|

DATANG RENEW(1798)

Analysis¡G

The business performance of China Datang Corporation Renewable Power (1798) improved significantly in the first quarter of 2021. Its revenue grew 40.9% to RMB3.363 billion compared to the same period last year and net profit attributable to shareholders surged 152.8% to RMB1.212 billion. In the first quarter, the total power generation of the Group amounted to 7,524,552 MWh, representing an increase of 38.23% compared with that of the corresponding period of 2020, of which, the wind power generation amounted to 7,347,725 MWh, representing an increase of 36.81%; the photovoltaic power generation amounted to 172,340 MWh, representing an increase of 158.76%. Going forward, the Group will speed up the layout for and development and construction of large-scale new energy bases with an integration of wind power, photovoltaic power and energy storage, concentrate on the development of project resources in areas with clean energy advantages, and accelerate the integration into the new development pattern for optimization of the national energy supply and demand structure, promoting high-quality development of the Group. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $1.68, Target Price: $1.95, Cut Loss Price: $1.55

|

TSINGTAO BREW(168)

Analysis¡G

Tsingtao Brew (168) is mainly engaged in the production, sales and domestic trade of beer. The company recently announced its 21Q1 results. The company`s 21Q1 revenue was RMB 8.93 billion, up by 41.9% yoy. The 21Q1 net profit attributable to the parent was RMB 1.02 billion, up by 90.3% yoy, and up by 26.6% comparing to 19Q1. The result beats expectation. The sharp increase in the company`s 21Q1 GPM can fully demonstrate that the company can maintain its profitability through cost control, price increase, and structural upgrade. Therefore, we believe that the expected increase in raw material costs will have a relatively small negative impact on the company as a whole.

Strategy¡G

Buy-in Price: $70.00, Target Price: $77.00, Cut Loss Price: $66.00

|

|

Xtep Int`l - (1368 HK) - Brand got attention after the Xinjiang Cotton event, and the company's valuation discount narrowed

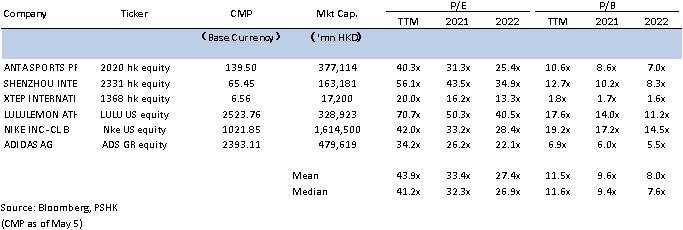

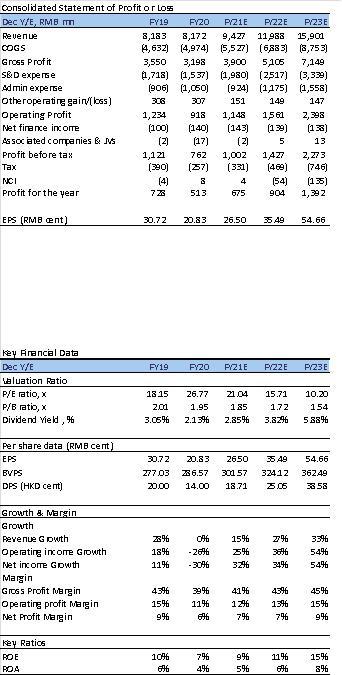

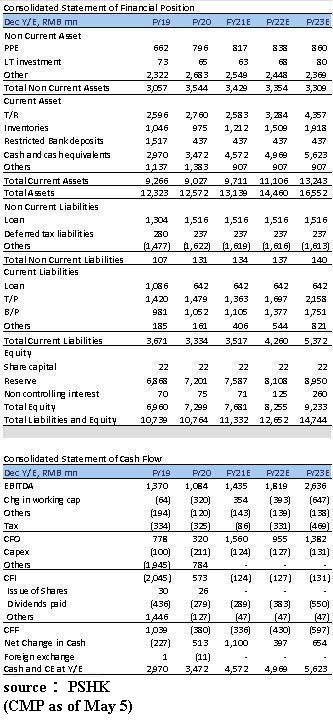

Investment SummaryXtep's main brand's retail sales (including online and offline channels) recorded an increase of approximately 55% in Q1. The discount level and inventory level have continued to improve quarterly. The retail inventory turnover period has been shortened to approximately 4.5 months, which is in line with our expectations. The company's recent valuation discounts with leading sportswear companies have continued to narrow due to the continued outperforming operating performance of its peers and the Xinjiang cotton event. The main brand's performance in 2021 further improvesXtep International announced on April 15 the operating status of Xtep's main brand in Q1. The retail sales growth of the main brand recorded a growth of about 55% compared with the same period last year, in line with our expectations, mainly due to the low base last year. Compared to 2019, it recorded a MDD growth, which was better than its peers (Anta Q1 vs 2019: LDD). By channel, online channels increased by 70% Yoy, and offline channels increased by 40% Yoy. Both retail discounts and inventory cycles have improved. Retail discounts range from 25% to 30%. Retail inventory turnover is about 4.5 months, returning to pre-epidemic levels on a quarterly basis. Xinjiang Cotton eventThe outbreak of the Xinjiang cotton event started on March 24. A Weibo about H&M not cooperating with any garment manufacturing factory in Xinjiang or purchasing products or raw materials from the region attracted the attention of mainland netizens. At the end of September last year, the United States passed the " Uyghur Forced Labor Prevention Act," and the Better Cotton Initiative (BCI) subsequently launched an initiative to boycott Xinjiang cotton. Many BCI members had already made a statement regarding the deactivation of Xinjiang cotton in September last year. At the end of March, the Chinese Communist Youth League's Weibo posts and reports from mainland official media initiated a series of boycotts in the mainland. The affected brands include approximately 200 brands, including international brands such as Nike, Adidas and PUMA. From the sales data of Tmall, the sales volume of domestic sports brands such as Anta, Li Ning and Xtep all recorded substantial growth in the week following March 24. Use rate of domestic brands increases, Xtep 160x series is recognized by professional runnersIn the Xiamen Marathon held on April 10, the use rate of domestic brands rose sharply. Among the runners completed within 3 hours, about 69% of the runners wore domestic brands. Domestic brands surpassed international brands for the first time, and Xtep ranked first with the 51% use rate, and Nike, which used to be the number one, dropped from 70% last year to 26%. Among the top 9 players who finished the race, 7 players used Xtep 160x PRO, reflecting the recognition of the company's running shoes in the professional market. 160x PRO is a new product launched by Xtep in March this year. It has been improved and upgraded on the basis of 160x. At the same time, 160x 2.0 and 300x 2.0 were also launched, all referred to as the second generation of 160x. Xtep's investment in technology R&D has increased Yoy in recent years to strengthen the performance of its products in the running profession. Valuation and investment adviceThe company's Q1 was in line with our expectations. Under the influence of the epidemic last year, the company's development of new brands was postponed. The sales and inventory levels of the main brands improved quarterly, while maintaining better performance than other peers. It is expected that the company will be able to cultivate its new brands more effectively after the opening of the new operation center in Shanghai in 2021. With the Xinjiang cotton event, the company's brand has received a lot of attention from the market, and the company's valuation discount with industry leaders has narrowed significantly. The Xinjiang cotton event brought a short-term sales impact to domestic sports brands, which is a one-off event, but at the same time, it also provides a customer experience opportunity for domestic products. Quality products can eventually attract users to continue using them. In the past years, the company has continued to deepen the field of running, and it has also been recognized by users in the practical use environment. We maintain our previous expectations. We expect the company's EPS for FY21/FY22 to be RMB 26.50/35.49 cents. We raise our target price to HK$7.79 (previously RMB 4.49), and raise the forecast P/E for FY 2021 to 25x (previously: 16x), Corresponding to FY21E/FY22E P/E of 25.00x /18.66x, maintain the Accumulate rating. (Current price as of May 5) Peer comparison

Financial

Click Here for PDF format...

| Recommendation on 7-5-2021 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 6.560 | | Suggested purchase price | N/A | | Target Price | $ 7.790 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2021 Phillip Securities (HK) Ltd. All Rights Reserved.

|