Overview

The company is a leading enterprise in the domestic liquor industry, specializing in the production and sale of Moutai, one of the world's three most famous liquors. As the originator of China's Daqu Maotai-flavor liquor, Moutai is honored as the "national liquor". Currently, the company offers a range of Moutai products with different alcohol content levels, including 43¢X¡A 38¢X¡A and 33¢X Moutai, which have expanded the development space for low-alcohol liquor within the Moutai family. In addition, Moutai Prince Liquor and Moutai Yingbin Liquor cater to mid- to low-end consumers, while 15-year-old, 30-year-old, 50-year-old, and 80-year-old Maotai liquor fill the gap for top-grade, vintage, and aged cellar liquor. The company's product line comprises three series of low-alcohol, high-medium-low-grade, and top-grade liquor with over 70 specifications and varieties. In 2022, the company's brand value surpassed one trillion, ranking first in the global spirits brand value rankings for the seventh consecutive year.

Company performance review

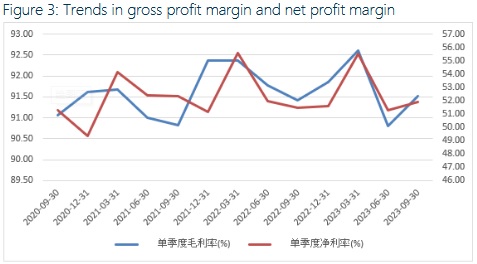

In the first three quarters of 2023, the company achieved a total operating income of 105.316 billion yuan, representing a year-on-year increase of 17.3%. The operating income amounted to 103.268 billion yuan, showing an increase of 18.48% compared to the same period last year. The net profit attributable to shareholders of listed companies reached 52.876 billion yuan, with a year-on-year growth rate of 19.09%. Excluding non-recurring gains and losses, the net profit of shareholders of listed companies was 52.816 billion yuan, representing an increase of 18.97% from the previous year. The gross profit margin decreased by 0.16 percentage points to 91.71%, while the net profit margin dropped by 0.05 percentage points to 53.09%. Earnings per share amounted to 42.09 yuan, showing an increase of 19.09% compared to the same period last year. In the third quarter of 2023, the total operating income amounted to 34.329 billion yuan, representing a year-on-year increase of 13.14%. The operating income stood at 33.692 billion yuan, indicating an increase of 14.04% from the corresponding period in the previous year. The net profit attributable to shareholders of listed companies reached 16.896 billion yuan, with a year-on-year growth rate of 15.68%. After deducting non-recurring gains and losses, the net profit attributable to shareholders of listed companies was 16.868 billion yuan, representing an increase of 15.30% from the previous year. The gross profit margin increased by 0.10 percentage points to 91.52%, while the net profit margin rose by 0.45 percentage points to 51.93%. The increase in the gross profit margin was mainly due to the rise in the proportion of direct sales. The growth rate of operating income in the third quarter was slightly higher than that of the previous two quarters, which was attributed to seasonal characteristics. In the off-season context, the company's adjustment of the shipment pace was conducive to maintaining market competitiveness. In terms of expense ratios, the sales expense ratio/management expense ratio/research and development expense ratio in Q3 2023 were respectively 3.79%/5.65%/0.08%, with year-on-year increases of +0.75pct/-0.90pct/-0.10pct respectively. The increase in the sales expense ratio was mainly due to increased investment in the marketization of the " and other series of wines, while management costs continued to decline with the benefits of scale expansion.

Main business analysis

The company specializes in Maotai liquor and a range of other liquor products. It follows the "strengthening Moutai and expanding its series of wines" dual-wheel strategy. Moutai uses high-quality local waxy sorghum as raw material and wheat-based high-temperature koji. The production process involves unique techniques such as koji usage, prolonged fermentation, multiple fermentations, and multiple wine extractions. Brewing Moutai requires two cuttings and nine fermentations, with a production cycle lasting up to one year. After aging for over three years, blending, and further storage for another year to enhance harmony and smoothness, the wine is ready for bottling and distribution. The entire production process spans approximately five years. Moutai is positioned as a premium liquor, priced at 1,000 yuan and above. Its product line includes 53¢X and 43¢X Moutai under the Feitian trademark and the five-star trademark, aged Moutai (15 years, 30 years, 50 years, 80 years), rare and fine Moutai, Moutai zodiac wine, gift box Moutai, and other varieties based on Moutai and aged Moutai. Among these, the 500ml 53%vol classic Feitian Moutai is the flagship product of Moutai. In recent years, the company has continuously enhanced Moutai product innovation by launching non-standard products such as vintage wine, zodiac wine, solar term wine, etc., thereby enriching its product portfolio. The series of wines primarily comprises three Mao (grains) and four sauces: Guizhou Daqu, Huamao, Wangmao, Laimao, Hanjiang, Renjiu, Prince, and Yingbin. Moutai 1935 also addresses the gap in the company's overall thousand-yuan price range and expands the potential for the development of its series wines.

In terms of product performance, Moutai generated a revenue of 87.27 billion yuan in the first three quarters of 2023, representing a year-on-year growth of 17.30%, accounting for 84.51%. This represented a decline of 0.85 percentage points compared to the previous year. The series of wines achieved a revenue of 15.594 billion yuan, with a year-on-year increase of 24.35%, accounting for 15.10%. This represented an increase of 0.71 percentage points from the previous year. In the third quarter of 2023, Moutai generated a revenue of 27.991 billion yuan, showing a year-on-year growth of 14.55%, accounting for 83.08%. This represented an increase of 0.37 percentage points compared to the same period last year. The series of wines achieved a revenue of 5.520 billion yuan, with a year-on-year increase of 11.69%, accounting for 16.38%. This represented a decrease of 0.34 percentage points from the previous year. The steady growth in Moutai liquor revenue is primarily attributable to products such as 100ml Xiao Moutai, Zodiac Liquor, and Moutai Premium Investment. With increased volume and the successful launch of new products like 24 solar terms wine, Moutai's product portfolio has become increasingly diverse, benefiting from optimized sales channels. The slower growth rate in series wines can be attributed to the company's adjustments in delivery speed and maintenance of market prices during the off-season in the third quarter, aiming to achieve a strategy of increasing sales during peak seasons while maintaining prices during off-peak periods.

The company has developed its offline pipeline through direct operations. In recent years, it has continuously increased its self-operated direct sales, and alcohol e-commerce has gradually become an important purchasing method for consumers. In May 2023, the China Alcoholic Drinks Association and JD Supermarket jointly released the Online Alcohol Consumption Trend Report". The report shows that online wine sales have generally maintained steady growth from 2018 to 2022. Specifically, the compound annual growth rate of foreign wine, wine, and liquor sales exceeded 50%, 40%, and 25%, respectively. Online wine purchases are increasing and gradually becoming a mainstream purchasing method.

Looking at channels, the company's direct sales channel revenue in the first three quarters of 2023 was 46.207 billion yuan, representing a year-on-year increase of 44.93% and accounting for 44.92%. This represents an increase of 8.25 percentage points compared to the previous year. During the same period, the company's wholesale pipeline revenue was 56.657 billion yuan, with a year-on-year increase of 2.90% and accounting for 55.08%. This represents a decrease of 8.25 percentage points compared to the previous year.

In the third quarter of 2023, the company's direct sales channel revenue was 14.787 billion yuan, showing a year-on-year increase of 35.26% and accounting for 44.13%. This represents an increase of 6.91 percentage points compared to the previous year. The wholesale channel revenue was 18.724 billion yuan, with a year-on-year increase of 1.52% and accounting for 55.87%. This represents a decrease of 6.91 percentage points compared to the previous year. The proportion of direct sales further increased due to the increased transaction volume of i Moutai and direct sales channels. As a self-operated e-commerce platform, i Moutai began trial operation on March 31, 2022. In the first three quarters of 2023, the "i Moutai" digital marketing platform achieved alcohol tax-free revenue of 14.871 billion yuan, representing a year-on-year increase of 75.75% and accounting for 10% of the direct sales channel revenue. In the third quarter of 2023, the "i Moutai" digital marketing platform achieved alcohol tax-exclusive revenue of 5.533 billion yuan, showing a year-on-year increase of 36.77% and accounting for 37.42% of direct sales channel revenue, representing an increase of 0.41 percentage points compared to the previous year. It is expected that as the product structure improves in the future, platform performance will further enhance.

On November 1, 2023, the company issued a major announcement. After thorough research and decision-making, the company has decided to increase the factory price of its 53%vol Kweichow Moutai (Feitian, Five Star) starting from November 1, 2023, with an average increase of approximately 20%. According to data from "Moutai Time and Space," this is the eighth price adjustment since Moutai's public listing in 2001. The previous price adjustments occurred in 2001, 2003, 2006, 2008, 2010, 2012, and 2018, with adjustment ranges varying between 10% and 35%. Feitian Moutai boasts strong brand power, and this price increase does not affect the market guide price. The new price for Feitian Moutai now stands at approximately 1,169 yuan/bottle. By increasing the ex-factory price, the company aims to appropriately control dealers` profit margins, encourage dealers to stock up, and boost sales. This price adjustment signifies the return of the price increase mechanism to the market, directly contributing to the company's increased operating income and profits. From an industry perspective, the liquor industry continues to face pressure, and price increases will help drive the overall valuation premium and promote consumption recovery. The fourth quarter is the peak consumption season for the liquor industry, where stocking up occurs in preparation for the Spring Festival. This price increase has a solid market foundation. Furthermore, from an overall product structure standpoint, this price increase breaks industry barriers and facilitates raising prices for products below Feitian Moutai's price range, ultimately optimizing the overall product structure.

Valuation and recommendation

On November 20, the company announced its plan to distribute special dividends to repay shareholders in 2023. The company intends to pay a cash dividend of 19.106 yuan per share to all shareholders and plans to distribute a total cash dividend of 24.001 billion yuan (including tax). This marks the ninth consecutive year that the company has paid dividends exceeding 50%. The special dividend aims to reward shareholders, boost market confidence, share profits with investors, and attract long-term funds to increase the company's valuation.

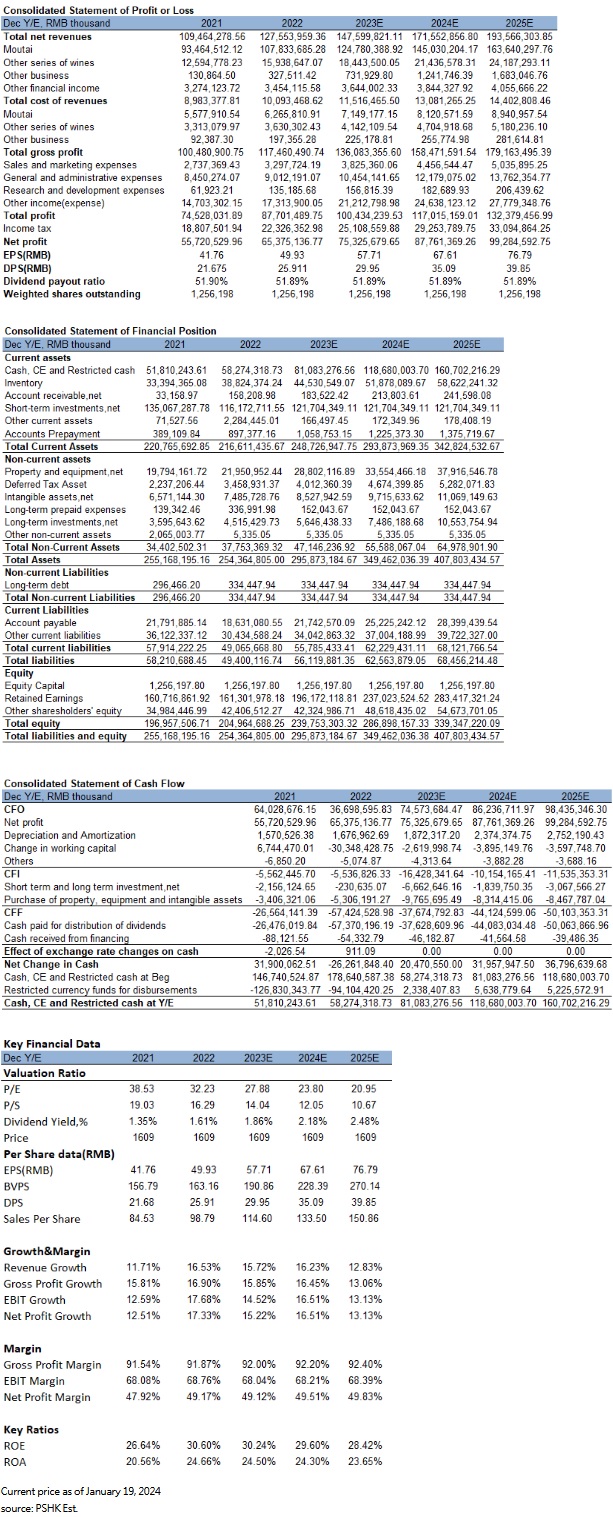

Considering that Moutai's core single product is Feitian Moutai, which caters to high-end business banquets and gifting scenarios, demand remains rigid and less affected by macroeconomic fluctuations. Furthermore, in the third quarter of 2023, the company's coffee and chocolate co-branded products effectively reached more young consumer groups, reflecting the company's focus on the wine industry while continuously pursuing product innovation and establishing an industrial ecosystem centered around "wine" products. We predict that the company's operating income will increase by 16%/16.50%/13% respectively in 2023-2025, reaching 143.956 billion yuan, 167.709 billion yuan, and 189.511 billion yuan. The earnings per share (EPS) are projected to be 57.71/67.61/76.79 yuan, corresponding to price-earnings ratios (P/E) of 27.88/23.80/20.95x. Meanwhile, the company's average P/E in the past three years is approximately 43.04. With a forecasted 31 times P/E in 2023 and a valuation of RMB 1,789, we recommend a "buy" rating. (as of January 19).

Risk warning: (1) The weakening of consumer spending power is negatively impacting industry demand. (2) There have been recent changes in industrial policies that are affecting the market.

�Financial

Click Here for PDF format...