Investment Summary

Gross Profit Margin Rose QoQ

According to the (unaudited) report for Q3 2020 disclosed by the Company, in the first three quarters, Sanhua recorded a revenue of RMB8,593 million, down 0.32% yoy, and a net profit attributable to shareholders of the listed company of RMB1,092 million, up 3.4% yoy. Specifically, the Company in Q3 reported a revenue of RMB3,275 million, up 17.40% yoy, and a net profit attributable to shareholders of the listed company of RMB449 million, up 23.51% yoy. The gross profit margin in the first three quarters was 28.69%, which was basically the same yoy. In Q3, the gross profit margin was 30.14%, a slight increase of 0.5 ppts yoy, and an increase of 1.14 ppts qoq. In Q3, the revenue of the Company's electric refrigeration and air conditioning parts business and auto parts business was approximately RMB2.63 billion and RMB650 million, respectively, an approximate increase of 10% and 50% yoy. The Company's outperformance in downstream sales volume and the improvement in product mix played a positive role in the recovery of profitability. The Company had good control on expenses. In the first three quarters, the period expense ratio was 15.09%, up 1.45 ppts yoy. Specifically, the financial expense ratio was 0.47%, up 0.83 ppts yoy, which was mainly affected by exchange gains and losses. The Company's net profit margin in Q3 reached 13.70%, up 0.68 ppts yoy.

The Company Continuously Obtains New Orders and New Energy Business Is Boosted Again

According to an announcement, Sanhua has recently won orders from several well-known customers:

1) The Company became the exclusive supplier of multiple thermal management valve products on the e-Platform of Fudi Technology under BYD, with cumulative sales of nearly RMB500 million in the five-year life cycle. The relevant models are expected to be mass-produced in 2021;

2) The Company was identified as the exclusive supplier of integrated thermal management components for GM's large-scale electric vehicle platform in North America, with sales expected to exceed RMB900 million;

3) The Company was identified as the exclusive supplier of products such as electronic expansion valves and integrated thermal management modules for the core platform for electric vehicles of SAIC Motor, with cumulative sales of more than RMB1 billion in the life cycle. The relevant models are expected to be mass-produced in 2022.

We believe that the Company's continuous receipt of orders from leading OEMs since 2017 has verified that its thermal management products and system capabilities have been continuously recognized. In the next 5-10 years, the Company will continue to focus on heat pump-related products for its new energy vehicle parts business. Compared with the PTC mode, the heat pump mode can reduce the power consumption by 2/3, which can greatly increase the cruising range. The Company has currently maintained a high capacity utilization rate and production-sales ratio. With the rapid development of the new energy vehicle market, the Company is expected to usher in a period of explosive growth of new orders.

Raising Funds for Production Expansion Facilitates the Development

In order to expand the commercial refrigeration market, the Company plans to issue convertible bonds to raise funds amounting to RMB3 billion, which will be used to increase commercial refrigeration production capacity. It includes a construction project with an annual output of 65 million sets of intelligent control components for commercial refrigeration and air conditioning, and a technical renovation project with an annual output of 50.5 million sets of high-efficiency and energy-saving refrigeration and air-conditioning control components. The construction period is six years and four years, respectively. The new expansion project will help the Company expand the product line, optimize the product mix and increase the revenue and profitability in the future. Commercial refrigeration products have a higher gross profit margin. If domestic substitution can be achieved, the Company's competitiveness will be consolidated.

Investment Thesis

Sanhua is the leading company of refrigeration parts and components with obvious technical advantages in its products. The thermal management of new energy vehicles, dishwashers and cold-chain logistics are all promising business areas in line with the general direction of social development in the future. We expect that the Company's home appliance business will benefit from the market share increase year by year. There is a broad market for the thermal management of new energy vehicles in the future. Under a clear pattern of dual-driven growth, the Company is entering a period of realizing high growth of result.

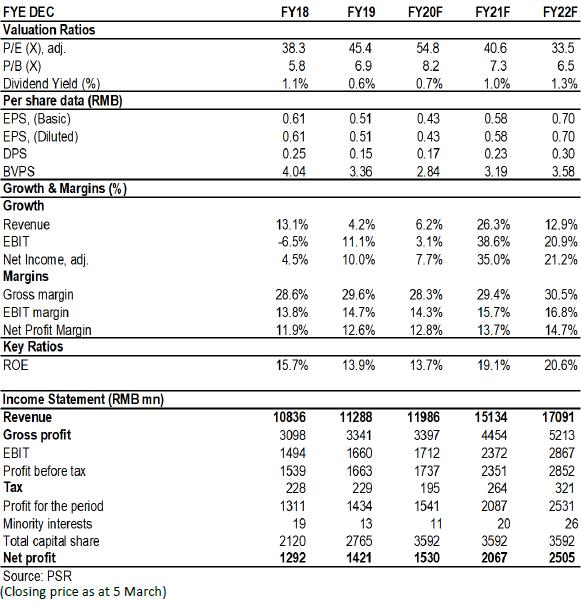

As for valuation, we expected diluted EPS of the Company to RMB0.43/0.58/0.70 of 2020/2021/2022. And we accordingly gave the target price to RMB26.7, respectively 63/46/38x P/E for 2020/2021/2022. "Accumulate" rating. (Closing price as at 5 March)

Risk

Progress of new production line is below expectations

Electric vehicle sales fall short of expectations

Macroeconomic downturn affects product demand

Sharply rising raw material prices or sharply falling product prices

Financials

Click Here for PDF format...