Investment Summary

Performance Rebounds Strongly in the First Half of 2023 with Second Highest Net Profit of HK$4.3 Billion

Acoording to Cathay Pacific Airways Limited ("Cathay Pacific" or the "Company") FY2023H result: the Company recorded revenue of HK$43,593 million, up by 135% yoy, which recovered to 81.4% of that in the same period of 2019 (specifically, passenger revenue and cargo revenue recovered to 73.6% and 108% of those in the same period of 2019, respectively). Operating costs stood at HK$36,957 million, accounting for 72.4% of that in the first half of 2019. The attributable profit amounted to HK$4,268 million, which significantly made good a deficit (the loss in the same period of 2022 was HK$4,999 million), and was substantially greater than the figure of HK$1,347 million in the first half of 2019. The corresponding basic earnings per share were approximately HK61.5 cents.

Specifically, a portion of the attributable profit came from a one-off non-cash gain of HK$1.9 billion recognized in the current period: Air China completed A-share seasoned equity offering in January 2023, thus diluting the shareholding of Cathay Pacific in Air China (down from 18.13% to 16.26%), which was regarded as a sale of some shares in Air China..

Favorable Business Indicators and Constant Financial Improve

The passenger load factor of Cathay Pacific in the Reporting Period jumped by 28 percentage points yoy to 87.2%, higher than the figure of 84.2% in the same period before the pandemic (i.e. the first half of 2019, the same below), as driven by the increase in transfer passengers after the resumption of normal traveler clearance between Hong Kong and the Chinese Mainland as well as the surge in demand of flights to Europe and America. Due to the growth of transport capacity, ticket rates fell from the historic high. Meanwhile, the passenger yield declined by 32% yoy to HK77.4 cents, which still greatly exceeded that of HK54.9 cents in the same period before the pandemic. However, the cargo load factor and the cargo yield decreased, as the boom in the pandemic period waned, by 12 percentage points and 51.7% yoy to 63.8% and HK$2.76, respectively, which were 0.4 percentage points and HK$0.88 higher than the pre-pandemic levels.

Fuel Costs Allow Rate Cuts, Burdens from Associates Will Decrease

With respect to costs, the Company's net fuel costs leaped by 304% yoy to HK$10,635 million, accounting for 72% of the pre-pandemic level, because of the growth in fuel consumption of HK$6.5 billion following the work resumption of many planes and the year-on-year decrease of fuel hedging gains of HK$1.51 billion. Nevertheless, unit costs were largely diluted due to the rising business volume. The cost per ton-kilometer (including fuel)fell from HK$5.88 to HK$3.35, which was HK$3.12 before the pandemic. Additionally, the cost per ton-kilometer less fuel decreased from HK$5.19 to HK$2.34, which was HK$2.23 before the pandemic. As of December 11, the trading price of Brent crude oil futures was approximately US$75.67 per barrel, dropping by more than 20% from the peak value of approximately US$97 per barrel in September. We expect fuel costs will continue to decrease.

Cathay Pacific has maintained positive operating cash flow since the beginning of 2023. Moreover, it has redeemed 50% of preference shares recently, and plans to redeem the rest 50% by the end of July 2024. Then, the Company will hopefully restore dividend distribution.

The Company recorded the attributable losses of associates of HK$2.62 billion in the first half of the year, mainly because of Air China's loss of RMB13.4 billion in the accounting period. Fortunately, the Company's burden from associates will significantly decrease, since Air China turned losses into profits of RMB3.72 billion in the second half of the year.

Investment thesis

As of the end of June 2023, the Company had 225 planes, including 35 cargo aircraft (including rented ones). Furthermore, Cathay Pacific has recently announced its plan to purchase 32 passenger aircraft and six cargo aircraft, which will be conducive to expanding outlets and strengthening efficiency. The Company has gotten back on track, after the three-year hardship of the pandemic, and, driven by both demand and supply, will further regain its profitability.

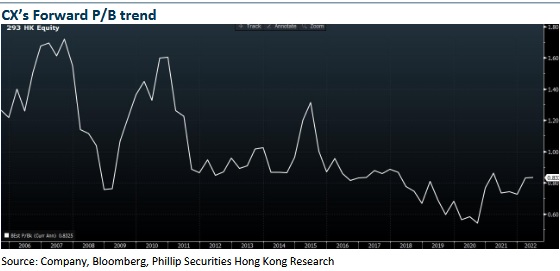

At present, the corresponding price-to-book ratio of the stock price is less than 0.8 times, which is the lowest point in the past 20 years.

Based on the revised financial forecast, we lift target price to HK$10 for the Company, equivalent to 2023/2024/2025E 0.98/0.92/0.84 x P/B, reaffirming the buy rating. (Closing price as at 23 February)

Risk

Surging oil price

RMB depreciation

Demand affected by economy

Transformation program failed

Financials

Click Here for PDF format...