Overview

China Power (2380.HK) is a core subsidiary of State Power Investment Corporation Limited. Its main businesses include hydropower, wind power, photovoltaic power, coal-fired power, natural gas power, environmental power, energy storage, green electricity transportation and color photovoltaics. The group has power plants in many places across the country. In recent years, the company has been committed to accelerating the transformation of clean energy, acquiring multiple clean energy projects actively and selling part of its original shares in the coal power business.

Company Performance review

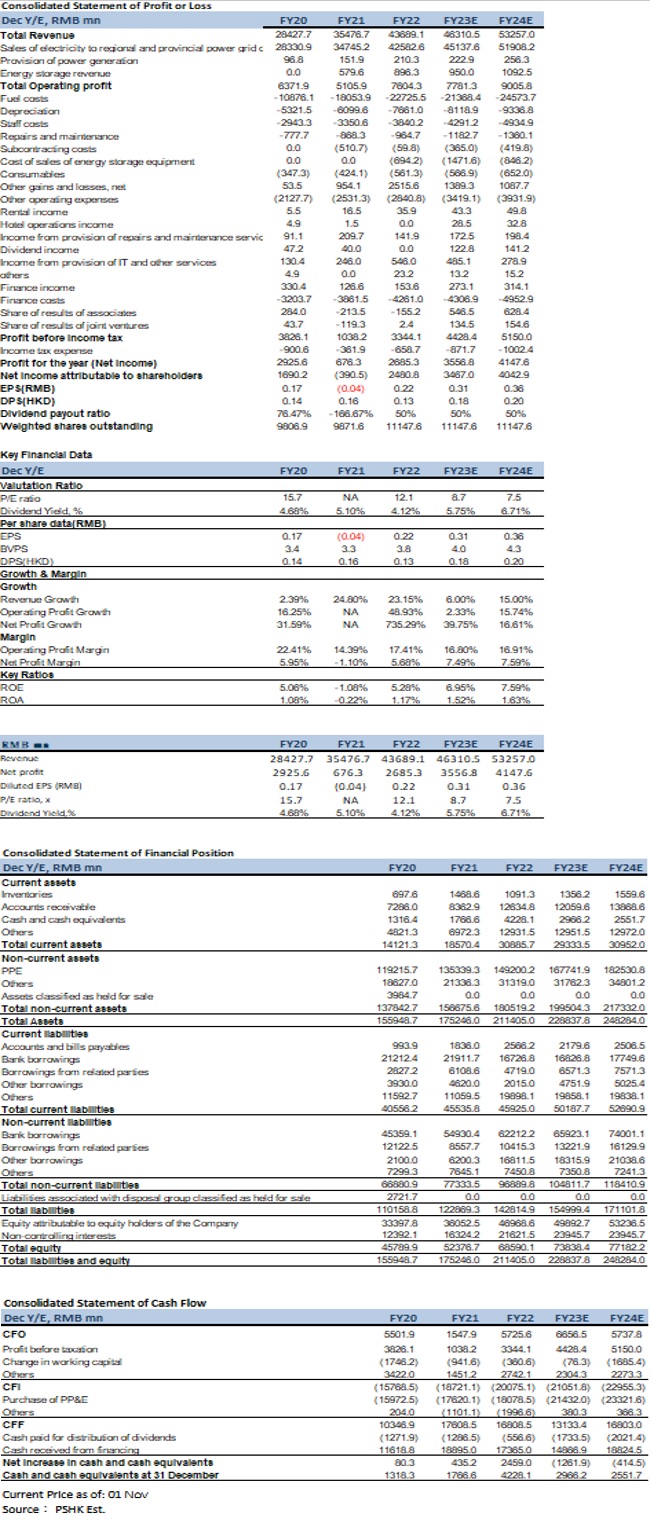

The company's revenue in the first half of 2023 was 21.32 billion yuan (RMB, the same below), an increase of 4.98% YoY. Operating costs were 17.6 billion yuan, an increase of 4.35% YoY. Operating profit was 4.48 billion yuan, an increase of 11.50% YoY. Basic earnings per share were 0.14 yuan. Profit attributable to Ordinary shareholders of the Company was 1.68 billion yuan, an increase of 114.36% YoY which was due to the company's active independent development and acquisition of high-quality clean energy. Besides, it benefited from thermal power's significant turnaround from losses to profits YoY. At the same time, generation capacity, output and revenue of wind power and photovoltaic power increased significantly, which offset the impact of insufficient hydropower sales in the first half due to lower rainfall effectively.

Industry Analysis

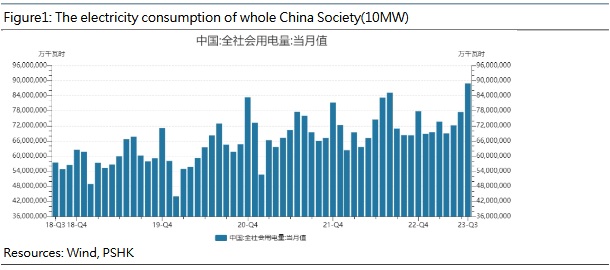

In the first half of 2023, the electricity consumption of the whole society was 4,307.6 billion kWh, an increase of 5.0% YoY. The electricity consumption of the primary industry was 57.7 billion kWh, an increase of 12.1% YoY; the electricity consumption of the secondary industry was 2,867 billion kWh, an increase of 4.4% YoY; the electricity consumption of the tertiary industry was 763.1 billion kWh, an increase of 9.9% YoY. The domestic electricity consumption of urban and rural residents was 619.7 billion kWh, an increase of 1.3% YoY. From Figure 1, we can find that the electricity consumption of the whole society has increased steadily year by year in the past five years. Electricity consumption has cyclical characteristics. Generally speaking, from July to September, we live in the summer, and electricity consumption is relatively high; from February to April, electricity consumption is relatively low.

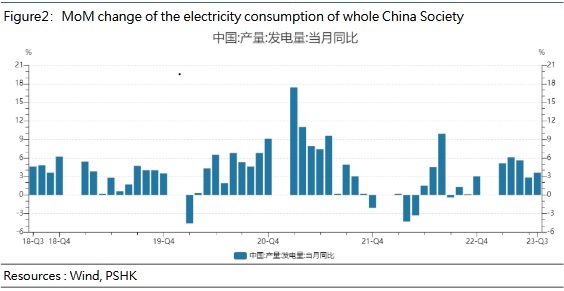

In the first half of 2023, the national power generation capacity was 4168 billion kWh, an increase of 3.8% YoY, of which hydropower decreased by 22.9%, wind power increased by 16.0%, solar power increased by 7.4%, and thermal power increased by 7.5%. Figure 2 shows the YoY increase of national power generation in the past five years.

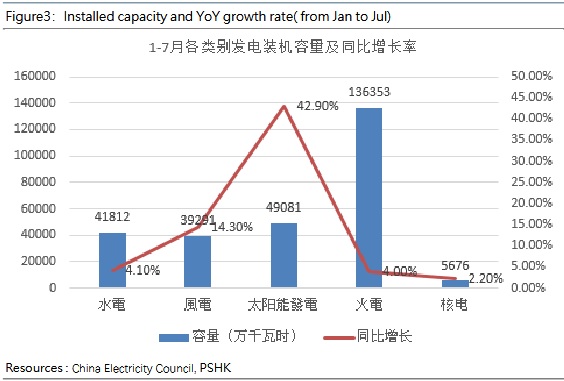

As of July 31st, the country's cumulative installed power generation capacity was approximately 2.74 billion kW, an increase of 11.5% YoY. The installed capacity and YoY growth rate are shown in Figure 3. We can see that solar power generation gained the highest YoY increase of 42.9%. In the future, the proportion of new energy power generation will continue to increase and gradually become the mainstay of our country's power generation.

From January to July 2023, the country's major power generation companies completed investment of 401.3 billion yuan in power engineering projects, an increase of 54.4% YoY, of which solar power generation accounted for 161.2 billion yuan, an increase of 108.7% YoY.

China Electricity Council released the "Analysis and Forecast Report on National Electricity Supply and Demand Situation in the First Half of 2023", which predicted that the electricity consumption of the whole society in 2023 will be 9.15 trillion kWh, an increase of about 6% YoY, of which the electricity consumption of the whole society will increase by 6%~7% YoY in the second half of the year. Driven by the rapid development of new energy power generation, it is expected that the scale of newly installed power generation capacity nationwide in 2023 will exceed 300 million kW for the first time in history. By the end of 2023, the total installed capacity of grid-connected wind power and solar power will reach 960 million kW, accounting for one-third of the total installed capacity, an increase of about 4% YoY.

Main business analysis

Hydropower Business Segment

In the first half of 2023, the company's hydropower business achieved revenue of 1.48 billion yuan, a decrease of 55.97% YoY, accounting for 6.95% of the company's revenue. The net profit was 147 million yuan, a decrease of -111.91% YoY. The electricity sales were 5.623 million MWh, a decrease of 56.20% YoY. The average on-grid tariff of hydropower was 263.65 yuan/MWh, an increase of 1.36 yuan/MWh compared with the same period last year which was mainly due to the increase in the proportion of sales of electricity with relatively high electricity prices, which increased the average on-grid tariff of hydropower. The average utilization hours of hydropower generating units was 1,046 hours, a decrease of 1,333 hours compared with the same period last year. The company's hydropower plants are located in Hunan, Guizhou, Sichuan, Guangxi and other places. As of the end of 2022, the combined installed capacity of hydropower plants was 5,454 MW; the equity installed capacity was 3,396 MW, unchanged from the same period last year. Hydropower is the process of converting water energy into electrical energy through the establishment of hydropower stations, water conservancy hubs, and aviation power hubs. Compared with photovoltaic power generation and wind power, hydropower has a certain seasonality and is closely related to precipitation. Hydropower is a kind of clean and renewable energy that plays an important role in protecting the environment and reducing greenhouse gas emissions. In recent years, China's hydropower industry has been developing steadily. In the first half of 2023, the country's new hydropower grid-connected capacity reached 5.36 million kW. However, the reason for the decrease in hydropower revenue was that the average rainfall in the basin where the group's hydropower plant are located dropped YoY, resulting in a significant reduction in electricity sales. China is rich in water energy resources, and there is still great potential for the development of water energy resources in the future. Hydropower involves many upstream and downstream companies, which will inevitably lead to the coordinated development of the entire industry chain. The company is committed to the development of clean energy. At the same time, China has released a number of favorable hydropower-related policies in recent years. And precipitation in the second half of the year will increase, the company's hydropower revenue and net profit are expected to improve significantly in the second half of the year.

Wind power business segment

In the first half of 2023, the company's wind power business achieved revenue of 3.98 billion yuan, an increase of 63.31% YoY, accounting for 18.7% of the company's revenue. Net profit was 1.45 billion yuan, an increase of 69.7% YoY. Electricity sales were 8.346 million MWh, an increase of 65.42% YoY. As of the end of 2022, the combined installed capacity of wind power plants was 7,189 MW, an increase of 73.5% YoY; the equity installed capacity was 5,179 MW, an increase of 93.8% YoY. The average on-grid tariff of wind power was 476.73 yuan/MWh, a decrease of 6.14 yuan/MWh from the same period last year. It was mainly due to the fact that the average on-grid tariff of newly projects put into operation was lower than that of existing wind power projects, thus lowering the average on-grid tariff of wind power. The average utilization hours of wind power generators were 1,163 hours, an increase of 64 hours compared with the same period last year, mainly due to better wind resources compared with the same period last year. China is the world's largest wind power market, and it is expected that wind power policies will generally improve in the future. The company attaches great importance to the wind power business and develops the Integrated Intelligent Wind-and-Energy Storage Wind Power Project with an installed capacity of 250MW actively, achieving China Power's first breakthrough in the development of comprehensive intelligent wind power projects in Liaoning Province. At present, onshore wind has basically achieved on-grid tariff parity in 2021, and China has continuously released policies to benefit sea wind, such as the ൖth Five-Year Plan" for coastal provincial administrative regions; Europe and the United States have also aggressively made their efforts in sea wind projects, such as the United States` 2023 release of "Advancing U.S. Offshore Wind Energy: Achieving "Strategy to realize and exceed the target of 30 GW" 9 European countries signed the "Ostend Declaration", and countries around the North Sea will further develop the offshore wind power industry. The sea wind industry will be at a high level of prosperity in 2023, and the company's wind energy business is expected to continue to maintain a growth trend.

Photovoltaic power business segment

In the first half of 2023, the company's photovoltaic power generation business achieved revenue of 2.52 billion yuan, an increase of 25.56% YoY, accounting for 11.81% of the company's revenue. Net profit was 780 million yuan, an increase of 21.69% YoY, and photovoltaic power electricity sales were 6.015 million MWh, an increase of 32.97% YoY. The average on-grid tariff of photovoltaic power was 418.64 yuan/MWh, a decrease of 24.73 yuan/MWh compared with the same period last year. It was mainly due to the fact that a number of grid-affordable photovoltaic power projects of the group were put into operation, which lowered the average on-grid tariff of photovoltaic power. The average utilization hours of photovoltaic generator sets were 769 hours, a decrease of 56 hours compared with the same period last year. It was mainly attributable to the decrease in solar irradiance for photovoltaic power as compared with the corresponding period last year, as well as the commencement of operation of various distributed and household photovoltaic projects with relatively lower utilization hours. As of the end of 2022, the combined installed capacity of photovoltaic power plants was 7,207 MW, an increase of 38% YoY; the equity installed capacity was 5,608 MW, an increase of 46.5% YoY. The company's photovoltaic power business has experienced significant growth in capacity, output and revenue. Photovoltaic power essentially uses the photovoltaic effect of the semiconductor interface to directly convert light energy into electrical energy. China produced 806,000 tons photovoltaic polycrystalline silicon in 2022, an increase of 59% YoY. Mainland China is the main producer of silicon wafers and is showing a growth trend. According to the data from the National Energy Administration, as of the end of July, the installed capacity of solar power generation was approximately 490 million kW, an increase of 42.9% YoY. China Photovoltaic Industry Association predicts that domestic newly installed photovoltaic capacity will reach 95-120 GW in 2023 and 100-125 GW in 2025 respectively. It is expected that the cumulative installed capacity of photovoltaics will surpass hydropower for the first time in 2023, becoming the largest source of non-fossil energy power generation. Photovoltaics is a renewable energy industry which is strongly supported by the state. In recent years, national and local governments had continuously issued relevant policies to promote the development of photovoltaic power generation business to achieve on-grid tariff parity. The company has put a number of affordable grid-connected photovoltaic power generation projects into operation, such as Fishery and Photovoltaic Complementary Photovoltaic Power Generation Project with an installed capacity of 100MW is the first project to achieve full capacity power grid connection of the Lubei Saline-Alkali Tidal Flat Land 10 million kW-level Integrated Wind-Photovoltaic-and-Energy Storage Base. The Integrated Sand Control, Husbandry Promotion and Photovoltaic Power Generation Demonstration Project with an installed capacity of 100MW is a city-level key demonstration project. The project has significant environmental, economic and social benefits, and effectively integrates economic development with environmental protection. In the first half of 2023, the Xinrong Phase II 600MW Grid Parity Photovoltaic Power Generation Project of Datong CP Photovoltaic Company Limited, a subsidiary of the Company, achieved full capacity power grid connection, marking a new milestone of the Group in establishing its advantages in terms of industry cluster of green energy and bringing the Group's accumulated installed capacity in Datong City, Shanxi Province to 1,300MW. The above projects contributed to the sustainable development of the Group and China, and are expected to provide a total of more than 6,000,000MWh of clean electricity per year, which is equivalent to saving approximately 2,000,000 tonnes of standard coal and reducing approximately 5,500,000 tonnes of carbon dioxide emissions, thereby further improving the air quality in the locality. According to the seasonal characteristics of photovoltaic power, installed capacity may reach the peak of the whole year around the fourth quarter. Against the background of the Russian-Ukrainian war and climate transition, as a clean energy source, the photovoltaic industry will continue to be in a growth period, and the company's Photovoltaic power business will continue to grow.

Thermal power business segment

In the first half of 2023, the company's thermal power business achieved revenue of 11.71 billion yuan, an decrease of 5.58% YoY, accounting for 54.9% of the company's revenue, and net profit is 560 million yuan, an increase of 151.25% YoY. The decrease in revenue was mainly affected by the disposal of coal power. Excluding the impact of coal power disposal, thermal power revenue increased YoY. Coal-fired power sales were 2,670.2 MWh, a decrease of 11.67% YoY. Although it benefited from the increase in electricity demand during the period, the sale of shares of two coal-fired power subsidiaries (disposal of coal power) was completed at the end of last year, resulting in a decrease in power sales, excluding the impact of coal power disposal, coal power sales increased YoY and exceeded the national electricity consumption growth. Gas power sales were 95.2 MWh, an increase of 133.40% YoY. The average on-grid tariff of coal power was 402.68 yuan/MWh, an increase of 0.76 yuan/MWh over the same period last year; the average on-grid tariff of gas power was 654.12 yuan/MWh, an increase of 33.26 yuan/MWh over the same period last year. It was mainly due to the increase in the average selling price of one of the Group's gas-fired power plants after participating in electricity transactions in the Guangdong Provincial Power Grid Enterprise Procurement Market. The average utilization hours of coal-fired power generation units were 2,556 hours, an increase of 402 hours compared with the same period last year, which was mainly due to the YoY increase in electricity demand during the period, which led to a rebound in electricity consumption. The average utilization hours of gas-electric generation units were 2,060 hours, an increase of 531 hours compared with the same period last year, mainly due to the YoY increase in power demand during the period, which led to a rebound in electricity consumption. As of the end of 2022, the combined installed capacity of coal power plants was 11,080 MW, a decrease of 19.9% YoY; the equity installed capacity was 7,554 MW, a decrease of 16.4% YoY, also affected by the disposal of coal power. The combined installed capacity of gas power plants was 475.2 MW, an increase of 72.7% YoY; the equity installed capacity was 459.8 MW, an increase of 77% YoY. Benefiting from the growth in domestic power demand in the past two years, the company will put new coal-fired power generation units into commercial operation in 2022. At the same time, new gas-fired power projects will be also put into commercial operation, and thermal power sales have increased. Although the market has promoted the increase in the use of clean energy in recent years, and the proportion of thermal power has shown a certain downward trend, overall, China's current power generation method is still dominated by thermal power. At present, the market competition in the thermal power industry is very fierce, and the market share of each enterprise is not high. National Development and Reform Commission and the National Energy Administration have issued flexible thermal power transformation policies during the ൖth Five-Year Plan" period. The company has actively carried out engineering construction of new thermal power units and technical transformation projects of existing generation units. And the company is committed to providing clean and efficient thermal power. In the short term, thermal power business will still be the company's main source of income.

Energy storage business segment

In the first half of 2023, the company's energy storage business achieved revenue of 1.63 billion yuan, an increase of more than 16 times YoY. The company's energy storage business continues to expand, revenue has increased significantly, and net profit was 35 million yuan, an increase of 49.16% YoY. The company actively carries out scientific and technological innovation in the field of energy storage. Xinyuan Smart Storage launched the self-developed intelligent operation and maintenance platform for general centralized control of energy storage, which is the first 100MW-level energy storage and power station on the power grid side to be connected to the cloud platform through internet in China, as well as the first intelligent switching cluster-level management solution in the industry, marking a new breakthrough in the research and development of the core technologies of energy storage. The energy storage business mainly includes the sales of energy storage equipment, the provision of engineering contracting services for the development and assembly integration of energy storage integrated power stations, energy storage capacity leasing services, and energy storage power station charging services. Energy storage is an emerging industry, and the company's energy storage business is still in the early stages of growth. It is expected that with the rapid development of the energy storage market, the prospects for the energy storage business are optimistic. The company has diversified the development of energy storage projects and continued to expand overseas businesses, including signing strategic cooperation agreements with companies in Mexico, Australia and other places. Overseas markets have great potential. In the future, the company will speed up the establishment of overseas marketing teams and actively expand marketing channels to fully promote the development of overseas energy storage markets. As the business continues to expand, it is expected that the energy storage segment will continue to contribute to the revenue of the company in the future.

Valuation and recommendation

Xinyuan Jinwu commenced the construction of the first production line with comprehensive utilization of full color photovoltaic functional materials and obsolete photovoltaic modules in Tongzhou District, Beijing at the end of March 2023, which is currently under commissioning and trial run. Meanwhile, it has also achieved new progress in the technological innovation of full color photovoltaic. The first full color auto-powered photovoltaic signage system and street light lighting system have been put into operation under the road scenarios in Tongzhou District and Fangshan District for demonstration. Such systems are expected to be widely applied to provinces and cities nationwide and will hence promote rapid development of colored photovoltaic. Qiyuanxin Power focused on the development of holistic solution applicable to battery swap of unmanned mine trucks in mine sites, which has already been put into operation, in an active attempt to tap into the unmanned vehicles application market in respect of scenarios such as main routes to collection and distribution ports as well as in-port transportation. In addition, it has developed the first ¡§battery-swap station for unmanned heavy trucks¡¨ in Xinjiang, marking the first intelligent green mine model project in Southern Xinjiang. Meanwhile, with regards to innovative areas of motive battery transportation, new energy vessels and echelon utilization of motive battery, we actively applied for a number of national key research and development programs and projects in 2023, so as to constantly enhance the Group's technological innovation capability and its influence in the emerging energy industries with technological innovation and application demonstration as the main focuses.

The Group has actively participated in the market-oriented reform of the national power industry and enhanced research on electricity market policies and regulations, particularly in aspects such as trading of spot electricity, green certificate/green energy and carbon emission quotas. Keeping abreast of the reform, the Group maximized electricity sold through the market and expanded its market share by increasing its participation in market-power transactions. Subsidiaries in various provinces have also established their electricity sales centers to attract more target customers through the provision of quality services.

Acquisition: On July 26th, 2023, the company reached an agreement with State Power Investment Corporation Limited. The company agreed to make the acquisition conditionally, and State Power Investment Corporation agreed to sell to the company the shares of Beijing Company 55.15% equity and 100% equity in Fujian Company, Heilongjiang Company and Shanxi Company conditionally, these four companies belong to State Power Investment Corporation Limited. On July 26th, 2023, the company reached an agreement with State Power Investment Corporation Guangdong and China Electric Power. The company agreed to acquire the company conditionally, and State Power Investment Guangdong and China Power Energy agreed to sell 100% equity in the Jieyang company to the company conditionally. The acquisition of high-quality clean energy assets involved in the Acquisitions will further enhance the asset structure of the Company, firmly promote the implementation of the Company's new development strategy of transforming itself into a leading clean and low-carbon energy provider and represent a frog-leap step towards its strategic goal. Upon completion of the Acquisitions, it is expected that the proportion of the Company's installed capacity of clean energy will increase by approximately 6.9 percentage points. The Company will vigorously promote the development and commencement of operation of quality clean energy and strive to proceed the Acquisitions to completion as soon as possible within this year, which is expected to further improve the results and earnings per share of the Company.

The Company will promote the rapid implementation of large-scale new energy base projects and the two types of ¡§integrated¡¨projects (i.e. integrated source-grid-load-and-storage project and integrated multi-energy complementary project). An integrated intelligent zero-carbon power plant will be established with pooled management achieved through ¡§load-side management + distributed power source + energy storage¡¨. The Company will also fully leverage the function of the green power conversion and development center and make use of its internal and external resources to track the progress of green power conversion projects on a continuous basis and practically steer the implementation of the first batch of these integrated projects. Strengthening the top-level design of scientific research to unlock greater values of the emerging energy industries and technological innovation. The Company will step up its efforts in the research and development of advanced technologies to push forward the progress of electrochemical energy storage and compressed air energy storage projects in full steam, whilst actively applying for establishment of demonstration pilot projects of novel energy storage with the National Energy Administration. They will carry on developing the organization system of scientific research, and complete the collaborative works in relation to the establishment of green energy and low-carbon technology research institutes, endeavoring to achieve groundbreaking success in the application of nation-level scientific research projects in the coming future. They will also accelerate the expansion in emerging industries and markets by driving companies in the emerging energy industries such as Xinyuan Jingwu to quickly lock in their first batch of users and resources, so as to ensure its long-term contribution to the profits of the Group.

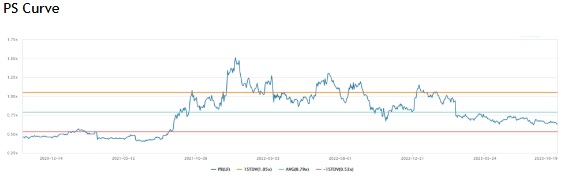

We predict that the company's revenue will be 46.31 billion yuan and 53.26 billion yuan in 2023-2024 respectively, with a compound annual growth rate of 10.41%, EPS will be 0.31/0.36 yuan, BVPS will be 4 and 4.3 yuan and P/B will be 0.67/0.63x, the company's average P/B in the past five years is about 0.67. In the first half of 2023, electricity consumption in the whole society will continue to grow, and it is expected that electricity consumption throughout the year will also increase relatively. The he precipitation has increased because of the rainy season in 2023. And the overall revenue from hydropower generation is expected to increase relatively. Favorable national policies for the wind power and photovoltaic industries are frequently issued recently. The company focuses on the transformation of the thermal power business. As for energy storage business, the company innovates and focuses on project development actively. It is expected that the company's profits will increase in 2023. Given that P/B will be 0.8 in 2023, we give the company a target price of HK$3.46, with a "accumulate" rating. (Current price as of November 1st)

Risk factors

Coal price changes, seasonal factors, photovoltaic component price changes, and national policies.

* The analyst has a financial interest in the listed corporation covered in this report.

�Financial

Click Here for PDF format...