Investment Summary

Private traffic management is the main trend for offline merchants

Take Tencent as an example. Tencent itself focuses more on WeChat payment and advertisement business, while its e-commerce SaaS services mainly choose to cooperate with third-party SaaS platforms. Therefore, the rapid development of social e-commerce platforms has provided huge business opportunities for third-party SaaS platforms. we believe that for merchants who already have enough user traffic of repurchase, it is more appropriate to open an online store through a third-party SaaS platform for private traffic management. Effective private traffic management can increase customer repurchase rates and reduce Customer acquisition cost. At the same time, since the growth of traditional e-commerce users has obviously reached a bottleneck and the cost of public traffic is high, it is especially important for small and medium-sized businesses to have their own fixed customers and to manage them efficiently under private traffic management.

The company focuses on product development and strives to improve user experience and renewal rate

We believe that for SaaS product providers, their future growth potential is closely tied to product R&D capabilities. Strong R&D capabilities are one of the main moats for SaaS product providers. The company clearly understands the importance of having a strong R&D system, so its investment in R&D is extremely high. The company's R&D expenses in 2019 were RMB 404 million, and the R&D expense ratio was 34.6%. As the company has more and more SaaS products, the rapid increase in SaaS revenue can bring obvious marginal effects, and the R&D expense ratio is expected to gradually fall. Relying on a strong R&D system and investment, the company can continuously polish its products according to the merchants` feedback. Thereby, increasing the user experience and merchant's renewal rate. Further, the company's strategy of targeting mid-top tier merchants will also increase the company's future merchants` renewal rate. We believe that maintaining a high renewal rate is particularly important for SaaS product providers. The renewal rate has a critical impact on the company's revenue and profit ends. The continuous optimization of the renewal rate can effectively increase the company's SaaS business revenue and reduce the company's overall sales expense rate. The company's 2019 merchant renewal rate was 45%, with a huge upward potential in the future.

Valuation and investment thesis

Since the company is still in the early stages of development and has not yet recorded a profit, we use the PS ratio to value the company. We are giving the company a 2022 target PS of 25x. Taking into account that the company's listed entity currently holds 51.9% of the shares of Qima Technology (Youzan's operating body), we give the company a 10% control premium, and the 24-month target price is HKD3.96, with respective 2020/2021/2022 PS (51.9% of revenue) at 63.7x/39.8x/27.5x. We initiate with a Buy rating. (Market closing price as of 6 Jan) (exchange rate: RMB 0.88/HKD)

Risks

1) The company is listed on HKEX GEM board, which may have higher risk and volatility comparing to stocks listed on HKEX main board 2) The expansion of SaaS customers is worse than expected 3) The increased industry competition 4) GMV increase less than expected 5) Merchants renewal rate less than expected.

Industry Review and Forecast

China's e-commerce industry

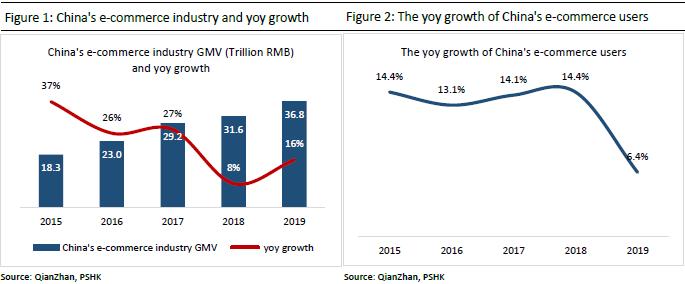

China's e-commerce industry is now mature and its growth is slower than before. The growth of traditional e-commerce users, led by Tmall, JD.com, and Vipshop, has significantly slowed down, which means that competition in the industry has become increasingly fierce and customer acquisition costs have become higher. According to data from the Qianzhan Industry Research Institute, China's e-commerce GMV and users increased by 13.1% and 6.4% yoy in 2019, respectively, and these growth rates were significantly slower than the 36.6% and 14.4% in 2015. The noticeable slowdown in user growth coupled with the gradual increase of merchants on traditional e-commerce platforms has led to intensified competition among merchants to a certain extent. The cost of user traffic for traditional e-commerce platform has risen sharply, putting a certain amount of pressure on small and medium-sized merchants and long-tail merchants.

China's social e-commerce industry

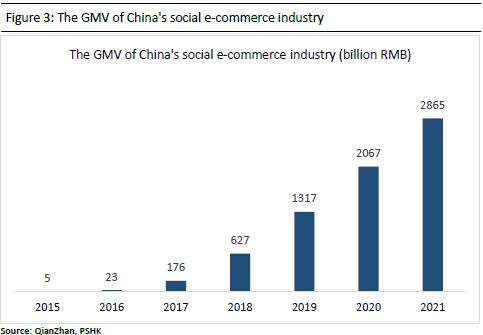

In today's mobile Internet era, social platforms Apps represented by WeChat have huge user traffic and occupy most of the user's online time. Take WeChat as an example. As of 2019, WeChat has 1.165 billion monthly active users, and the huge user traffic of WeChat has greatly reduced the cost of customer acquisition for its social e-commerce. On the other hand, other functions in the WeChat ecosystem such as WeChat Payment etc. also provide good technical support for its social e-commerce platform. At present, WeChat has created its unique social e-commerce ecosystem through decentralized innovation and breaking the traditional e-commerce model, allowing small and medium-sized enterprises to quickly expand their business and user base, while directly controlling and managing their customer data and customer relationships. According to the Zhiyan Consulting Report, the GMV of China's social e-commerce industry has increased from RMB 4.69 billion in 2015 to RMB 1.32 trillion in 2019, and is expected to reach RMB 2.86 trillion in 2021.

The differences between social and traditional e-commerce

We believe that e-commerce shopping can be divided into two major stages, the demand stage and the purchase stage. In the demand stage, traditional e-commerce is dominated by search shopping, so user consumption is typically planned consumption. On the contrary, part of social e-commerce shopping are unplanned consumptions, such as product sharing in Wechat's Moments to stimulate users` desire to consume. In the shopping phase, the consumption conversion rate of traditional e-commerce is lower than that of social e-commerce. The main reason is that the trust mechanism of social e-commerce (recommendation by friends) is more credible than traditional e-commerce user reviews, so that consumption can be quickly promoted on social e-commerce platforms.

In addition, in the case of abundant supply of goods, the ranking of items will have an extremely important impact on traditional e-commerce consumers. Consumers generally choose items with higher rankings, so the centralized characteristics of traditional e-commerce (traffic flow in from one entrance, the platform) makes the user traffic continuously converge to the high ranking items. In this case, product marketing and advertisements become especially important. On the other hand, social e-commerce (decentralized), doesn`t has the characteristic of user traffic asymmetric, because in the case of friend recommendation, consumers` trust in friends will reduce their dependence on ranking and brand, causing products more likely to get their user traffic equivalent to its price-performance ratio. Therefore, we believe that social e-commerce is more friendly to long-tail products and small and medium-sized businesses, while traditional e-commerce is more focused on top products. We believe that the application scenarios of the two e-commerce models in the future will be different.

Private traffic management is the main trend for offline merchants

Take Tencent as an example. Tencent itself focuses more on WeChat payment and advertisement business, while its e-commerce SaaS services mainly choose to cooperate with third-party SaaS platforms. Therefore, the rapid development of social e-commerce platforms has provided huge business opportunities for third-party SaaS platforms. The third-party e-commerce SaaS platforms help offline merchants to build their online stores on social platforms (such as WeChat) and provides services such as online products transactions, order management, online payment, and user management. For offline merchants, compared to opening a store on traditional e-commerce, the third-party SaaS platform provides store opening services with two major advantages.

1) The private traffic management of social e-commerce is more effective. Through third-party SaaS platform to open a store in the social e-commerce (such as opening a store on WeChat), the offline merchant can directly manage and interact with their consumers. On the other hand, if a merchant opens a store in a traditional e-commerce platform, it cannot directly manage its consumers. Since the traditional e-commerce platforms control the user traffic, hence the buyers can only reach the merchants` good through the search engine. Therefore, it is more effective for businesses to manage private traffic in social e-commerce platforms.

2) Since third-party SaaS platforms do not need to provide merchants with strong user traffic like the traditional e-commerce platforms do, the fees charged by third-party SaaS platforms for opening stores and selling products on social e-commerce platforms will also be less than the traditional e-commerce platform. Take Tmall as an example. Tmall merchants need to pay an annual fee of RMB 30,000-60,000 and a sales commission of 2%-5%, while China Youzan (the leading third-party SaaS platform in the industry) only charges a minimum of RMB 6,800 annual SaaS service fee.

Based on the above reasons, we believe that for merchants who already have enough user traffic of repurchase, it is more appropriate to open an online store through a third-party SaaS platform for private traffic management. Effective private traffic management can increase customer repurchase rates and reduce Customer acquisition cost. At the same time, since the growth of traditional e-commerce users has obviously reached a bottleneck and the cost of public traffic is high, it is especially important for small and medium-sized businesses to have their own fixed customers and to manage them efficiently under private traffic management.

The top tier third party SaaS providers are likely to be the beneficial from the launch of ¡§Wechat small stores¡¨

In June 2020, Tencent launched ¡§small WeChat store¡¨, a small program designed to help small businesses open online stores for free. But since it only offers basic SaaS services for free, hence its main customers are the relatively small SMEs. On the contrary, the main customers of leading third-party SaaS providers in the industry (such as Weimob and Youzan) are the relatively large SMEs. The free function ¡§small WeChat stores¡¨ offers are incompatible with the needs of the large SMEs. We believe the ¡§small Wechat stores¡¨ will gradually eliminate the low tier third-party SaaS providers, making the industry gradually concentrated, which is beneficial to the industry's leading third-party SaaS providers. In addition, the free SaaS services provided by ¡§WeChat small stores¡¨ can encourage small SMEs to adapt to the current digital trend and grow rapidly from it. When these small SMEs take shapes, the free SaaS services no longer fulfill their requirements, they are expected to become potential new customers of the top tier third-party SaaS providers in the industry.

Company Overview and its Competitive Advantages

The leading social e-commerce store SaaS service provider in China

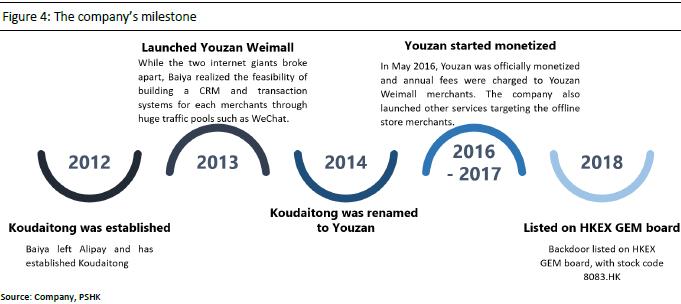

Baiya (formerly known as Zhu Ning) established Koudaitong (Previous name of Youzan) in November 2012. Prior to the establishment of Koudaitong, Bai Ya worked for Alipay under Alibaba as the chief product designer and other positions, and he has extensive experience in the internet community, e-commerce, online payment and other sectors. In the initial stage of its establishment, Koudaitong mainly helped Taobao merchants to initiate business in the WeChat ecosystem. On 22th November, 2013, in order to take control of all the traffic entrances, Taobao has blocked the access from WeChat. At the same time, WeChat users could not directly access Taobao through WeChat. While the two internet giants broke apart, Baiya realized the feasibility of building a CRM and transaction system for each merchant on platforms with huge user traffic such as WeChat. In December 2013, Koudaitong launched Youzan Weimall, and Koudaitong was renamed to Youzan in November 2014. In May 2016, Youzan officially monetized and annual fees were charged to Youzan Weimall merchants. In the early days of the monetization, Youzan was questioned by many merchants, but soon the merchants realized that the GMV increase brought by Youzan Weimall far exceeded the annual service fee charged by Youzan. In 2017, the company released Youzan Retail, Youzan Beauty, Youzan Catering and other services for offline store merchants. In 2018, the company was backdoor listed on the Growth Enterprise Market of the Hong Kong Stock Exchange with the stock code 8083.HK. In the same year, the company teamed up with Kuaishou to launch the "short video e-commerce shopping guide" solution. At present, the company provides powerful SaaS systems with omni-channel operations and integrated new retail solutions, applying PaaS cloud service to create business customization options, while providing extended services such as Youzan Guarantee, Youzan Distribution, Youzan Promotion, etc. As of September 30, 2020, the company has 97,875 paying merchants.

The company's diversified SaaS products

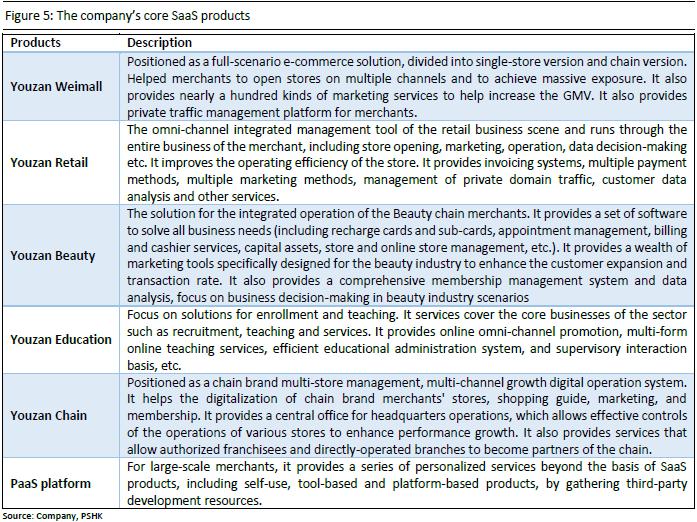

The company's core products mainly serve the business clients, including Youzan Weimall, Youzan Retail, Youzzan Beauty, Youzan Education and etc. Below are the descriptions of these products.

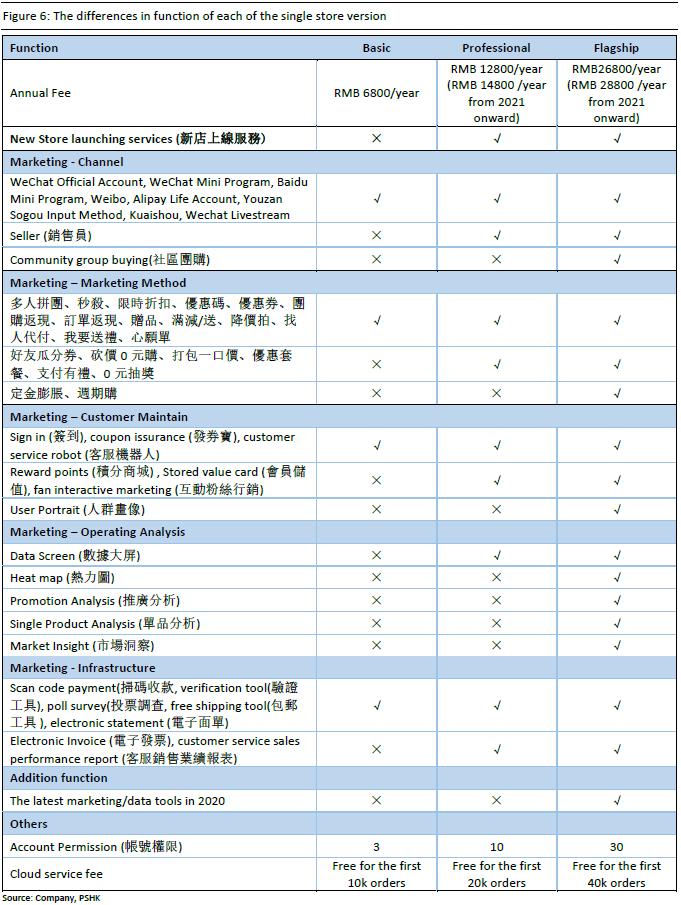

Youzan Weimall is the flagship product among the company's all SaaS products. It is divided into single store version and chain version. The single-store version includes basic version, professional version and flagship version, with annual fee of RMB 6800, 12800 (14800 from 2021 onward), and 26800 (28800 from 2021 onward) respectively. As for the customized version for large merchants, the annual fee ranges from hundreds of thousands. Merchants can subscribe to the appropriate version according to their own scale and needs. The basic version is more suitable for individuals or operation teams with less than three people, the professional version is more suitable for growing e-commerce or store merchants, while the flagship version is more suitable for businesses with a certain scale and operate in multiple business scenarios. In addition, the higher grade the version is, the more the functions it provides. The following are the differences in function of each of the single store version.

The company's diverse extended services and transaction services

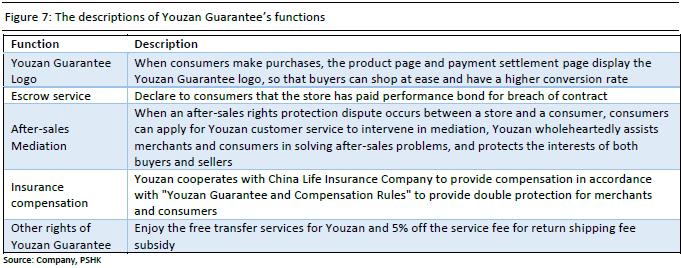

The company currently holds an internet payment license, so it is capable to provide customers with payment, loan, guarantee and other financial services. Youzan Guarantee is one of the most popular services among merchants. Youzan Guarantee provides endorsement services for customers and help merchants to increase their conversion rates. Due to the weak credibility on social ecosystem, the conversion rate of unfamiliar purchases is low. Generally, the conversion rate of non-fans is less than 1%. Many buyers refuse to trade because of concerns about the quality of goods and after-sales services. Youzan Guarantee can increase the creditworthiness of the social ecosystem and increase the purchase conversion rate for merchants. Youzan Guarantee charges 0.5% of the merchant's GMV as a service fee. If the merchant does not generate any transactions during the business period, Youzan Guarantee does not charge any fees. The followings are the descriptions of Youzan Guarantee functions.

In addition to Youzan Guarantee, Youzan also provides financial services such as 1) fast payment collection, 2) Youzan transfers, and 3) installment payments. Fast payment collection improves liquidity for merchants. After the order is shipped, the factoring company provides financing services for the merchant (a certain percentage of the transaction amount) before the consumer confirms the receipt. After the buyer receives the goods and the seller receives the payment, the merchant will return the financing amount. Through the time differences, the merchants can recover the payment in advance and accelerate their capital turnover. The charge from Youzan for fast payment collection is generally 0.5% of GMV. 2) Youzan transfers allow merchants to transfer payment to meet the need of merchants to transfer funds to other merchants and pay wages to employees. The handling fee charged for Youzan transfer is RMB 1 per transfer. 3) Installment payment can reduce the financial pressure of buyers to purchase high-priced goods and increase the purchase conversion rate. The company charges 0.5%-1.3%/month as an installment fee.

On the other hand, the company also provides a variety of non-financial/insurance extension services, such as 1) Youzanke and 2) Youzan distribution. 1) Youzanke is a product promotion platform launched this year. Currently, it has access to multiple traffic platforms such as WeChat and Kuaishou. Through Youzanke, merchants` products can be connected to different influencers (KOL), and KOLs can also select products that match their fan characteristics through the platform and carried out live streaming e-commerce business (ª½¼½±a³f) in exchange for for part of the GMV as a commission share. The company, who acts as the technical platform of Youzanke, charges 10% of the commission as revenue. The GMV of Youzanke is growing rapidly every month. The GMV in September is about 8 times that of January. 2) Youzan Distribution provides a distribution market that allows merchants with inventory but lack traffic to connect with merchants that lack inventory but with sufficient traffic. Thereby driving the overall GMV of the merchants. The company generally charges 1%-5% of GMV as a service fee.

Youzan Weimall is connected to multiple traffic platforms, hence merchants can open stores online on multiple channels

The company's Weimall has the advantage of multiple platforms. Currently, it has cooperated with multiple traffic platforms such as WeChat, Kuaishou, Baidu, Weibo, Momo, Alipay, QQ, Douyu, Xiaohongshu and etc. In addition, merchants can access live streaming platforms such as Kuaishou Live Broadcast and Momo Live Broadcast to stimulate the store's GMV, through Youzan Selling Assistant (¦³ÃÙ½æ³f§U¤â). We believe that in the current era of the rise of private traffic management, due to the different user profiles and characteristics of each traffic platform, the company's multi-platform layout can more easily meet the strong demand of merchants for multi-platform store opening and diversified marketing. For example, for merchants selling cosmetics, their female cosmetics can be marketed on platforms that are female oriented (such as Xiaohongshu). At the same time, for the male cosmetics, the merchant can choose to cooperate with a well-known KOL with mainly male fans for live streaming e-commerce (ª½¼½±a³f) on Kuaishou. In this way, merchants can enjoy a higher advertising conversion rate, which drives the increase of GMV. On the other hand, for Youzan, diversified traffic platform cooperation can reduce the company's excessive dependence on a single platform.

The company focuses on product development and strives to improve user experience and renewal rate

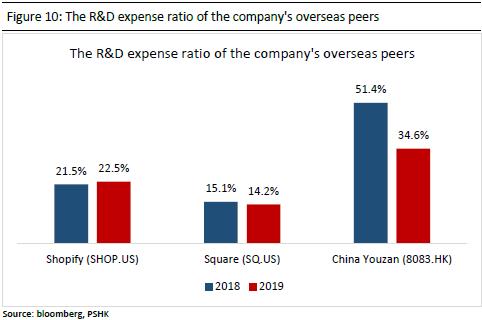

We believe that for SaaS product providers, their future growth potential is closely tied to their product R&D capabilities. Strong R&D capabilities is one of the main moats for SaaS product providers. The company clearly understands the importance of having a strong R&D system, so its investment in R&D is extremely high. As of the end of 2019, the company has more than 1,000 technical personnel, accounting for 36% of the total number of employees. On the other hand, the company's R&D expenses in 2019 were RMB 404 million, and the R&D expense ratio was 34.6%. As the company has more and more SaaS products, the rapid increase in SaaS revenue can bring obvious marginal effects, and the R&D expense ratio is expected to gradually fall. Comparing with its overseas peer Shopify (SHOP.US), as Shopify's SaaS business is relatively mature, although its R&D investment has continued to grow in recent years, the R&D expense ratio can still remain stable at about 20%.

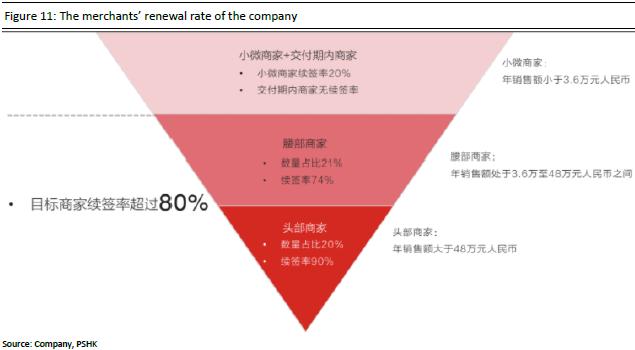

Relying on a strong R&D system and investment, the company can continuously polish its products according to the merchants` feedback. At present, the company conducts dozens of functional iterations on its products every month according to the needs of the merchants, and regularly publishes feedback of merchants for the products, as well as the current development progress of the functions built to target the needs of merchants. The company's active interaction with merchants and the ability to meet their needs in real time can effectively allow it to establish long-term partnerships with merchants, thereby increasing merchant renewal rates. As of the end of 2019, the renewal rate of the company's top-tier merchants (annual GMV exceeding RMB 480,000) was as high as 90%. But the renewal rate of small merchants (annual GMV less than RMB 36,000), due to their poor payment ability, was only 20%. Hence the company's overall merchants` renewal rate was only 45% in 2019. However, we believe that the company intends to mainly focus on expanding its proportion of top-tier and mid-tier merchants (annual GMV higher than 36,000). Although the cost of acquiring top and mid-tier merchants is relatively high. Nonetheless, due to the longer life cycle, higher willingness to pay and higher renewal rate of these merchants, the company's SaaS business is expected to become more stable afterward. We believe that in the future, with the gradual effectiveness of the high-mid tier merchants expansion strategy, the renewal rate is expected to reach a higher level.

We believe that maintaining a high renewal rate is particularly important for SaaS product providers. The renewal rate will directly affect the ability of SaaS product providers to achieve profitability. SaaS product providers generally sell products through agents, and for products sold by agents, agents can get part of the sales as sales commissions. Youzan is no different, with most of its SaaS products` sales conducted through agents. The commission share given to agents are accounted in the selling expenses. With that being said, compared with new merchants, the commission share ratio for renewing merchants is lower. According to management, the commission points for new customers are currently 40%-60%, while the commission share for renewing customers is generally 10-15ppts lower than that of new customers. Therefore, the renewal rate has a critical impact on the company's revenue and profit ends. The continuous optimization of the renewal rate can effectively increase the company's SaaS business revenue and reduce the company's overall selling expense rate.

The monetization efficiency on existing merchants is expected to increase

Improving monetization efficiency has always been one of the biggest problems for e-commerce SaaS service providers. Compared with traditional e-commerce platforms, the traditional e-commerce platform's centralized characteristic can continue to bring traffic to merchants, hence traditional e-commerce platforms can enjoy higher bargaining power in the current Internet age where "traffic is king" and also enjoy higher monetization effectiveness. On the contrary, private traffic e-commerce SaaS providers will not actively divert traffic for merchants. Therefore, e-commerce SaaS tool providers lack the ability to monetize traffic, which affects their monetization efficiency and bargaining power to a certain extent. Nevertheless, even without considering new merchants, we believe that the company's monetization efficiency is expected to be further enhanced (for existing merchants). The main reasons are:

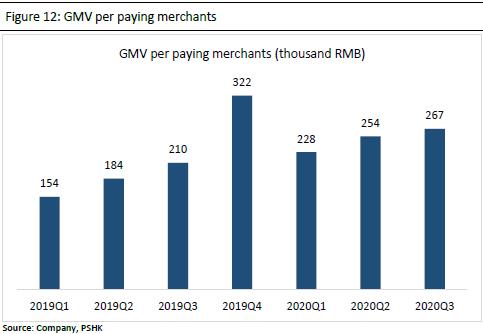

1) A tool itself cannot create value for the tool provider. Only when the user of the tool can continuously and effectively generate value by using the tool, can the tool create value. We believe that the average GMV of merchants is one of the more effective indicators to measure merchants` performance improvement. The average GMV per paying merchants (quarterly GMV generated by Youzan SaaS products/paying users as of the end of the quarter) has gradually increased in recent years, from RMB 154,000 in 2019Q1 to RMB 267,000 in 2020Q3. Ignoring the data deviation caused by the churn of low-tier merchants with low average GMV and the increase of top-tier merchants with high GMV, the average GMV of the company's paying merchants has grown hugely, with a CAGR of 44% during the period. As long as merchants realize that the company's SaaS products can effectively increase their GMV, the company will have higher bargaining power, and its SaaS products will have a certain room for price increase. We believe the company can increase its monetization efficiency on existing merchants by increasing the price of SaaS products in the future. Although the company has already announced to increase RMB 2000 in price for Youzan Weimall's professional and flagship version, nonetheless, in a mid-long term perspective, we believe the company's SaaS product still have certain room for price increase.

2) Even if the company's products do not increase in price in the future, the company can still enhance its monetization effectiveness on existing merchants by increasing the ARPU. The overall ARPU (total revenue / paying merchants) of 2019 and 2020Q3 were RMB 14,217/4,924, respectively. We believe that there is still sufficient room for improvement in ARPU in the future. The main reasons are ① As the company's extended services and payment service system further improved in the future, the penetration rate of extended services and payment services is expected to increase, driving the overall ARPU to increase. ② We believe that when a business has a certain degree of trust and recognition for the company's SaaS products, and when the business's scale has grown to a certain extent, they will upgrade to higher-level SaaS products, thereby increasing the company's overall ARPU.

As a whole, we believe that even without considering new paying merchants, the company still has the ability to enhance its monetization efficiency, laying a certain foundation for the company to start generating profit and to achieve SaaS scale effect.

Launched overseas product allvalue, allowing merchants to enter overseas` market

During the 8th Anniversary Ecological Conference of Youzan on November 27, 2020, Baiya announced that Youzan will launch allvalue, an overseas product, to meet the strong demand for cross-border e-commerce sales from Chinese merchants. The allvalue brand means "All you need to grow is what we value", and once again emphasizes the company's consistent idea to create value for the growth of merchants. Allvalue provides a variety of functions for merchants. The followings are descriptions to some of the functions.

1) Help merchants quickly build online stores, the entire shop opening process is simple to operate, and provides multi-industry and multi-category store templates for merchants to choose. The templates are all designed by international first-class designers to improve buyers` shopping and browsing experience.

2) Access the world's leading social platforms for product sales, including Facebook, Line, Instagram, etc., and provide mobile social communication channels to facilitate buyers to contact merchants and customer service for shopping consultation. Youzan also developed an application for merchants, which is convenient for merchants to effectively grasp store orders and other operating data.

3) Help merchants to carried out social marketing and operate private traffic management in overseas markets. It helps merchants to connect with overseas advertising platforms such as Google, Facebook, etc., and provide merchants with rich marketing tools. In addition, allvalue also provides a socialized customer management (SCRM) system, where merchants can interact with buyers, including the establishment of member discounts, points systems, etc., to stimulate repurchase rates and increase customer loyalty.

The company is expected to effectively assist merchants in entering overseas markets by relying on years of experience in providing online store opening and private traffic management services in China. At the same time, the company has established different operation teams in overseas regions to provide overseas localized services for Chinese merchants to increase the success rate of them going abroad. At present, the overseas e-commerce markets have great growth potential, with the high going-aboard demand from Chinese merchants, we believe that allvalue will become the company's future key growth driver.

�Financial Analysis and Forecast

Revenue

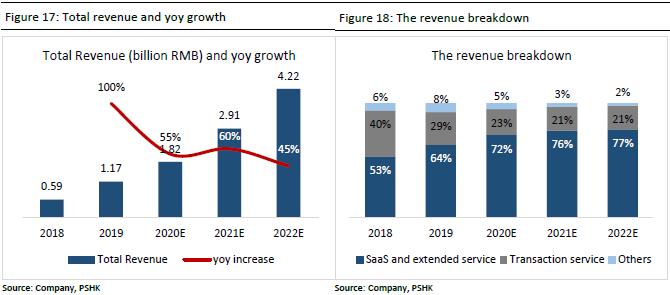

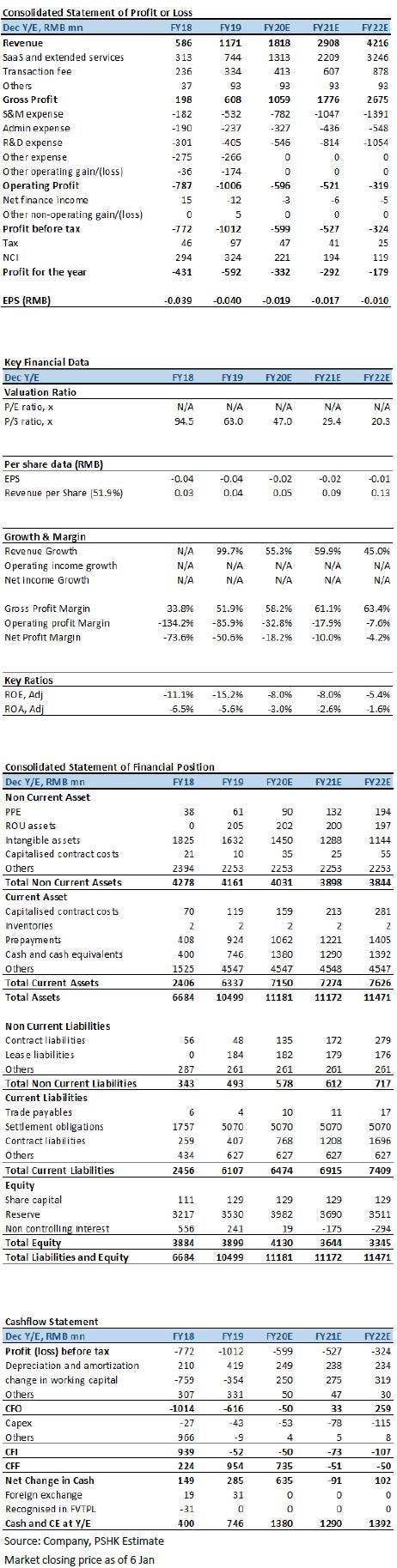

The company's revenue is composed of three business segments, SaaS and extended services, transaction services and other businesses. The company's total revenue rose from RMB 586 million in 2018 to RMB 1.171 billion in 2019, an increase of 99.7%. The company's SaaS and extended services/transaction services/other business revenues accounted for 53.4%/40.2%/6.3% and 63.6%/28.5%/7.9% of revenue in 2018 and 2019, respectively.

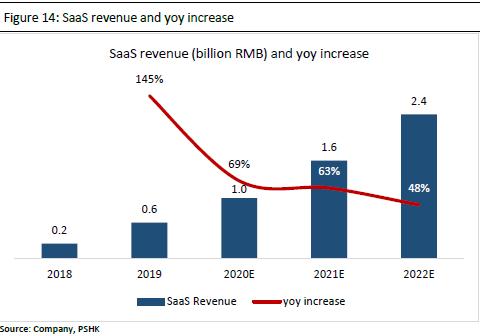

In terms of breakdown, the company's SaaS business revenue in 2018/2019 was RMB 242 million/RMB 593 million, an increase of 145%. This huge growth was mainly driven by the simultaneous growth of the number of paying merchants and the ARPU of merchant SaaS services. The number of paying merchants in 2019 was 82,300 (+39.6% yoy) and the ARPU of the SaaS business in 2019 was RMB 7,200 (+75% yoy). We believe that the number of paying merchants and the ARPU of the company's SaaS business still has huge potential for growth in the future. Considering 1) The renewal rate will gradually increase due to the continuous expansion of top and mid-tier merchants in the future. 2) The popularity of the private traffic management e-commerce model will further increase in the future. 3) The digital transformation trend of offline merchants will continue in the future. We expect the company's paying merchants to reach 169,000 in 2022 with 2019-2022 CAGR of 27.0%. On the other hand, we believe that the ARPU of the SaaS business can rise steadily in the future because 1) the continuous increase in proportion of top and mid-tier merchants will drive ARPU upward 2) the upgrade of higher level SaaS products by merchants as a result of increasing degree of trust on the company's SaaS products from merchants, will also drive ARPU upward 3) the future increase in price of SaaS products (including the recent rise of price in 2021) will also likely to increase the company's future SaaS ARPU. Based these assumptions, we predict that the SaaS business ARPU in 2022 will reach RMB 14,300, and the CAGR will be 26% in 2019-2022. In conclusion, we estimate that the company's SaaS business revenue in 2020/2021/2022 to be RMB 1.00/1.63/2.41 billion, representing a yoy increase of 69%/63%/48% respectively.

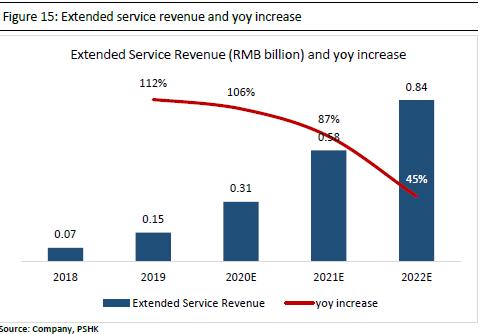

As for the company's extended services, it rose from RMB 70 million in 2018 to RMB 150 million in 2019, an increase of 112%. This increase is mainly due to the increase in merchant GMV (the charging method for extended services is generally linked with the GMV) and the increase in the penetration rate of company extended services. The overall GMV of the company's merchants in 2018/2019 was RMB 33.0 billion / RMB 64.5 billion, and it increased by 65.5% in 2019. On the other hand, the take rate of extended services (extended service revenue/GMV, this ratio can be used to measure the company's extended service penetration rate) in 2018/2019 were 0.21%/0.23% respectively. Looking ahead, we believe that the further popularization of private traffic e-commerce system in the future will drive the increase in total GMV of the company's merchants. It is estimated that GMV will reach RMB 195 billion in 2022, with CAGR in 2019-2022 at 44.6%. Meanwhile, we believe as the company's extended services system continue to further improve, the extended service penetration rate/take rate will gradually increase. We predict the take rate of extended services to be 0.43% in 2022. To sum up, we estimate that the company's extended service revenue for 2020/2021/2022 to be RMB 309/578/839 million, representing a yoy increase of 106%/57%/45% respectively.

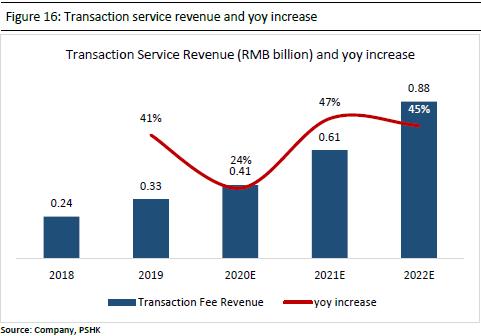

For the company's transaction services business, revenue rose from RMB 240 million in 2018 to RMB 330 million in 2019, an increase of 41%. This increase was mainly due to the increase in merchant GMV (transaction fee income is linked to GMV), but at the same time it was offset by the shrinking of the company's original payment business. The transaction service take rate (transaction fee income/GMV) also dropped from 0.715% in 2018 to 0.517% in 2019. We believe that the company will continue to shrink its original payment business in the future, and the company's future payment business will mainly serve SaaS merchants in order to complete and enhance the closed loop of the e-commerce transaction ecosystem. Therefore, we predict that the company's future transaction service take rate will continue to remain at low level, estimated to be about 0.4%-0.45%. Based on this assumption, we estimate that the company's transaction fee income for 2020/2021/2022 to be RMB 413/607/877 million, representing a yoy increase of 24%/47%/45% respectively.

Because the company's other revenue business segment is not one of the company's core business, it includes advertising business and some leftover businesses. Therefore, we do not make future revenue forecasts for the segment. The revenue remains the same for 2020/2021/2022. Overall, we predict that the company's total revenue for 2020/2021/2022 will be RMB 1.82/2.91/4.22 billion, representing a yoy increase of 55%/60%/45% respectively.

Gross Profit Margin

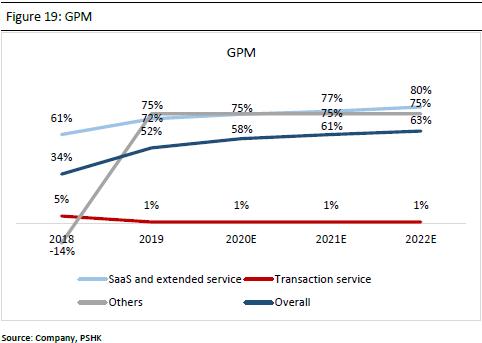

The company's gross profit margins in 2018/2019 were 33.8%/51.9%, an yoy increase of 18.1 ppts in 2019. This increase was mainly due to 1) the increase in the proportion of revenue from SaaS and extended services (higher gross profit margin). 2) At the same time, the gross profit margin of SaaS and extended services increased by approximately 10ppts due to the large increase in the number of merchants. In terms of segments, we believe that the company's GPM of SaaS and extended service business will continue to rise in the future, mainly due to 1) SaaS scale efficiency 2) the expected increase in extended service penetration rate. We forecast it to be 75%/77%/80% in 2020/2021/2022. As for the payment service business, since the company's payment platform is mainly positioned as the infrastructure of the SaaS business, the fees it collects from the merchants are basically the same as those charged by the third-party payment platforms (such as WeChat Pay and Alipay) that it connects to, hence we predict the GPM for this segment to be below 1% in the future. Overall, we forecast the company's gross profit margin for 2020/2021/2022 to be 58%/61%/63%.

Expense ratio

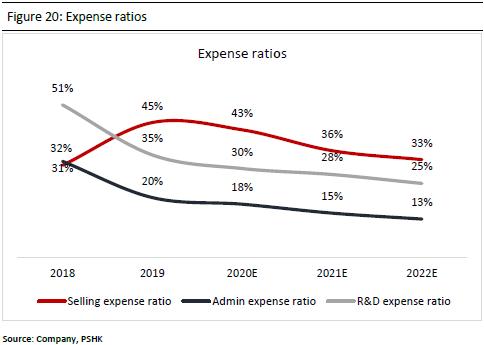

We believe that with the increase in the merchant renewal rate and the increase in the proportion of extended service revenue in the future, the company's selling expense ratio is expected to gradually decline. We forecast the selling expense ratio of the company in 2020/2021/2022 to be 43%/36%/33%. At the same time, the admin expense ratio and R&D expense ratio (included in other operating expenses and equity-settled share-based payments) are also expected to decline correspondingly with the high growth of income (scale effect). We forecast the company's admin expenses ratio for 2020/2021/2022 to be 18%/15%/13%, and the R&D expense ratios for 2020/2021/2022 to be 30%/28%/25%.

�Valuation

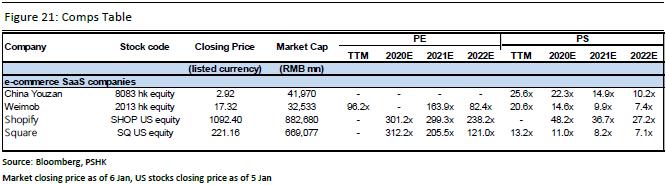

Since the company is still in the early stages of development and has not yet recorded a profit, we use the PS ratio to value the company. We believe that the core businesses of the US-listed Shopify (SHOP.US) is similar to the company, both of which provide merchants with shop opening services, value-added services and payment services. As of January 6, 2021, Shopify's 2022 forecast market-sales ratio is 27.2x, but considering that Shopify's business development is relatively mature and future growth stability is relatively high, we will give the company a certain amount of valuation discount to Youzan. We are giving the company a 2022 target PS of 25x. Taking into account that the company's listed entity currently holds 51.9% of the shares of Qima Technology (Youzan's operating body), we give the company a 10% control premium, and the 24-month target price is HKD3.96, with respective 2020/2021/2022 PS at 63.7x/39.8x/27.5x. We initiate with a Buy rating. (Market closing price as of 6 Jan) (exchange rate: RMB 0.88/HKD)

Risk

1) The company is listed on HKEX GEM board, which may have higher risk and volatility comparing to stocks on HKEX main board 2) The expansion of SaaS customers is worse than expected 3) The increased industry competition 4) GMV increase less than expected 5) Merchants renewal rate less than expected

�Financial Statements

Click Here for PDF format...