Investment summary

Lithium Prices Plummet, Performance in Q3 Slumps

Tianqi Lithium Corporation (hereinafter referred to as "Tianqi Lithium" or the "Company") has recently disclosed its report for the third quarter (Q3). The Company recorded an operating revenue of RMB33,399 million in the first three quarters this year, with a year-on-year increase of 35.52%, as shown in the report. The net profit attributable to shareholders stood at RMB8,099 million, down 49.33% yoy. The increase in the yoy revenue in the first three quarters mainly contributed to: The launch and constant growth in capacity of the tailings pond of the Greenbushes mine raised the output. Meanwhile, the negotiated prices lagged behind the market prices in 2023H1, and the average price of lithium minerals was higher than that in the same period last year. The decline in the performance was mainly due to: 1) The drastic drop in the prices of lithium chemical products led to a decrease in their gross margin. 2) Because of the rise in the selling prices of lithium minerals, the net profit of Windfield Holdings Pty Ltd., a holding subsidiary of the Company, grew, and the profit and loss of minority shareholders increased. 3) The listing of SES, a joint-stock company of the Company, in the same period of 2022 resulted in nonrecurring return on investment, which did not occur in the current period. 4) The yoy decrease in the return on investment of the associated company, SQM, recognised for the current period, should be subject to the Q3 report to be officially released by the company.

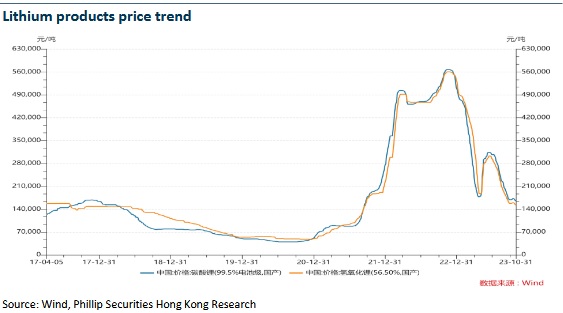

Since the beginning of this year, as affected by supply-demand mismatch and destocking of the industry chain, the prices of lithium salt plunged from RMB500 thousand per ton last year to approximately RMB170 thousand per ton at the end of April, which then rebounded to RMB300 thousand per ton in June and yet fell to around RMB160 thousand per ton. According to Wind, the Q3 average prices of lithium carbonate and lithium hydroxide for batteries in China were RMB240.6 thousand per ton and RMB223.6 thousand per ton, with the yoy decreases of 50.1% and 52.9%, respectively. As of October 27, 2023, the prices of lithium carbonate and lithium hydroxide for batteries decreased by 69.43% and 70.07% from the same period last year and by 66.73% and 70.91% from the beginning of the year to RMB168 thousand and RMB160 thousand per ton, as revealed by BAIINFO.com.

Consequently, Tianqi Lithium recorded an operating revenue of RMB8,576 million in Q3, which fell by 17.14% yoy and by 35.88% qoq. Its net profit attributable to shareholders amounted to RMB1,646 million, which decreased by 70.89% yoy and increased by 4.38% qoq.

Nevertheless, thanks to its complete self-sufficiency of the raw material, lithium concentrates, the Company enjoys advantages in cost control and vertical integration of the industry chain and its gross margin remains high. Specifically, the gross margin in the first three quarters and Q3 reached 86.6% and 85.23%, with a yoy increase of 1.1 and a yoy decrease of 2.1 ppts, respectively. Additionally, Tianqi Lithium is ranked among the top in net profit margin, which was 66.98% and 68.6%, down 12.36 and 7.37 ppts, respectively. Moreover, the Company's financial profile is stable, and its debt-equity ratio was only 30.59%, up 5.5 ppts from the beginning of the year. The net operating cash inflow was RMB20 billion, rising by 71% yoy, mainly due to increased payment collection.

Strategic Investor Zijin Mining Is Introduced, Capacities in Domestic and Overseas Bases Are Continuously Enhanced

In regard to lithium minerals, the capacity of lithium concentrates of Talison Lithium Pty Ltd. (Talison Lithium) is 1.62 million tons/year. In mid-2025, the planned capacity of the No. 3 processing plant at the chemical grade3 will exceed 2.1 million tons/year, after its launch with the capacity of 520 thousand tons/year. Furthermore, the construction of the No. 4 processing plant at the chemical grade, with the capacity of 520 thousand tons/year, will begin in 2025, which is estimated to be launched by 2027. The long-term planned capacity of Talison Lithium will reach 2.66 million tons/year.

Sichuan Tianqi Shenghe Lithium Industry Co., Ltd., a wholly-owned subsidiary of the Company, introduced the strategic investor, Zijin Mining, through share capital increase in May 2023. The subsidiary has the mining right of the lithium mine in Cuola Town, Yajiang County, Sichuan Province. Currently, it is conducting feasibility research regarding the restart and site selection of the Phase 1 project of spodumene ores in Cuola Town. The strengths in mineral exploitation and construction of the strategic investor of Zijin Mining will promote project construction, further accelerate the conversion of the Company's existing resources to capacity/output, and enrich Tianqi Lithium's domestic resources.

In terms of lithium compound projects, the Company's current capacity is 68.8 thousand tons/year, and the planned capacity surpasses 140 thousand tons. Specifically, the 20 thousand-ton lithium carbonate project in Anjv District, Sichuan Province is estimated to be completed and commissioned by 2023H2. The Phase 1 24 thousand-ton lithium hydroxide project in Kwinana, Australia, is being promoted gradually, and has been certified by the South Korean battery maker, SK on. The Phase 2 24 thousand-ton project is under initial preparation. The construction of the Phase 1 30 thousand-ton lithium hydroxide in Zhangjiagang has been initiated and is expected to be completed within two years. The Company strives to push the total capacity to 300 thousand tons by 2027, 4.36 times as much as the current capacity.

Valuation and Investment thesis

We predict that lithium prices may still experience low fluctuations in the short term. However, high growth of and cost support and preferential policies for the downstream industries, especially new energy vehicles, shipping, and energy conservation, are promising in medium and long term. The fundamentals of the lithium industry are likely to achieve sustained, sound growth in the next few years. The Company has made the layout of the best lithium resources worldwide, practiced a vertical integrated business model, and achieved the 100% self-sufficiency of lithium concentrates. In combination of the advanced production and processing of lithium compounds, it can maximise the profit margin of lithium products, and will continue to consolidate its leading position based on its future capacity expansion.

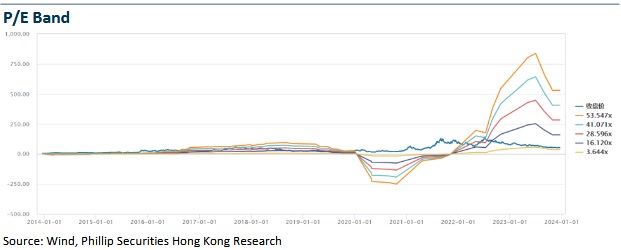

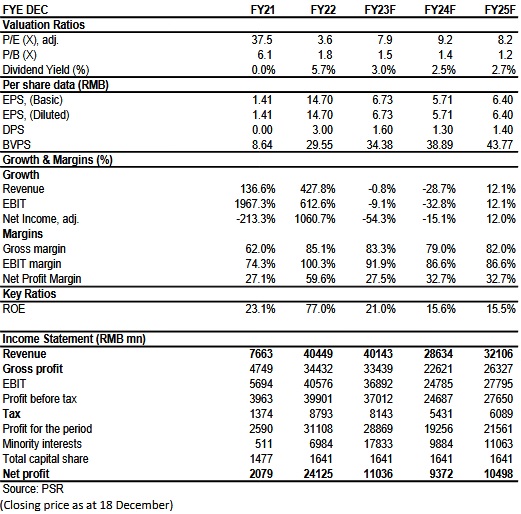

We expected diluted EPS/BVPS of the Company to RMB6.73/5.71/6.40 and 34.4/38.9/43.8 of 2023/2024/2025. And we accordingly gave the target price to 59, respectively 8.8/10.3/9.2x P/E for 2023/2024/2025. "Accumulate" rating. (Closing price as at 18 December)

Risk

New business progress slower than expected

Lithium series Product price falling

Financials

Click Here for PDF format...