Sectors:

Air & Automobiles (Zhang Jing),

TMT, Semiconductors, Consumer, Healthcare (Eric Li)

Energy, Consumer (Judy Li)

Automobile & Air (ZhangJing)

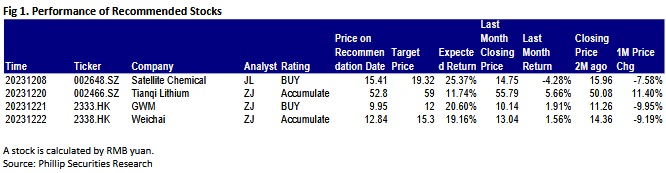

This month I released 3 updated reports of Tianqi(002466.CH), GWM (2333.HK), and Weichai(2338.HK).

Since the beginning of this year, as affected by supply-demand mismatch and destocking of the industry chain, the prices of lithium salt plunged from RMB500 thousand per ton last year to approximately RMB100 thousand per ton. Consequently, Tianqi Lithium recorded an operating revenue of RMB8,576 million in Q3, which fell by 17.14% yoy and by 35.88% qoq. Its net profit attributable to shareholders amounted to RMB1,646 million, which decreased by 70.89% yoy and increased by 4.38% qoq. Nevertheless, thanks to its complete self-sufficiency of the raw material, lithium concentrates, the Company enjoys advantages in cost control and vertical integration of the industry chain and its gross margin remains high. Specifically, the gross margin in the first three quarters and Q3 reached 86.6% and 85.23%, with a yoy increase of 1.1 and a yoy decrease of 2.1 ppts, respectively. We predict that lithium prices may still experience low fluctuations in the short term. However, high growth of and cost support and preferential policies for the downstream industries, especially new energy vehicles, shipping, and energy conservation, are promising in medium and long term. The fundamentals of the lithium industry are likely to achieve sustained, sound growth in the next few years. The Company has made the layout of the best lithium resources worldwide, practiced a vertical integrated business model, and achieved the 100% self-sufficiency of lithium concentrates. In combination of the advanced production and processing of lithium compounds, it can maximise the profit margin of lithium products, and will continue to consolidate its leading position based on its future capacity expansion.

GWM has been deepening new energy and intelligent transformation, adjusting the product mix and increasing investments in brand and channel building since H2 of last year, and has realized the flat, network-based and decentralized layout covering the entire industrial chain in new energy and intelligence sectors. Meanwhile, it continued to invest in the R&D in the fields of new energy and intelligence, and rolled out new models with DHT and the brand-new Hi4 technology, such as All-New Haval H5, Haval 2nd Generation Big Dog PHEV, Haval Menlong, Haval Xiaolong, WEY Lanshan, WEY Gaoshan, TANK 400Hi4-T and TANK 500Hi4-T, by the end of last year. As of late October, the Company has unveiled 10 new models this year, including 8 plug-in hybrid models. In the next step, it will roll out new energy models such as TANK 300 Hi4-T, New Haval Xiaolong MAX, New WEY Latte, Lanshan's advanced edition with intelligent driving and Ora Lighting Cat Dark Night Edition. The gross profit margin decreased by 1 percentage point yoy to 20.6%, mainly due to the favorable exchange direction in 2022H1, resulting in a higher base. In addition, due to GWM's increased R&D investment in the first half of the year to ensure its ability to undertake orders, the proportion of revenue increased from 1.9 ppts to 8.9% compared to the same period last year. During the period, the profit attributable to shareholders was RMB 150 million, a slight increase of 1% yoy. The net profit attributable to shareholders ratio was 5.9%, a decrease of 1.5 ppts yoy.

If the additional increase in R&D investment is not included, the operating profit margin will actually increase slightly by 0.5% compared to 2022H1. The Management pointed out that the peak period of R&D investment in the first half of the year has passed, and in the future, it will return to the normal revenue proportion level of around 7%. The expense ratio level is expected to improve in the second half of the year. We believe that the Company's current strategy of increasing R&D investment and competing for more market share may put pressure on profit margins in the short term, but it provides a foundation for long-term competitive and sustainable development. H6 Midterm Modified Edition, a sedan of WEY and TANK 700/800 will also be included in the brand matrix in the future. Driven by new models, Great Wall Motor sold 170 thousand new energy models accumulatively in the first three quarters, accounting for 19.7% of the total, up 7.4 ppts from 12.3% for 2022.

As natural gas prices are dramatically lower than diesel prices, natural gas-fueled heavy trucks have emerged to be the most eye-catching segment during the recovery of the heavy truck industry this year. The cumulative domestic sales of natural gas-fuelled heavy trucks from January to September amounted to 107.4 thousand, up 255% yoy. Weichai has been the leader of engines for natural gas-fueled heavy trucks in China, with a market share of nearly 70%. Additionally, the export of heavy trucks has maintained a fast growth this year. Statistically, 210 thousand heavy trucks were exported from January to September, up 70% yoy, which represented up to 30% of the total exports and hit a record high.

Thanks to several favorable factors, Weichai Power sold 548 thousand engines in the first three quarters, which climbed by 24.5% yoy. Particularly, 52 thousand of them were exported, with a year-on-year increase of 35.6%. In terms of commercial vehicle business, Shaanxi Heavy Duty Automotive Co., Ltd. (Shaanxi Zhongqi), a controlling subsidiary of the Company, sold 92 thousand heavy trucks in the first three quarters, up 52% yoy, wherein 42 thousand were exported with a year-on-year increase of 71.9%. In regard to intelligent logistics business, KION Group AG (KION), a controlling subsidiary of the Company, recorded the net profit before interest and tax of EUR570 million in the first three quarters, which jumped by 171.6% yoy. As shown in its 2023 A-share Restricted Equity Incentive Plan Draft released, the target values of revenue for 2024, 2025, and 2026 are RMB210.2 billion, RMB231.2 billion, and RMB258.9 billion, respectively. The EBT margin is 8%, 9%, and 9%, respectively, and the EBT target are RMB16.8 billion, RMB20.8 billion, and RMB23.3 billion. The above objectives exceed market expectations, indicating the Company's great confidence in its future growth ratio.

Energy, Consumer (Judy Li)

This month I released reports of Satellite Chemical Co., Ltd. (002648.SZ).

The company is a leading integrated manufacturer of light hydrocarbon industry chain in China, focusing on three major fields: functional chemicals, new polymer materials, and new energy materials. It owns the first imported ethane comprehensive utilization unit, the first propane dehydrogenation unit, The largest acrylic production facility in China, with production capacity of HDPE (high-density polyethylene), EO (ethylene oxide), EG (electro-galvanizing), SAP (super absorbent resin), polyether macromonomer, hydrogen peroxide and other products Ranking at the forefront in the country, its products are widely used in aerospace, new energy vehicles, electronic chips, agriculture and forestry maintenance, health care and other fields.

In the first half of 2023, the company achieved operating income of 20.014 billion yuan, a year-on-year increase of 6.38%. The net profit attributable to the parent company was RMB 1.843 billion, a year-on-year decrease of 34.13%. Achieved non-net profit of RMB 1.952 billion, a year-on-year decrease of 28%. The gross profit margin was 17.51%, a year-on-year decrease of 6.97 percentage points. The net profit margin was 9.20%, a year-on-year decrease of 5.64 percentage points. Among them, revenue in the second quarter was 10.599 billion yuan, a year-on-year decrease of 0.72% and a month-on-month increase of 12.57%. The net profit attributable to the parent company was 1.136 billion yuan, a year-on-year decrease of 9.87% and a month-on-month increase of 60.59%. Achieved non-net profit of RMB 1.17 billion, a year-on-year increase of 1% and a month-on-month increase of 51%. The gross profit margin was 18.62%, a year-on-year decrease of 2.37 percentage points and a month-on-month increase of 2.35 percentage points. The net profit margin was 10.71%, a year-on-year decrease of 1.1 percentage points and a month-on-month increase of 3.22 percentage points.

The company's Pinghu base new materials and new energy integration project is planned to be operational by the end of 2023. The annual output of 360,000 tons of acrylic acid and 720,000 tons of ester technological transformation projects, 300,000 tons of polypropylene and 250,000 tons of hydrogen peroxide projects will make more efficient use of PDH's propylene Resources produce multi-carbon alcohols, forming a closed industrial chain of propylene-acrylic acid-acrylate. According to information from Baichuan Yingfu, China's actual acrylic acid consumption will reach 2.415 million tons in 2022, a year-on-year increase of 23.4%, and the CAGR in the past five years has reached 10.3%. In 2022, the proportion of CR5 in the acrylic acid industry will reach 60.9%, and the industry concentration is high. Among them, satellite chemicals have a market share of 18.9%, ranking the industry leader. The company has sufficient reserves of projects under construction, and its future growth potential is expected to be gradually realized.

Click Here for PDF format...