Pop Mart International Group Limited (09992) is principally engaged the product design and development and sale of pop toys in China and certain overseas countries and regions. Pop Mart brand products are primarily categorized into blind boxes, action figures, BJDs and accessories. Revenue of the Company is generated in Mainland China and Hong Kong, Macao, Taiwan and overseas through: offline channels, online channels, and wholesales channels and others. Proprietary products of Pop Mart are mainly divided into: artist IPs and licensed IPs. Artist IPs are the major product type of the Company, primarily including MOLLY, SKULLPANDA, DIMOO and THE MONSTERS.

In 1HFY2023, Pop Mart opened 19 new physical stores in Mainland China. The number of physical stores increased to 340. The company opened 118 roboshops in Mainland China. The number of roboshops increased to 2,185. The total number of registered members in Mainland China increased to 30.388 million. In particular, there were 4.384 million new registered members. During the first half of 2023, the sales contributed by members represents 92.2% of total sales, with repeat purchase rate of the member of 44.5%. The number of stores in Hong Kong, Macao, Taiwan and overseas cities amounted to 55 (including joint ventures) and the number of roboshops amounted to 143 (including joint ventures and franchise), respectively, with overseas e-commerce platforms reaching 28. Pop Mart established the first physical store in the France and Malaysia during the period.

Operations resume normal in 1HFY2023. Offline sales recover rapidly

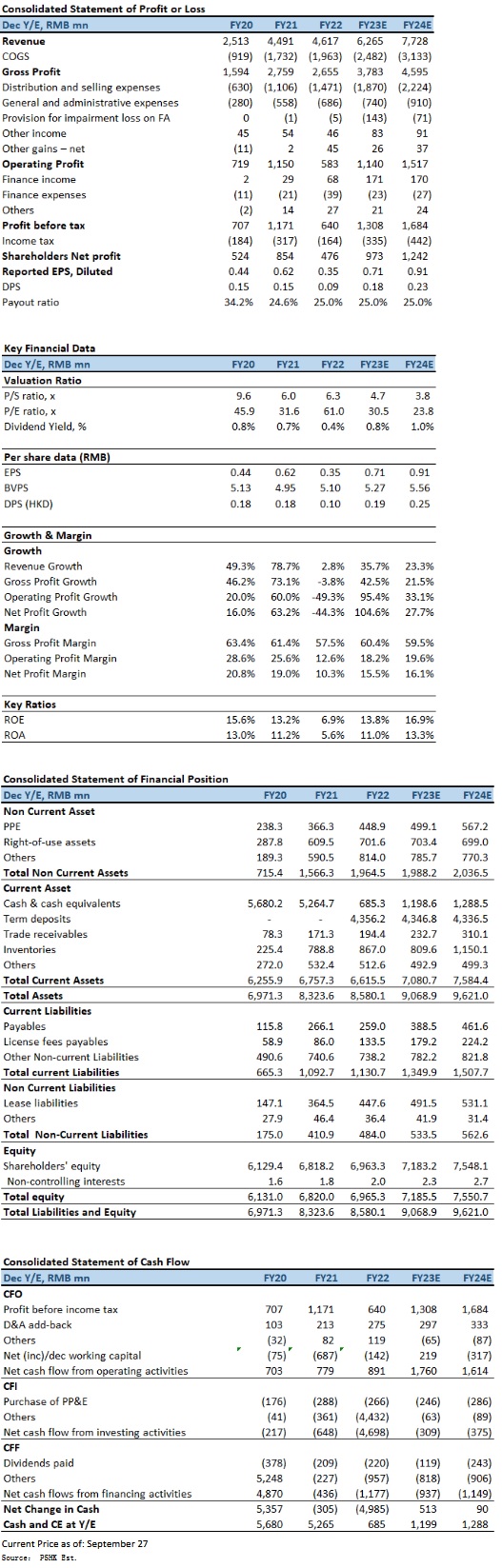

In 1HFY2023, Revenue of the company increased to RMB2,814 million, representing a year-on-year increase of 19.3%. Profit for the period increased to RMB477 million, representing an increase of 43.3% YoY. Basic EPS were RMB35.46 cents, and no interim dividend was paid. Non-IFRS adjusted net profit (after excluding share-based payment) increased to RMB535 million, representing an increase of 42.3% YoY.

Costs of sales increased by 12.9% to RMB1,116 million. The Company's gross profit increased by 23.9% to RMB1,698 million. Gross profit margin increased from 58.1% for the first half of 2022 to 60.4% for the first half of 2023, primarily due to the increase in gross profit margin of proprietary products.

Revenue from Mainland China Offline channels increased by 32.4% to RMB1,451 million, amongst which, revenue from retail store sales increased by 32.3% YoY to RMB1,179 million, primarily due to the number of retail stores increased, offline channels consumption has recovered due to full resumption of normal social and economic operations in the first half of 2023; and enhance the image of store decoration, improve the display effect and relocate to a better location to attract foot traffic, thereby boosting sales. Revenue from roboshop sales increased by 32.9% YoY to RMB271 million, primarily due to the roboshops increased, gradually relocated machines with low sales to premium sales locations; with the recovery of offline consumption and tourism market, machines in high-speed railway stations, airports, scenic spots, cinemas and other scenes saw rapid growth in sales.

Revenue from online sales decreased by 16.4% to RMB817 million, amongst which, revenue from Pop Draw decreased by 31.4 % to RMB373 million, revenue from Tmall flagship store decreased by 36.6 % to RMB155 million; and revenue from DouYin platform increased by 569.0% to RMB110 million. In 2023, affected by the general online environment, the rapid development of content e-commerce platforms such as Tik-Tok, and dispersion of online consumption with the recovery of consumption in offline channels, the traditional e-commerce platforms were shocked.

Revenue from wholesales and others in Mainland China increased by 32.3% to RMB170 million, primarily due to the increased store sales of the distributor, Nanjing Pop Mart.

Revenue from offline sales of Hong Kong, Macao, Taiwan and overseas increased by 392.4% to RMB190 million, amongst which, revenue from retail store sales increased by 374.2% YoY to RMB165 million, primarily due to the increase in the number of retail stores, continuous expansion of channels in Hong Kong, Macao, Taiwan and overseas channels and opening of retail stores in more countries and regions. Revenue from roboshop sales increased by 556.5% YoY to RMB25.4 million, primarily due to an increase in the number of roboshops. Revenue from online channels in Hong Kong, Macao, Taiwan and overseas includes those generated from Pop Mart official website, Shopee and other online channels, and revenue from online sales increased by 63.1% to RMB56.8 million. Amongst which, revenue from Shopee increased by 145.8% to RMB14.8 million; and revenue from Pop Mart official website decreased by 23.3% to RMB12.32 million. Revenue from wholesales and others in Hong Kong, Macao, Taiwan and overseas regions increased by 54.6% to RMB129 million, primarily due to the increasing brand awareness.

Revenue from proprietary products contributed 91.9% of the total revenue. Revenue from proprietary products increased by 20.0% RMB2,586 million. Amongst which, The proportion of revenue from artist IPs decreased to 76.9%. Revenue from artist IPs increased by 16.7% to RMB2,164 million, primarily due to the increased revenue contribution from sales of SKULLPANDA, MOLLY, DIMOO and THE MONSTERS and newly superscript IPs, such as HACIPUPU, Zsiga, PINO JELLY, also achieved outstanding performance.

The performance of top IPs remained strong. Revenue generated from SKULLPANDA, MOLLY and DIMOO amounted to RMB526 million, RMB411 million and RMB362 million, respectively, representing a YoY increase of 14.0%, 1.8% and 21.3%, respectively. HACIPUPU, a brand new IP launched in 2HFY2022 was widely recognized by fans, and its revenue amounted to RMB69.2 million in 1HFY2023. Revenue generated from Hirono and Sweet Bean, launched by Pop Mart in-house design team PDC (Pop Design Center), amounted to RMB109 million and RMB75.4 million, respectively, representing a YoY increase of 191.3% in revenue in 1HFY2023.

3QFY2023 growth continues. Maintain overseas expansion

According to the latest business update for 3QFY2023, Overall revenue in Q3 recorded a period-on-period increase of 35%-40%, among which, revenue attributed from operations in Mainland China recorded a period-on-period increase of 25%-30% and revenue attributed from operations in Hong Kong, Macao, Taiwan and overseas recorded a period-on-period increase of 120%-125%.

The revenue attributed from each respective channel of the operations in the Mainland China: for retail stores operations, was recorded an increase of 35%-40%; for roboshops operations, it was recorded an increase of 45%-50%; for Pop Draw operations, it was recorded a decrease of 10%-15%; for the operations of e-commerce platforms and other online platforms, it was recorded an increase of 20%-25, of which the operations for Tik-Tok flagship store recorded a increase of 875%-880% and the operations for Tmall flagship store recorded a decrease of 20%-25%; and for the operations in wholesales and other channels, it was recorded an increase of 50%-55%.

Investment Thesis

With the development of trendy of pop toy culture, fans` demand for trendy pop toys is increasing and becoming more diverse. In the past, the company has been committed to enrich IPs types, expand IPs base, and introduce more products under the head series. It can be expected that it will further tap explore the value of box products such as MEGA, POP BEAN, side products and BJD. While further engaging in the pop toy business, the company has continued to create new brands including MEGA, GONG and inner flow, and facilitate the establishment of amusement parks and other new businesses to construct a more sophisticated and comprehensive business ecosystem with IP at its core, which would be able to exert a greater "long tail effect". We expect FY2023E-FY2024E EPS to be $0.71 and $0.91 respectively, with PT of HK$28.47, implies a FY2024E P/E of 28.3x (~2-yrs historical average plus 1 standard deviation). Our investment rating is ¡§Accumulate¡¨.

Risk factors

1) Consumption recovery is slower than expected; 2) Inventory impairment risk; 3) Overseas sales are less than expected; and 4) New IP/products are less attractive than expected.

�Financial

Click Here for PDF format...