as sulphuric chemistry and extraction and processing of precious and rare metals. The annual production of copper contained in copper concentrates of the Company is over 200,000 tonnes. Humon Smelting, a controlled subsidiary of the Company, has an annual production capacity of 50 tonnes of gold and 1,000 tonnes of silver and has production capacity of 0.25 million tonnes of electrolytic copper and 1.3 million tonnes of sulphuric acid. The company is currently the largest copper processing manufacturer in the PRC, with over 1,700,000 tonnes of processed copper products produced per year. The production capacity of copper cathode of the company is over 1,700,000 tonnes per year.

Valuation and recommendation

In 2023, Shanghai copper prices will stay near 68,000 for a long time. There are two main reasons, one is the negative impact of the macro environment, and the other is that inventories are always low. In the future, as the main carrier of China's "Double Carbon Action", copper consumption will continue to maintain rapid growth in fields such as photovoltaics, wind power, and new energy electric vehicles. Jinrui Futures research data shows that by 2025 and 2030, China's copper consumption in the three major fields of photovoltaics, wind power and new energy electric vehicles will increase from 1.09 million tonnes in 2022 to 2.09 and 3.98 million tonnes respectively. As many places across the country are currently increasing the construction of large-scale investment projects in the field of new energy, the actual consumption of copper in the field of new energy is likely to maintain a faster growth rate. Looking forward to 2024, in terms of supply and inventory, global copper mine supply will continue to grow. In late January, China has gradually begun to realize the positive inventory accumulation cycle. Some smelting was originally put into production in Q1, but processing profits have declined, coupled with the Red Sea problem which resulted in release of cathode copper output is less than expected, so the inventory accumulation process has slowed down. The supply of cathode copper may be less than expected in the first half of the year, and because the development of the global manufacturing industry is still weak, the recovery of scrap copper supply is also relatively slow. In terms of consumption, the growth rate of real estate is still at a low level and the support is weak. The sales of new energy vehicles are expected to maintain growth, but the growth rate will gradually slow down, which will have a boosting effect on copper consumption. In terms of industry, as mentioned before, the prosperity of the entire manufacturing industry has declined which may be a drag on copper prices. Generally speaking, copper prices may rise slightly in the first half of the year after new construction starts, but the overall situation is still in a state of shock. In the second half of the year, the Federal Reserve may start an interest rate cut cycle, and China will launch more favorable policies. After the macro environment improves, copper prices are expected to start a new round of upward cycle.

The company is committed to accelerating project construction with higher efficiency. Thecopper cathode project with an annual capacity of 180,000 tonnes of JCC Guoxing was successfully put into operation; the fine copper wire expansion project with an annual capacity of 10,000 tonnes of JCC Copper Products commenced coordinated commissioning in late June; the landmark sub-projects of phase III of the extension project of Wushan Copper Mine, such as 1,000-metre main shaft and auxiliary shaft were completed three months ahead of schedule; the 5,000 tonnes/day open pit project of Yinshan Mining completed all preparation works for comprehensive commencement of construction. In addition, the company has also achieved certain results in technological innovation. The ¡§diamond-copper¡¨ product, a high-end chip cooling material developed by the Company, delivered outstanding performance in the trial mass application and had a great appeal to target customers, and the Company will seek cooperation to advance commercialisation in the future. The 6N high-purity copper, the raw material to break high-tech stranglehold in the fields of high-end electronic manufacturing and aviation, completed the midpoint testing research. The heat-proof and anti-corrosion 4N rhenium powder for use in alloys was tried out by high new technology enterprises and was highly recognised in the market. The high-performance oxygen-free copper rods for use in new energy vehicles achieved low-cost and large-scale production and sales. In addition, the company paid attention to energy conservation and emission reduction, the company recorded a period-on-period decrease of 1.39% in total energy consumption and an overall decline of about 18,000,000 kWh in purchased electricity in the first half of the year. And the company introduced new energy electric heavy-duty dump trucks in mines to apply new energy scenarios for the first time.

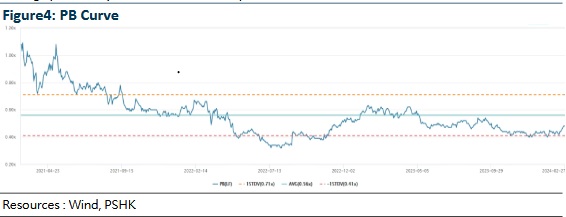

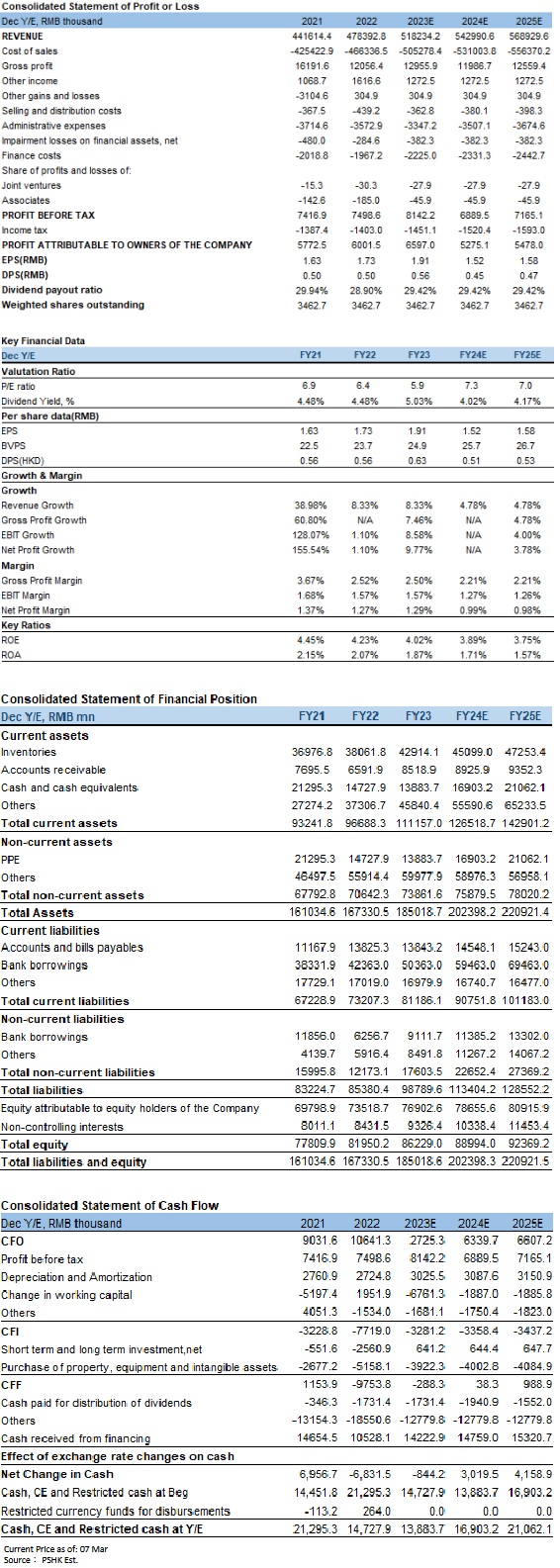

We predict that the company's revenue will be 518.23 billion yuan, 542.99 billion yuan and 568.93 billion yuan respectively in 2023-2025, with a compound annual growth rate of 4.78%, earnings per share (EPS) are projected to be 1.91/1.52/1.58 yuan, and BVPS are projected to be 24.9/25.7/26.7, corresponding to a price-to-book ratio (P/B) of 0.45/0.43/0.42x. The company's average P/B in the past three years is approximately 0.56x. Copper prices continued fluctuating in 2023. With a forecasted 0.55 times P/B in 2023 and a valuation of HKD 14.89, we recommend a "accumulate" rating. (Current price as of March 07)

Risk factors

Macroeconomic environment, changes in market environment, product price fluctuations, impact of safety accidents, exchange rate changes, product substitution risks, and environmental risks.

* The analyst has a financial interest in the listed corporation covered in this report.

Financial

Click Here for PDF format...