Investment Summary

Private traffic management is the main trend for offline merchants

Take Tencent as an example. Tencent itself focuses more on WeChat payment and advertisement business, while its e-commerce SaaS services mainly choose to cooperate with third-party SaaS platforms. Therefore, the rapid development of social e-commerce platforms has provided huge business opportunities for third-party SaaS platforms. The third-party e-commerce SaaS platforms help offline merchants to build their online stores on social platforms (such as WeChat) and provides services such as online commodity transactions, order management, online payment, and user management. We believe that for merchants who already have enough user traffic for repurchase, it is more appropriate to open an online store through a third-party SaaS platform for private traffic management. Effective private traffic management can increase customer repurchase rates and reduce Customer acquisition cost.

The company actively expands the scale of its SaaS direct sales team, and the proportion of SaaS direct sales revenue is expected to further increase in the future

We believe that for a SaaS service provider, it is especially important to have a strong sales channel. The sales channel connects the company's products with its customers, and a professional sales team can clearly understand customer needs, so as to ensure that the company's products can meet customer needs. Currently, the company mainly sells through two major channels, 1) its own direct sales team and 2) channel partners. According to the management of the company, the company currently has approximately 1,600 direct sales personnel. In recent year, the revenue proportion of the company's SaaS direct sales has increased, from 29% in 2016 to roughly 40% in 2019. It is expected that the direct sales revenue for the whole year of 2020 will reach 50%. We believe that the company's future increase in the proportion of direct sales revenue can reduce the channel partner share expense ratio of the SaaS business (reflected in the sales and sharing expenses), thereby increasing the profit margin of the SaaS business.

The companys advertising cooperation with Bytedance is expected to become another growth point in the future

In recent years, Bytedance's advertising business has grown rapidly. According to Juheng.com, the scale of Bytedance's advertising has risen from RMB 6 billion in 2016 to RMB 155 billion in 2020 (according to industry sources). At present, the company has cooperated with Bytedance to place advertisements on Bytedance's platforms (such as TikTok, Toutiao News, etc.) for its advertisers. Since the users of the Bytedance platform are known for their youth. Hence, for some businesses (such as industries that with mainly young customers), placing advertisements on the Bytedance platform can enjoy a higher advertising conversion rate. According to the management, about 80% of the company's targeted marketing business's gross billing comes from Tencent, and 20% comes from ByteDance. The proportion of gross billing contributed by ByteDance is still at a low level and we believe it can be greatly increased in the future. We believe that Bytedance will become a major driving force of growth for the company's targeted marketing business in the future, and we look forward to tighter cooperation between the two parties in the future.

Valuation

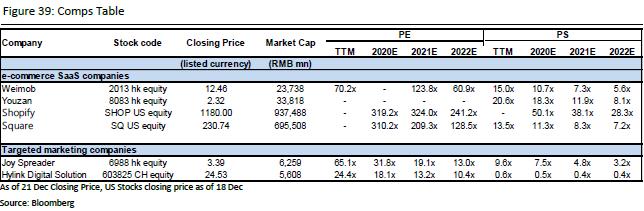

We have adopted SOTP to value the company. Considered its peer valuation multiples, we are giving target 2021 PS of 20x to the company's SaaS business, and a target 2021 PE of 18x to the company's targeted marketing business. We set the target stock price at HKD 15.04, with respective 2020/2021/2022 adjusted PE at 198x/127x/82x. We initiate with a Buy rating. (Market closing price as of 22 Dec) (exchange rate: RMB 0.88/HKD)

Industry Review and Forecast

China's e-commerce industry

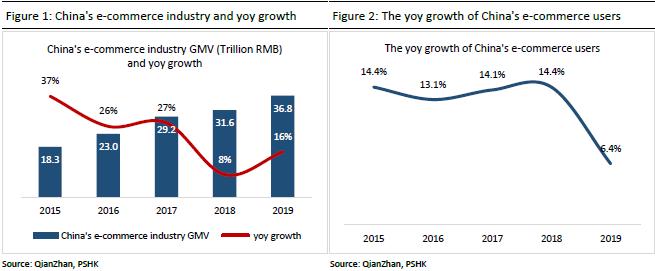

China's e-commerce industry is now mature and its growth is slower than before. The growth of traditional e-commerce users, led by Tmall, JD.com, and Vipshop, has significantly slowed down, which means that competition in the industry has become increasingly fierce and customer acquisition costs have become higher. According to data from the Qianzhan Industry Research Institute, China's e-commerce GMV and users increased by 13.1% and 6.4% yoy in 2019, respectively, and these growth rates were significantly slower than the 36.6% and 14.4% in 2015. The noticeable slowdown in user growth coupled with the gradual increase of merchants on traditional e-commerce platforms has led to intensified competition among merchants to a certain extent. The cost of user traffic for traditional e-commerce platform has risen sharply, putting a certain amount of pressure on small and medium-sized merchants and long-tail merchants.

China's social e-commerce industry

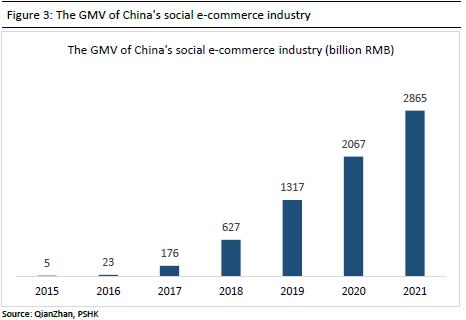

In today's mobile Internet era, social platforms Apps represented by WeChat have huge user traffic and occupy most of the user's online time. Take WeChat as an example. As of 2019, WeChat has 1.165 billion monthly active users, and the huge user traffic of WeChat has greatly reduced the cost of customer acquisition for its social e-commerce. On the other hand, other functions in the WeChat ecosystem such as WeChat Payment etc. also provide good technical support for its social e-commerce platform. At present, WeChat has created its unique social e-commerce ecosystem through decentralized innovation and breaking the traditional e-commerce model, allowing small and medium-sized enterprises to quickly expand their business and user base, while directly controlling and managing their customer data and customer relationships. According to the Zhiyan Consulting Report, the GMV of China's social e-commerce industry has increased from RMB 4.69 billion in 2015 to RMB 1.32 trillion in 2019, and is expected to reach RMB 2.86 trillion in 2021.

The differences between social and traditional e-commerce

We believe that e-commerce shopping can be divided into two major stages, the demand stage and the purchase stage. In the demand stage, traditional e-commerce is dominated by search shopping, so user consumption is typically planned consumption. On the contrary, part of social e-commerce shopping are unplanned consumptions, such as product sharing in Wechat's Moments to stimulate users` desire to consume. In the shopping phase, the consumption conversion rate of traditional e-commerce is lower than that of social e-commerce. The main reason is that the trust mechanism of social e-commerce (recommendation by friends) is more credible than traditional e-commerce user reviews, so that consumption can be quickly promoted on social e-commerce platforms.

In addition, in the case of abundant supply of goods, the ranking of items will have an extremely important impact on traditional e-commerce consumers. Consumers generally choose items with higher rankings, so the centralized characteristics of traditional e-commerce (traffic flow in from one entrance, the platform) makes the user traffic continuously converge to the high ranking items. In this case, product marketing and advertisements become especially important. On the other hand, social e-commerce (decentralized), doesn`t has the characteristic of user traffic asymmetric, because in the case of friend recommendation, consumers` trust in friends will reduce their dependence on ranking and brand, causing products more likely to get their user traffic equivalent to its price-performance ratio. Therefore, we believe that social e-commerce is more friendly to long-tail products and small and medium-sized businesses, while traditional e-commerce is more focused on top products. We believe that the application scenarios of the two e-commerce models in the future will be different.

Private traffic management is the main trend for offline merchants

Take Tencent as an example. Tencent itself focuses more on WeChat payment and advertisement business, while its e-commerce SaaS services mainly choose to cooperate with third-party SaaS platforms. Therefore, the rapid development of social e-commerce platforms has provided huge business opportunities for third-party SaaS platforms. The third-party e-commerce SaaS platforms help offline merchants to build their online stores on social platforms (such as WeChat) and provides services such as online products transactions, order management, online payment, and user management. For offline merchants, compared to opening a store on traditional e-commerce, the third-party SaaS platform provides store opening services with two major advantages.

1) The private traffic management of social e-commerce is more effective. Through third-party SaaS platform to open a store in the social e-commerce (such as opening a store on WeChat), the offline merchant can directly manage and interact with their consumers. On the other hand, if a merchant opens a store in a traditional e-commerce platform, it cannot directly manage its consumers. Since the traditional e-commerce platforms control the user traffic, hence the buyers can only reach the merchants` good through the search engine. Therefore, it is more effective for businesses to manage private traffic in social e-commerce platforms.

2) Since third-party SaaS platforms do not need to provide merchants with strong user traffic like the traditional e-commerce platforms do, the fees charged by third-party SaaS platforms for opening stores and selling products on social e-commerce platforms will also be less than the traditional e-commerce platform. Take Tmall as an example. Tmall merchants need to pay an annual fee of RMB 30,000-60,000 and a sales commission of 2%-5%, while Weimob (the leading third-party SaaS platform in the industry) only charges a minimum of RMB 6,800 annual SaaS service fee.

Based on the above reasons, we believe that for merchants who already have enough user traffic for repurchase, it is more appropriate to open an online store through a third-party SaaS platform for private traffic management. Effective private traffic management can increase customer repurchase rates and reduce Customer acquisition cost. At the same time, since the growth of traditional e-commerce users has obviously reached a bottleneck and the cost of public traffic is high, it is especially important for small and medium-sized businesses to have their own fixed customers and to manage them efficiently under private traffic management.

The top tier third party SaaS providers are likely to be the beneficial from the launch of ¡§Wechat small stores¡¨

In June 2020, Tencent launched ¡§small WeChat store¡¨, a small program designed to help small businesses open online stores for free. But since it only offers basic SaaS services for free, hence its main customers are the relatively small SMEs. On the contrary, the main customers of leading third-party SaaS providers in the industry (such as Weimob and Youzan) are the relatively large SMEs. The free function ¡§small WeChat stores¡¨ offers are incompatible with the needs of the large SMEs. We believe the ¡§small Wechat stores¡¨ will gradually eliminate the low tier third-party SaaS providers, making the industry gradually concentrated, which is beneficial to the industry's leading third-party SaaS providers. In addition, the free SaaS services provided by ¡§WeChat small stores¡¨ can encourage small SMEs to adapt to the current digital trend and grow rapidly from it. When these small SMEs take shapes, the free SaaS services no longer fulfill their requirements, they are expected to become potential new customers of the top tier third-party SaaS providers in the industry.

China's mobile targeted marketing market

Compared with traditional Internet advertising, the advertising advantage of targeted marketing lies in its ability to analyze potential customers through big data. Therefore, advertising is more targeted, greatly reducing advertising costs and improving advertising efficiency. Mobile targeted marketing experienced significant growth recently, as a result of the rapid rise in penetration of mobile social media services, the explosion in digital content, and increasing time spent online by mobile users. According to Frost and Sullivan, the market size of China's mobile targeted marketing market will reach RMB 601 billion in 2022, with 2017-2022 CAGR at 31.7%.

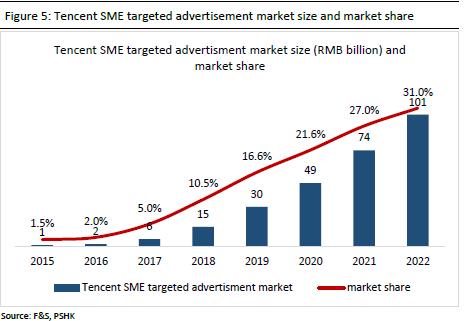

Tencent's advertising is based on WeChat (including Wechat's Moments advertising), and integrates other product advertising resources such as QQ Music, Tencent Video, and Tencent News. According to Frost & Sullivan, Tencent will become the mainstream SME targeted marketing channel. Its market shares in the SME targeted marketing market is expected to reach 31% in 2022, which is a huge increase compared to the 1.5% in 2015.

Company Overview and its Competitive Advantages

Weimob is a leading provider of SaaS services and targeted marketing services based on Tencent ecosystem for SMEs in China

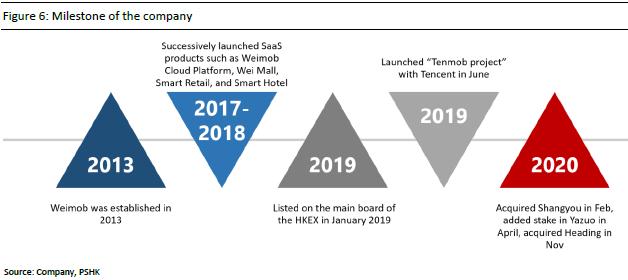

Weimob was established in April 2013 and currently provides e-commerce SaaS and targeted marketing services for Chinese SMEs. Weimob launched its first SaaS product shortly after it was founded, and became one of the first partners of the WeChat official accounts. Since then, Weimob has become the main partner of WeChat e-commerce SaaS and advertising services, and it is closely tied to the development of WeChat advertising and e-commerce ecology. From 2017 to 2018, Weimob successively launched SaaS products such as Weimob Cloud Platform, Wei Mall, Smart Retail, and Smart Hotel. In June 2019, the company and Tencent Advertisement launched the "Tenmob Project", combining the user traffic of Tencent's advertising platform and Weimob e-commerce SaaS service capabilities, to create a more complete e-commerce ecosystem. In addition, the company have invested/acquired Shangyou, Yazuo and Heading respectively during 2019-2020 to accelerate its business expansion to offline retail and catering SaaS business. The company was listed on the main board of the Hong Kong Stock Exchange in January 2019 and was included in the Southbound Stock Connect in September 2019. According to the Frost & Sullivan Report, the company is currently a leading provider of SaaS services for SMEs in China, and has become a leading targeted marketing provider in China serving SMEs on Tencent's social network service platform.

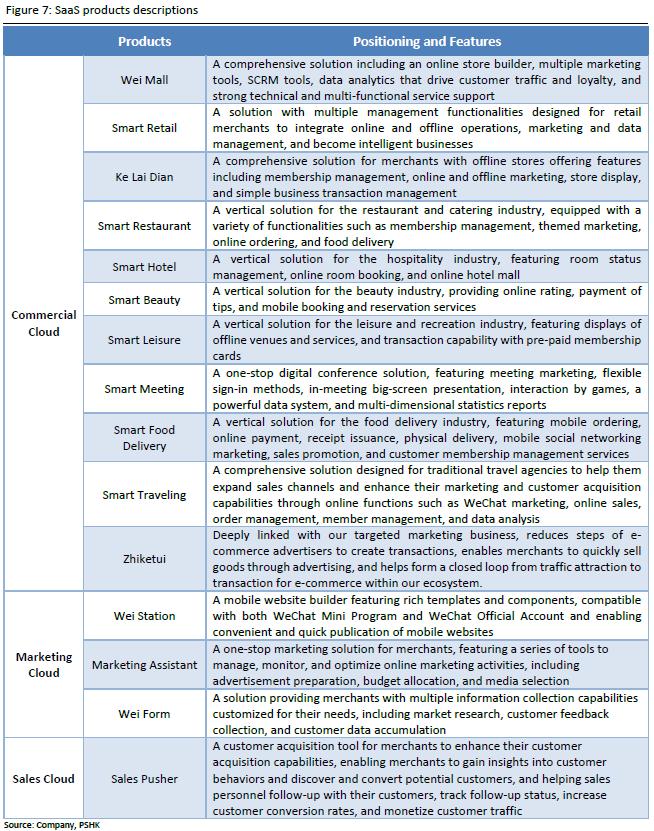

Weimob's SaaS products can be divided into three business segments: Commercial Cloud, Marketing Cloud and Sales Cloud

Weimob provides merchants with SaaS services based on the WeChat ecosystem through three SaaS products, Commerce Cloud, Marketing Cloud, and Sales Cloud. Among the three SaaS service products, commerce cloud's revenue accounted for the vast majority of the company's total SaaS revenue. In 2019, commerce cloud's revenue accounted for approximately 79% of total SaaS service revenue, while marketing cloud revenue accounted for approximately 21%. Weimob's commerce cloud mainly includes commercial SaaS products such as Wei Mal, Smart Retail, Smart Restaurant, Smart Hotel, and mainly serves merchants in the e-commerce, retail, hotel, and catering industries. The marketing cloud products mainly include Wei Station, marketing assistants, etc. The following is the descriptions of each product.

WeiMall

Weimall is an integrated e-commerce solution designed for SMBs centered on the WeChat ecosystem. It offers an integrated social media storefront builder, including storefront design, product display, order management, logistics management, data management, and support for both WeChat Mini Program and WeChat Official Account. Further, it offers various marketing and promotional plug-ins for merchants to attract, and interact with followers on WeChat, enhance word-of-mouth promotion, gamify the online shopping experience, and increase rate of repurchase. The major marketing plug-ins include 1) Group Buying («÷¹Î), 2) Bargaining (¬å»ù), and 3) Flash Discount (®É§é¦©). 1) Group Buying («÷¹Î) offers customers products and services at largely reduced prices on the condition that a minimum number of customers would make the purchase, which incentivizes customers to promote the products within their social networks to enjoy the reduced price. 2) Bargaining (¬å»ù) enables a customer to reduce the original price of the product or service by inviting friends to help cut the price, and the more users involved, the more discount the customer gets. Friends who help with bargaining for the purchaser receive coupons or cash as incentives. This allows the merchants to reach for a wider customer groups. 3) Flash Discount (®É§é¦©) provides customers with steep, limited-time discounts and other benefits, including membership points or coupons, to stimulate sales while promoting the merchant's brand image. Lastly, Wei Mall also provide services such as Social Customer Resource Management (SCRM), Data-driven Analytics and Reporting and etc.

Smart Series SaaS Products

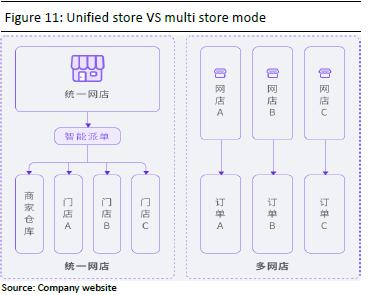

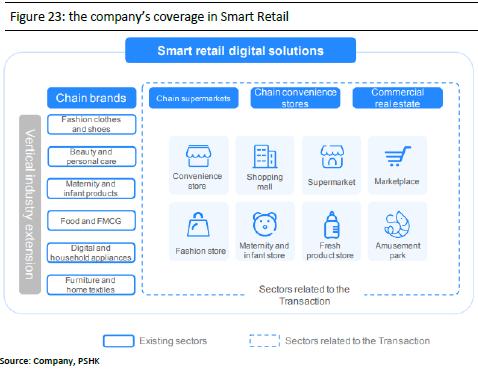

Smart Series SaaS Products, including Smart Retail, Smart Restaurant, Smart Hotel etc, are solution with multiple management functionalities designed for merchants to help them integrate online and offline operations, marketing and data management, through the Wechat Official Accounts and mini program, and become intelligent businesses. Take Smart Retail as example, it provides a series of services, including 1) Online Store Management, 2) Invoice Management, 3) Shopping Guide System, 4) Online Appointment and 5) SCRM. 1) Merchants can create online stores and manage basic store information, decoration, logistics, and products. The online store management supports two modes: unified store mode and multi-store mode. For unified store mode, the system will allocate the order to the most appropriate offline store for mailing through its AI system, based on the mailing address and the inventories record of each offline stores. 2) It provides an independent invoice management system for a merchant's headquarters and for each store. Through the provision of complete inventory management such as stock in, stock out, transfer, and inventory control for merchants, online and offline integrated product management is realized. 3) It provides a complete shopping guide system to help merchants provide one-on-one service to customers. The shopping guide can provide customers with coupons, order recommendations, and other exclusive customer services based on the comprehensive user profile provided by the system. 4) Customers can easily make an appointment online and choose the store and service time, this allow higher efficiency at peak time. 5) The SCRM tool provides merchants with a powerful and complete system that collects online and offline customer resources, and digitalizes and integrates management of members to help brands maximize the value of customer resources. As of 2019 year-end, the company has 1,101 Smart Retail merchants.

Zhiketui (ª½«È±À)

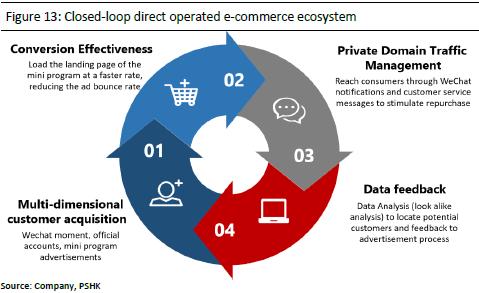

On June 12, 2019, while announcing the launch of the "Tenmob Project" with Tencent Advertisement, the company officially released the product zhiketui (ª½«È±À) solution, directly tackling the e-commerce marketing demand at the direct operated e-commerce 2.0 era. By consolidating the quality resources of both Weimob and Tencent, it creates a closed-loop e-commerce ecosystem to assist the marketing transformation and upgrade of the Chinese SMEs. Zhiketui, help merchants to build advertisement landing pages on Wechat mini program. As compared with the traditional advertising landing page, the landing page created by Weimob Zhiketui uses the light codes of Wechat mini-program and page static caching technology, so consumers can load the mini program landing page at a faster speed, greatly reducing the bounce rate of the advertisement while loading. After the customer completes the transaction, Zhiketui can assist merchants to reach consumers through WeChat customer messages, service notifications, etc., and maintain them for a long time to promote consumer repurchase and retention. It greatly improves the monetization ability of the private traffic management. In addition, Zhiketui provides comprehensive user data analysis, accurately locates potential target customers for merchants. The data can be recycled back to the advertisements process, hence, creating an ecological closed loop targeting the 2.0 era of direct operated e-commerce.

The company is migrating toward the high-end market

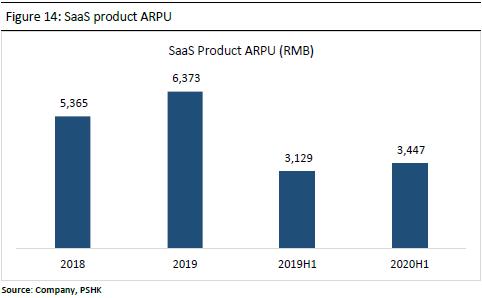

Regarding the company's SaaS business, the company has been actively expanding to high-end customers since 2019. Although the cost of acquiring a high-end customer is relatively high, but high-end clients tend to have longer life cycles and are more willing to pay. Besides that, the renewal rate of high end clients is also higher. Hence, we believe that the company's SaaS revenue will become more stable after implemented the high-end strategy. Further, as mentioned in the above industry analysis, the company's high-end strategy not only completely avoided the negative impacts of Tencent's launch of the ¡§WeChat small store¡¨, but also is expected to be benefited from it. The company's SaaS product ARPU in 2020H1 was RMB 3,447, which is a significant increase compared to RMB 3,129 in 2019H1. It can be seen that the company's strategy of moving toward the high-end markets by serving the high-end clients is gradually implemented and is very effective.

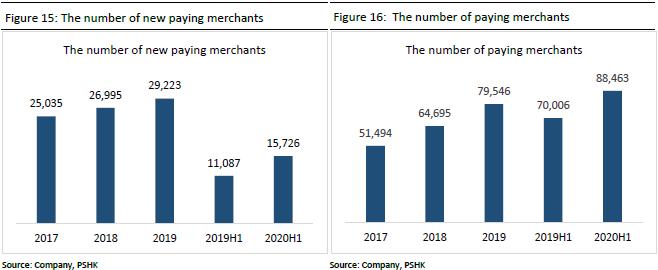

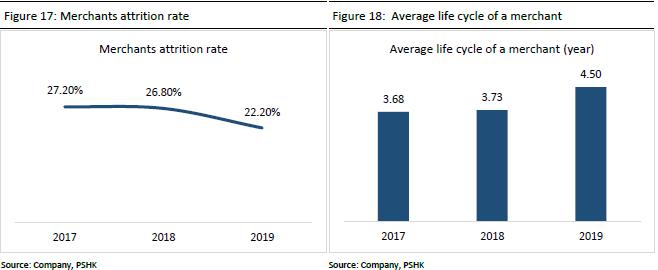

SaaS business paying merchants gradually increased, and merchant attrition rate decreased yoy

In addition to ARPU, 1) the number of new paying merchants 2) the number of paying merchants 3) the merchant attrition rate are also important operating indicators of the company's SaaS business. 1) The number of new paying merchants of the company rose from 25,035 in 2017 to 29,223 in 2019, with a CAGR of 8.0% during the period. 2) The number of paying merchants increased from 51,494 in 2017 to 88,463 in 2019, with a CAGR of 31% during the period. 3) The merchant attrition rate has been significantly improved in recent years, from 27.2% in 2017 to 22.2% in 2019. The average merchant life cycle (ie 1/merchant attrition rate) has risen from 3.7 years in 2017 to 4.5 years. The gradual increase in merchants` dependency on the company SaaS products has enabled its SaaS performance to grow steadily.

Weimob is a leading third-party service provider based on WeChat for SMEs

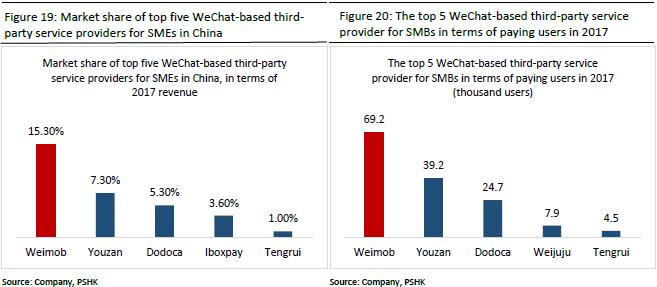

In recent years, the user base of WeChat has increased rapidly. As of 2019, the monthly active users of WeChat were 1.165 billion. As the user base of WeChat increases, the activeness of its ecosystem also increases. Because WeChat focuses more on its main business, such as advertising and payment services, this has created the rise of many WeChat-based third-party service providers to meet the needs of Chinese SMEs for user traffic in the WeChat ecosystem. According to F&S, the company held the leading position as measured by revenue in 2017, among the cloud-based commerce and marketing service providers for SMEs in China. We believe that as more and more offline industries and merchants expand their businesses through the WeChat ecosystem, the WeChat-based third-party service market for SMEs in China will maintain high growth in the future, and Weimob, as WeChat's main partner in this market, will become the main beneficiary.

Actively expand offline SaaS business through investment acquisition and cooperation with Tencent

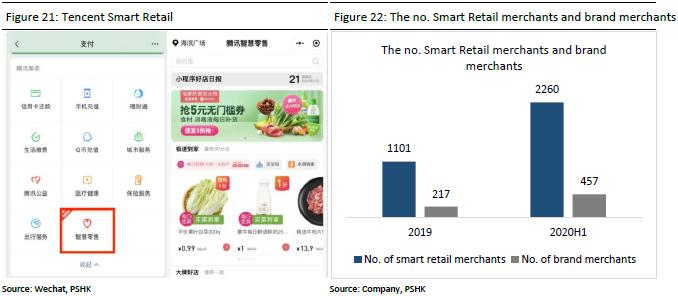

During the epidemic (February 2020), WeChat launched a "smart retail" mini program in Shenzhen, vigorously entering the offline retail industry. At present, WeChat Smart Retail are serving major retailers such as Daily Youxian, Yonghui, Uniqlo, and Walmart. As a partner of WeChat's third-party services for many years, Weimob has continued to maintain good cooperation with Tencent Smart Retail in customer acquisition, product research and development, and operational services. The operating indicators of the company's Smart Retail has increased significantly. As of the end of June 2020, the number of the company's smart retail merchants reached 2,260 (+105% hoh). Among the 2,260 smart retail merchants, brand merchants reached 457 (+106% hoh) and the ARPU of brand merchants reached RMB 227,000 (+82% hoh).

On the other hand, the company is expanding offline retail, catering, and other sectors` SaaS business extensively through investments and acquisitions, ie Shangyou, Yazuo and the recently acquired Heading Information. The below is the case study of the Heading Information and Yazuo acquisitions.

1) Acquisition of Heading Information ¡V expanding another retail format: Heading Information is principally engaged in providing information and digital upgrading solutions for retail enterprises. Currently, it mainly provides information solutions in chain retail, commercial real estate, and warehousing and logistics for multi-format merchants and enterprises including convenience stores, specialized stores, supermarkets, department stores and shopping malls, and also explores innovative businesses related to payment and smart hardware. Further, According to the China's Top 100 Convenience Stores in 2019 issued by China Chain Store & Franchise Association (¡§CCFA¡¨), Heading Information's customers cover more than 30% of companies on such list. According to Top 100 in Terms of Commercial Real Estate in 2019 published by Guandian Index Academy (Æ[ÂI«ü¼Æ¬ã¨s°|), over 40% of the enterprises select Heading Information, while Top 50 companies cover 58% of commercial real estate customers. Upon completion of the Transaction, the company has increased its coverage of multiple retail formats such as commercial real estate, chain supermarkets and chain convenience stores. In 2019, the ARPU of Heading is RMB 540 thousand, which is higher than the company's Smart Retail brand merchants` ARPU of RMB 220 thousand. Hence, acquiring Heading is in line with the company's strategy of high-end market migration. In addition, through the Transaction, the company further improves its ability to serve medium and large chain retail customers. After covering retail business forms including commercial real estate and chain supermarkets, the Group has the opportunity to further expand resources of brand owner customers who have cooperation with shopping malls and large supermarkets, thus forming ecological management from comprehensive commercial entities and shopping malls to brand stores (Plaza to Business) and from brand stores to customers (Business to Customer). Lastly, the company is expanded to further improve its middle- and back-end capabilities including purchasing, sales and inventory management, order management, warehousing management etc.

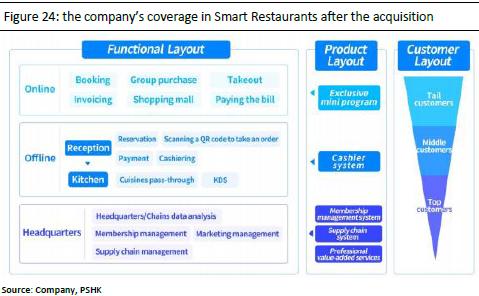

2) Yazuo Acquisition - from online to offline: On 19th of February, the company has announced to acquire 63.83% stake of Yazuo for RMB 114 million. Yazuo is principally engaged in (i) provision of middle-end membership management software and consultative professional services supporting member operation to KA chain catering enterprises; (ii) provision of front-end cashier software and hardware systems such as smart cashiers, smart ordering devices and smart QR code-scanning machines to catering outlets; and (iii) provision of back-end supply chain management solutions to catering enterprises. Prior to the acquisition, the company's advantage at catering SaaS providing sector was mainly online. After the acquisition of Yazuo, the company can effectively cut in from online to offline, improving its Smart Restaurant product chain by providing services from membership, cashier, takeaway, ordering, reservation, and supply chain management. The acquisition makes up for the company's shortcomings in serving medium and large catering customers. The ARPU of Yazuo in 2019 was RMB 18.4 thousand, higher than the ARPU of the company's 20H1 Smart Restaurant of TMB 16 thousand, once again, the acquisition is in line with the company's strategy of high-end market migration.

The company actively expands the scale of its SaaS direct sales team, and the proportion of SaaS direct sales revenue is expected to further increase in the future

We believe that for a SaaS service provider, it is especially important to have a strong sales channel. The sales channel connects the company's products with its customers, and a professional sales team can clearly understand customer needs, so as to ensure that the company's products can meet customer needs. Currently, the company mainly sells through two major channels, 1) its own direct sales team and 2) channel partners. When the company was founded, its sales were mainly relying on the channel partners. In recent years, the company has actively expanded the size of its direct sales team. According to the management of the company, the company currently has approximately 1,600 direct sales personnel. In recent year, the revenue proportion of the company's SaaS direct sales has increased, from 29% in 2016 to roughly 40% in 2019. It is expected that the direct sales revenue for the whole year of 2020 will reach 50%.

We believe that the company's SaaS direct sales revenue share still has room for improvement in the future. The main reasons are 1) The company's current direct sales personnel mainly operate in tier 1-2 cities in China. Since SaaS services are not yet popular in tier 3-4 cities, merchants in tier 3-4 cities do not have enough awareness of SaaS services, so the company's sales in tier 3-4 cities mainly rely on its channel partner. As the popularity of SaaS services in tier 3-4 cities gradually increases, we believe that the company's direct sellers will be able to operate in tier 3-4 cities. 2) According to the company's management, the company's new SaaS product are mainly allocated to its direct sales team for sales. As more and more new products are launched, the proportion of direct sales revenue will increase. We believe that the company's future increase in the proportion of direct sales revenue can reduce the channel partner share expense ratio of the SaaS business (reflected in the sales and sharing expenses), thereby increasing the profit margin of the SaaS business.

Targeted marketing services based on Wechat's ecosystem

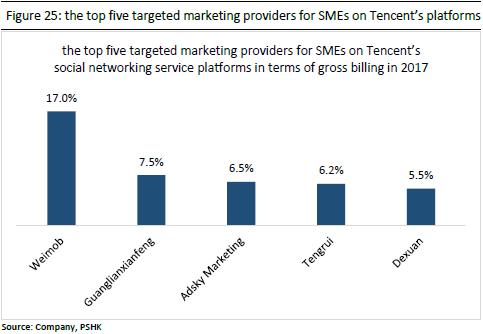

The company mainly provides targeted marketing to advertisers through Tencent social media platforms such as WeChat Moments, WeChat Official Accounts, Tencent News and Tencent Advertising. Tencent has more than 1.1 billion monthly active users and a huge amount of user traffic. Therefore, for advertisers, Tencent's diversified advertising channels have great advertising value. Weimob is the one of the most important third-party service provider and partner of Tencent advertising. According to Frost & Sullivan, based on 2017 gross revenue, the company is the largest targeted marketing provider for SMEs on Tencent's social network service platform. The market share is 17%. On 18th Aug 2020, the company was awarded the official gold service providers of KA (key accounts) by Tencent's advertising, fully demonstrate the recognition of Tencent on the company's advertising and marketing capabilities.

In addition, the company has built a proprietary data management platform (DMP) that contains rich consumer behavior and transaction data. DMP can help advertisers in targeted marketing to more accurately identify audiences who may be interested in the brand or become paying customers. The company's DMP analyzes the browsing behavior and transaction records of consumer groups for merchants, and marks the interest tags of these consumer groups for merchants to optimize audience positioning strategies. The company provides merchants with audience analysis such as payment ability, interests, age, gender and behavior, so that advertisers can accurately locate their potential customers and conduct marketing. The company has accumulated many years of targeted marketing and operation experience in multiple vertical sectors such as wedding clothing, education, interior decoration, catering, real estate and lifestyle services. Its intensive experience and data accumulated in these vertical sectors have become the company's strong competitive advantage.

The two major businesses of the company are synergized in many aspects

We believe that the two major businesses of the company have many aspects of synergy.

1) The company has integrated the SaaS business with the targeted marketing business. For example, merchants using the Wei mall can easily purchase the company's targeted marketing services through the control panel of the Wei mall, and place their advertisements on social media such as WeChat official accounts and Moments. This can greatly reduce the customer acquisition cost of the company's targeted marketing segment and hence and increase the company's overall profit margins. According to the management, the customer overlap rate of the company's targeted marketing business and SaaS business is roughly 40% currently. With the increasing demand for targeted marketing from merchants in the future, we believe this overlap rate is expected to increase further.

2) In the designated retail vertical sector, compared with ordinary advertising agencies, since the company has many years of experience in providing SaaS services, hence it has the advantage of having a clearer understanding of the business model of the merchants. Therefore, it can provide more accurate and effective marketing service plans for the merchants.

3) As mentioned above, the company is actively expanding its offline SaaS business in recent years (ie by acquisition and intensive investments). We believe that the company will continue to actively expand its offline SaaS business in the future, including expanding into new vertical retail format/sector. If these newly acquired merchants have demand for targeted marketing services, they will naturally become new customers of the company's targeted marketing business.

In summary, we believe that the multi-faceted synergies of the company's two major businesses are important competitive advantages for the company.

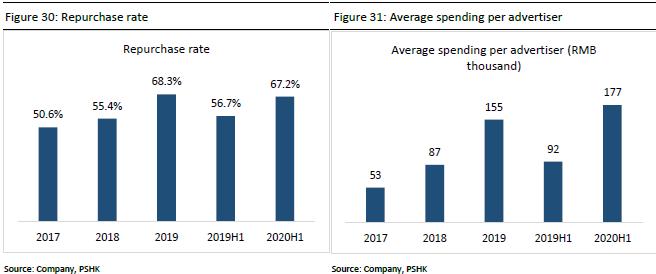

The operating indicators of targeted marketing have been improving in recent years

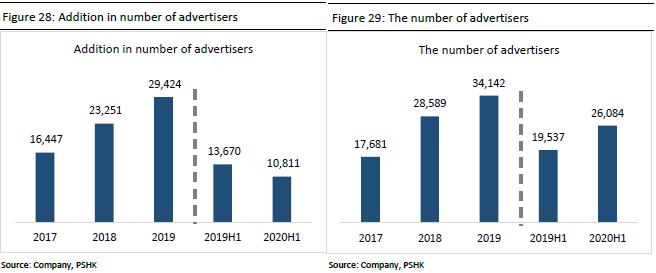

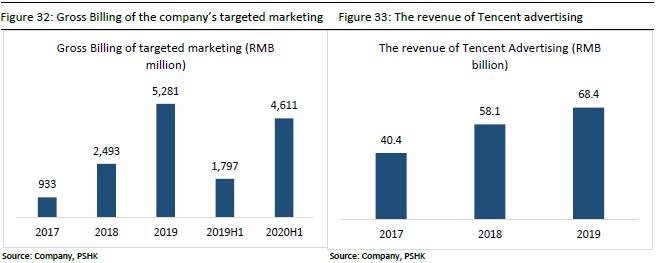

The company's targeted marketing business indicators are mainly 1) addition in number of advertisers 2) the number of advertisers 3) Repurchase rate 4) Gross billing and 5) Average spend per advertiser. The addition in the number of advertisers in the targeted marketing business rose from 16,447 in 2017 to 29,424 in 2019, with a CAGR of 33.8% during the period. 2) The number of advertisers rose from 17,681 in 2017 to 34,142 in 2019, with a CAGR of 39.0% during the period. 3) The repurchase rate, that is, the number of advertisers who have repurchased the services within the year as a proportion of the total number of advertisers, rose from 50.6% in 2017 to 68.3% in 2019, fully demonstrated the increasing customer satisfaction in recent years. 4) Gross revenue (that is, the total monetary value collected by targeted marketing from advertisers) increased from RMB 933 million in 2017 to RMB 5.281 billion in 2019. The CAGR during the period was as high as 138%. This growth is much higher than the 30% CAGR of Tencent advertising revenue over the same period, which means that the company's advertising share in Tencent advertising is also increasing rapidly. According to management estimates, the company's 2020H1 share in the Tencent advertising is approximately 11.5%. 5) The average spending per advertiser increased from RMB 53,000 in 2017 to RMB 155,000 in 2019. The CAGR during the period was 71%, mainly due to the company's transformation to serve Tencent KA (Key Accounts) customers.

The company's advertising cooperation with Bytedance is expected to become another growth driven in the future

In recent years, Bytedance's advertising business has grown rapidly. According to Juheng.com, the scale of Bytedance's advertising has risen from RMB 6 billion in 2016 to RMB 155 billion in 2020 (according to industry sources). At present, the company has cooperated with Bytedance to place advertisements on Bytedance's platforms (such as TikTok, Toutiao News, etc.) for its advertisers. Since the users of the Bytedance platform are known for their youth. Hence, for some businesses (such as industries that with mainly young customers), placing advertisements on the Bytedance platform can enjoy a higher advertising conversion rate. According to the management, about 80% of the company's targeted marketing business's gross billing comes from Tencent, and 20% comes from ByteDance. The proportion of gross billing contributed by ByteDance is still at a low level and we believe it can be greatly increased in the future. We believe that Bytedance will become a major driving force of growth for the company's targeted marketing business in the future, and we look forward to tighter cooperation between the two parties in the future.

Financial Analysis and Forecast

The revenue of SaaS business

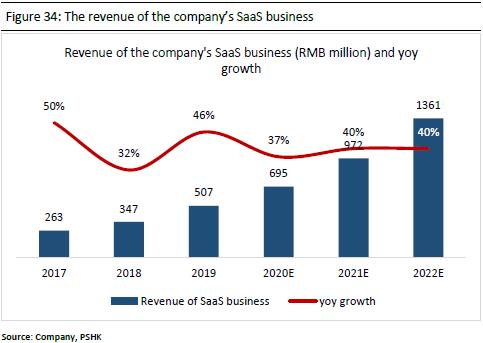

In recent years, the company's revenue from SaaS business has grown rapidly, from RMB 263 million in 2017 to RMB 507 million in 2019, with a CAGR of 38.8% during the period. This increase was mainly due to 1) the increase of SaaS paying customers and 2) ARPU increase during the period. 1) Thanks to the reduction in the attrition rate of paying customers and the expansion of offline SaaS merchants, the company's SaaS paying customers increased from 51,500 in 2017 to 79,500 in 2019. 2) Thanks to the company's strategic migration to high-end market and the expansion of offline SaaS merchants (the ARPU of offline SaaS products is higher, please refer to the acquisition case of Heading Information and Yazuo). The company's SaaS business APRU has increased significantly in recent years, from 2017 RMB 5,100 in the year rose to RMB 6,373 in 2019.

Looking ahead, considering 1) the company will continue to develop offline SaaS merchants in the future. 2) In the future, with the improvement and diversification of SaaS products of the company, we believe the dependence of SaaS products from the merchants will further increase, so the attrition rate of SaaS business paying merchants is expected to further decline. 3) The e-commerce model of private traffic management will be further popularized, and the number of Wei mall merchants will continue to increase. Based on the above three reasons, we believe that the number of paying SaaS merchants of the company will continue to increase in the future and is expected to reach 151 thousand in 2022, with a CAGR of 23.7% during 2019-2022. On the other hand, we believe that the ARPU of the company's SaaS business will continue to rise steadily in the future, thanks to the company's strategic migration to high-end market and the continuing expansion of offline SaaS merchants. The ARPU of SaaS business is expected to reach RMB 9,034 in 2022, 2019-2022 The CAGR is 12.3%. In summary, we predict that the company's SaaS revenue in 2020/2021/2022 will be RMB 6.95/9.72/1.36 billion, respectively, and the CAGR for 2019-2022 will be as high as 39.0%.

Targeted marketing Gross billing

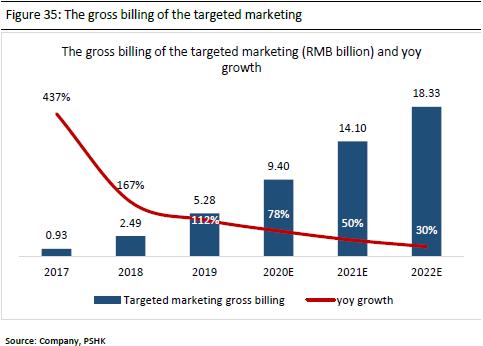

In the accounting perspective, there are two ways to recognize revenue for the company's targeted marketing business, the gross method and the net method. The difference between the two revenue recognition methods lies in the company's way of charging advertisers. If the company charges its advertisers in CPC (cost per click)/ CPM (cost per thousands), the net method is used to recognize revenue, and advertising rebates are recognized as revenue. On the contrary, if the company charges its advertisers in CPA (cost per action), the company adopts the gross method to recognize revenue. The gross billing (net of sales discounts granted to key customers and VAT) will be charged as revenue, with advertising platform's revenue share accounted as cost. Based on the complexity and misleading nature of this financial standards, we believe as compared as revenue, the gross billing of targeted marketing business can more clearly reflect the operational performance and growth of this business segment. The company's past gross revenue has maintained high growth, rising from RMB 933 million in 2017 to RMB 5.281 billion in 2019, with a CAGR of 138% during the period.

Considering 1) the new opportunities brought by the company's expansion to ByteDance platform 2) the additional targeted marketing needs from new merhcnats in the SaaS business 3) the increasing scale of Tencent's advertising and the increase in the advertising needs of merchants on the Tencent ecosystem. we believe that the gross billing of the company's targeted marketing business will maintain high growth in the future. We expect it to be RMB 9.40/141.0/18.33 billion in 2020/2021/2022, respectively, with a CAGR of 51% for the period 2019-2022.

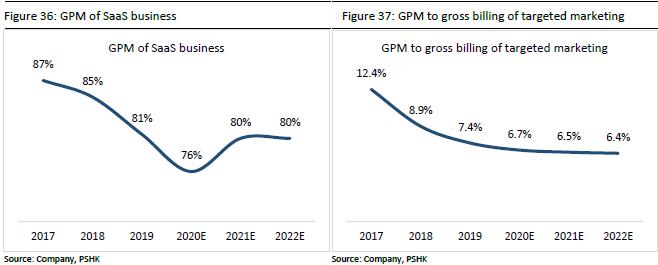

GPM and expense ratios

In recent years, the GPM of the SaaS business has declined, from 87.0% in 2017 to 80.5% in 2019. We believe that the gross profit margin will continue to decline in 2020, mainly because the company's new SaaS product research and development investment generally is amortized over 3 years and is included in the COGS. After the product development costs are fully amortized, gross profit margin is expected to recover. We predict that the company's GPM of SaaS business in 2020/2021/2022 will be 76%/80%/80%, respectively.

The company's GPM to gross billing of targeted marketing business also showed a downward trend in recent years, from 12.4% in 2017 to 7.4% in 2019. The main reason for the downward trend is that the company is gradually transforming to serve Tencent KA (key account) customers, and since the advertising gross billing of the KAs tend to be higher, hence, the rebates from Tencent advertising to the company are lower, which lowers GPM to gross billing. Considering 1) the proportion of the company's KA advertisers will further increase in the future 2) the company will continue to expand to Bytedance advertising platform, and the advertising rebates from the Bytedance advertising platform are generally lower than those from Tencent. We believe the GPM to gross billing of the company's targeted marketing business will continue the downward trend in the future and we expect it to be 6.7%/6.5%/6.4% in 2020/2021/2022, respectively.

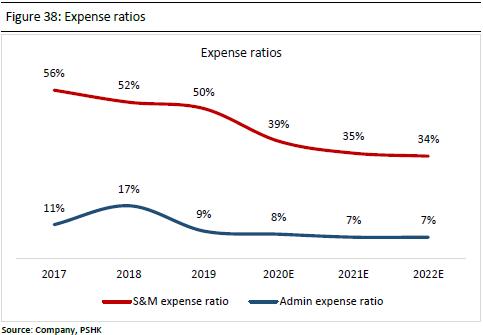

As for S&M expense ratio, as mentioned above on page 14-15, we expect the company's SaaS revenue share from direct sales will increase, thereby reducing the S&M expense ratio. We expect that the company's S&M expense ratio in 2020/2021/2022 to be 39%/35%/34%, respectively. We expect that the company's administrative expense ratio in 2020/2021/2022 will remain stable at 7%-8%.

�Valuation

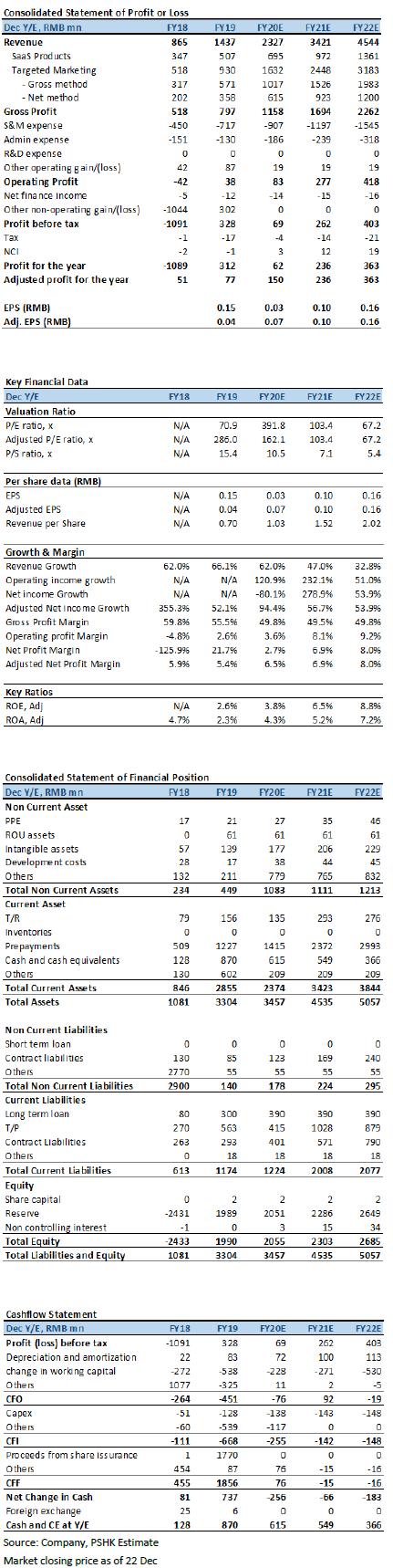

We forecast the company's 2020/2021/2022 adjusted NP to be RMB 150/236/363 million, revenue for SaaS business to be RMB 695/971/1361 million, NP for targeted marketing business to be RMB 383/579/739 million.

We have adopted SOTP to value the company. Considered its peer valuation multiples, we are giving target 2021 PS of 20x to the company's SaaS business, and a target 2021 PE of 18x to the company's targeted marketing business. We set the target stock price at HKD 15.04, with respective 2020/2021/2022 adjusted PE at 198x/127x/82x. We initiate with a Buy rating. (Market closing price as of 22 Dec) (exchange rate: RMB 0.88/HKD)

Risk

1) The expansion of SaaS customers is worse than expected 2) The increased industry competition 3) Advertising demand is less than expected 4) Targeted marketing business mainly relies on the cooperation with Tencent

Financial Statements

Click Here for PDF format...