Investment Summary

Q3 Results Beat Expectations

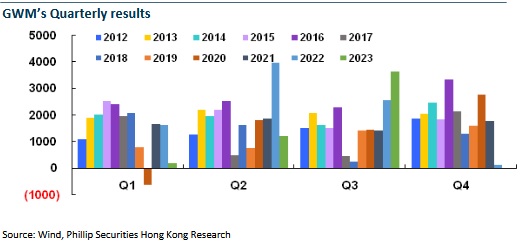

In 2023 Q3, Great Wall Motor recorded revenue of RMB49.53 billion, up 33% yoy and 21% qoq, net profit attributable to the parent company of RMB3,634 million, up 42% yoy and 206% qoq, and net profit attributable to the parent company excluding non-recurring items of RMB3,058 million, up 34% yoy and 217% qoq, with the results beating expectations. In Q1 and Q2, the Company saw a yoy decrease of 13.6% and yoy increase of 43.5%, respectively, in revenue, and a yoy decrease of 89.3% and 70.1%, respectively, in the net profit attributable to the parent company. On account of the sharp contraction of the profits in the transition period in H1, the accumulated revenue recorded by the Company in the first three quarters grew by 20% yoy to RMB119.5 billion and the net profit attributable to the parent company fell by 38.8% yoy to RMB4,995 million.

Higher Proportion of High-end Models Drives up Unit Prices and Profitability

In Q3, the Company's gross margin was 21.7%, down 0.8 ppts yoy and up 4.3 ppts qoq, mainly owing to the structural improvements of models, reduction of battery costs and the scale effect brought by higher sales volumes. The positive scale effect of revenue played a positive role in the fall of the expense ratio. The expense ratio of sales, management and R&D is 3.7%, 2.1% and 4.0%, respectively, down 0.6, 1.3 and 0.1 ppts yoy and 0.7, 0.4 and 0.8 ppts qoq.

In Q3, the Company sold 344,800 vehicles, a yoy increase of 21.5% and qoq increase of 15.2%, above the industry growth rate, mainly owing to great sales in overseas markets and high-gross-margin models. Specifically, 87,800 vehicles were sold in overseas markets, a qoq increase of 22% and accounting for more than 25% of the total sale (up 1.41 ppts yoy). The annual expectation of 300 thousand for overseas sales is expected to be exceeded. Both the average sales price and gross margin of models in overseas markets were higher than those in domestic markets, contributing more to the increase in the unit price and the improvement of profitability. In Q3, models of the Company that were sold at a unit price of RMB150 thousand or higher accounted for 23.53% of the total, up 1.21 ppts qoq, bringing an average single vehicle revenue of RMB143,600 to the Company during the reporting period, up 9.2% yoy and 5.0% qoq. On average, the net profit excluding non-recurring items of a single vehicle was RMB8,900, an increase of RMB5,700 qoq.

Electrification Strategy Ushers in a Period of Rapid Growth

The Company has been deepening new energy and intelligent transformation, adjusting the product mix and increasing investments in brand and channel building since H2 of last year, and has realized the flat, network-based and decentralized layout covering the entire industrial chain in new energy and intelligence sectors. Meanwhile, it continued to invest in the R&D in the fields of new energy and intelligence, and rolled out new models with DHT and the brand-new Hi4 technology, such as All-New Haval H5, Haval 2nd Generation Big Dog PHEV, Haval Menlong, Haval Xiaolong, WEY Lanshan, WEY Gaoshan, TANK 400Hi4-T and TANK 500Hi4-T, by the end of last year. As of late October, the Company has unveiled 10 new models this year, including 8 plug-in hybrid models. In the next step, it will roll out new energy models such as TANK 300 Hi4-T, New Haval Xiaolong MAX, New WEY Latte, Lanshan's advanced edition with intelligent driving and Ora Lighting Cat Dark Night Edition.

H6 Midterm Modified Edition, a sedan of WEY and TANK 700/800 will also be included in the brand matrix in the future. Driven by new models, Great Wall Motor sold 170 thousand new energy models accumulatively in the first three quarters, accounting for 19.7% of the total, up 7.4 ppts from 12.3% throughout 2022.

From the perspective of orders, more than 20 thousand units of TANK 500Hi4-T have been ordered, and more than 12 thousand units of TANK 400Hi4-T and more than 10 thousand units of Haval Menglong were ordered in the first month or day after they were rolled out, indicating the competitive strength of the Company's products in different market segments. It is expected that, with the roll-out of new models and the refinement of channels, the Company will continue to see sales growth, which will speed up its new energy transformation on all fronts.

Investment Thesis

In October 2023, the sales volume of Great Wall Motor was up 31.04% yoy and 7.96% mom to 131,308 vehicles. Haval and TANK recorded a strong performance, with a yoy increase of 23.43% and 73.33% to 74 thousand and 22 thousand vehicles, respectively, in the number of vehicles sold. Ora and Steed sold 11 thousand and 17 thousand vehicles, up 94.3% and 10.4% yoy, respectively, and WEY sold 2,256 vehicles, down 7.1% yoy. Meanwhile, the penetration rate of new energy vehicles continued to rise to 23.3%, and 35,400 new energy vehicles were sold overseas, above 30 thousand for three consecutive months.

The Company has set resolute strategic objectives and clear steps for new energy and high-end-oriented transformation. The roll-out of new models, the further improving overseas market layout and the continuous decline in the cost of raw material parts such as batteries in Q4 amid a strong product cycle are expected to make revenue and net profit more elastic. We think that Great Wall Motors` long-term layout of new technologies and new product systems will facilitate its share rally and bring stable returns in the future.

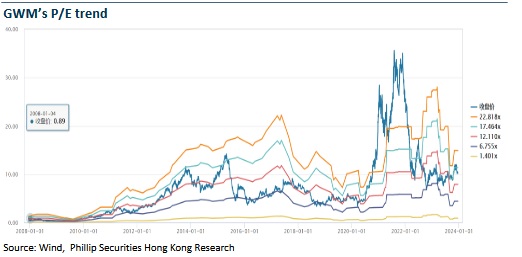

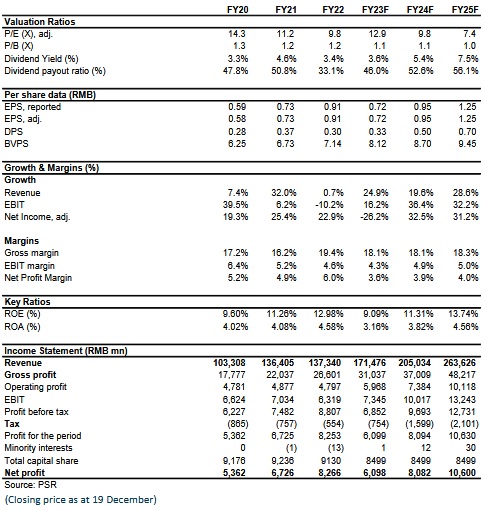

Considering latest financial forecast, we revised our target price to HK$12, equivalent to 15.6/11.8/9x P/E and 1.4/1.3/1.2x P/B in 2023/2024/2025. We gave the rating of ¡§Buy¡¨. (Closing price as at 19 December)

Risk

New vehicle sales fall short of expectations

The SUV market dramatically worsens

The progress of new energy vehicle/Pickup is poorer than expectations

Financials

Click Here for PDF format...