Investment Summary

FY20's Results Grew by Nearly 40% against the Trend, and Q1 FY21 Results Rose by 116%

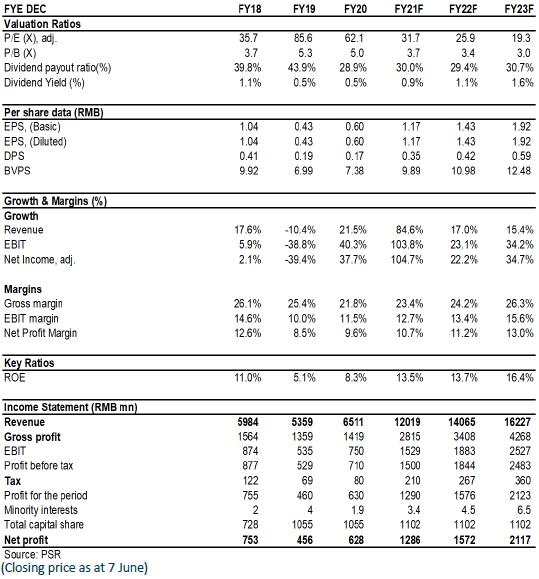

In 2020, Tuopu Group reported operating revenue of RMB6.51 billion, up by 21.5% yoy; net profit attributable to the parent company was RMB630 million, up by 37.7% yoy; earnings per share was RMB0.60. Dividend per share was RMB0.172, with a dividend payout ratio of 28.7%. Although the industry was hit by the COVID-19 pandemic in H1 of 2020, the Company's revenue grew against the trend and was significantly better than the industry average. This is mainly because the Company has been actively engaged in the field of lightweight chassis for new energy vehicles and automotive electronics in recent years. The transformation effect has gradually appeared. The increment brought by Tesla's localization project made an obvious contribution, and the transition period in the same period last year brought a relatively low base. Specifically, the revenue of shock absorbers, interiors, chassis, and automotive electronics increased by 9.3%, 34.8%, 27.0%, and 39.6%, respectively to RMB2.56 billion, RMB2.22 billion, RMB1.33 billion, and RMB180 million, respectively.

In the first quarter of 2021, benefiting from the strong industry rebound and the continued sales volume of Tesla models, Tuopu Group reported operating revenue of RMB2,426 million, up by 100.8% yoy. Net profit attributable to the parent company was RMB246 million, up by 116.4% yoy. The net profit was in the upper limit of the interval of the Company's previous result forecast (RMB220 million to RMB260 million).

Gross Margin Fluctuated Due to Accounting Standard Adjustments and Rising Raw Material Prices

In 2020, the Company recorded a 22.7% gross margin, down by 3.6 ppts yoy. The gross margin declined by 3.14 ppts, mainly due to the fact that under the new accounting standards, RMB197 million of transportation and storage expenses related to sales of goods was included in operating costs. Without consideration of such factor, the actual gross margin dropped by 0.58 ppts to 25.7%.

In the first quarter of 2021, the Company's gross margin was 21.9%, down by 5.4 ppts yoy. In addition to the changes in accounting standards, we estimate that part of the reason was the increase in raw material prices in the first quarter. We expect that as new production capacity continues to climb, the gross margin will improve yoy.

In the same way, the period expense ratios in 2020 and the first quarter of 2021 decreased by 3.96 ppts and 7.3 ppts yoy, respectively, due to 1) accounting factors and 2) high revenue growth, which led to the dilution of the expense ratio. In the end, the Company's net profit margin rose by 1.1 ppts and 0.81 ppts, respectively yoy.

Downstream OEM Clients` Momentum and the Tier-0.5 Strategy Open up Room for Growth

In recent years, on the basis of the original business of shock absorbers and interior functional parts, the Company has proactively arranged the module of the lightweight chassis system and the automotive electronics business as the future Ŗ+3" strategic development projects, in order to adapt to the trend of electrification, intellectualization and lightweight of vehicles.

Relying on its excellent vehicle synchronisation R&D capabilities, strategic forward-looking arrangement and other comprehensive factors, as well as early binding of strong downstream customers, the Company has begun to enter the order harvesting period and continued to steadily expand its market share. The Tier 0.5 strategy pioneered by the Company has achieved demonstrative success. The matching amount of single vehicles was relatively high. New orders have increased significantly compared with previous years, which provides guarantee for the Company's rapid and sustainable development in the future.

To meet the demand for orders, the Company accelerated the construction of Xiangtan base, Ningbo Hangzhou Bay New Area base Phase II and Phase III, and Ningbo Yinzhou District production base. In 2021, the Company will complete the construction of 1,500 mu of factory under construction and start the planning of the next 1,500 mu of industrial park.

In addition, in 2020, the Company's business was extended to the new energy vehicle thermal management relying on the technical homology of electronic control and related precision manufacturing capabilities in the IBS process of the automotive electronics business in the previous period. At present, the Company has successfully developed products such as heat pump air conditioners, electronic expansion valves, electronic water valves, electronic water pumps, and gas-liquid separators. In the future, the Company is expected to become an overall solution provider in the new energy vehicle thermal management. The overall matching value of single vehicles is as high as RMB6,000 to RMB 9,000. We expect that the Company will continue to benefit from the trend towards electrification and intellectualization of vehicles and enter a stage of rapid growth.

Investment Thesis

We revised the estimate that the company's net profit in 2021/2022/2023 will reach RMB 1286/1572/2117 million, respectively, with the corresponding EPS being RMB 1.17/1.43/1.92. We are optimistic about the development prospects of the company's lightweight business and automotive electronics. So, we lift the Company's target price to RMB46.1, respectively 40/32/24 x P/E, 4.7/4.2/3.7 x P/B for 2021/2022/2023, a "BUY" rating. (Closing price as at 7 June)

Risk

Price war among peers

Raw material price increase

New business risk

Financials

Click Here for PDF format...