Investment Summary

Update of sales volume in November: "Han" is getting better and the proportion of high-end models continues to expand

According to the latest data, BYD sold 53,943 vehicles in November, up 31% yoy and up 13% mom, including 26,700 new energy passenger vehicles, up 139.4% yoy and up 15.9% mom, 1,137 new energy commercial vehicles, up 109% yoy and down 3% mom, and 27,300 traditional fuel vehicles, up 11% yoy and down 9% mom.

The sales volume of new energy passenger vehicles showed strong growth momentum. The growth was mainly driven by pure electric models, up 128% yoy, which is resulted from Han EV. The hybrid vehicles witnessed a significant increase of 174%. The increase was mainly underpinned by Han DM and new Tang DM. The increase in fuel vehicles came mainly from Song Pro. In terms of product structure, the proportion of high-end models continued to expand.

BYD's new-generation flagship Han was launched in July. Its sales volume climbed to 7,545 vehicles in October, and reached 10,105 vehicles in November, mainly high-end versions. Currently, the delivery cycle of pre-sale orders is longer than two months. Therefore, we expect the Company's total vehicle sales volume will continue to soar at the end of the year.

Another popular model, the new Tang DM, has been improved in terms of the fuel consumption, interior trim, and power supply. Its product strength has also been further enhanced.

Regarding the cumulative sales in the past 11 months, the sales volume of BYD's automobiles, new energy passenger vehicles, new energy commercial vehicles and traditional fuel vehicles reached 418,000, 125,000, 8,251 and 183,000 vehicles,

respectively, down 16% and 36 % and up 14% and 6.3% yoy, respectively. Taking into account the low base in the same period last year, the effect of the auto show, and the mission at the end of the year, we expect the strong growth momentum in the fourth quarter will still continue.

Next year, BYD's Dynasty series will start a comprehensive upgrade. For new models equipped with blade batteries and new DM platform technology, the Company will further reduce costs and increase efficiency, lead technological innovation, and comprehensively enhance the core competitiveness of the product..

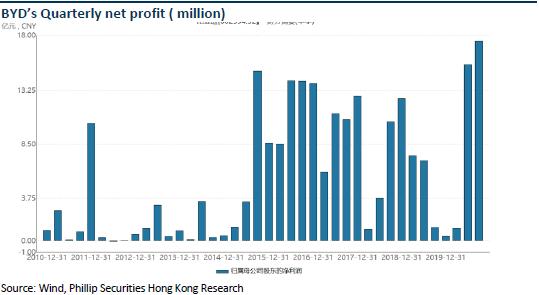

2020Q3 Result hit a record high

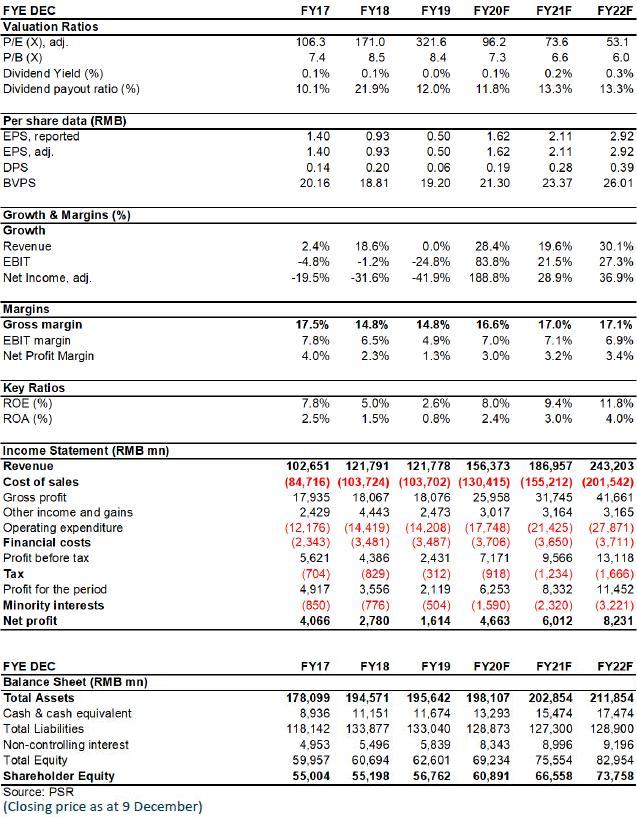

According to the Company's report for three quarters, BYD reported a revenue of RMB19.68 billion, RMB40.82 billion and RMB44.52 billion in the first three quarters of 2020, down 35.1% and up 28.1% and 40.7% yoy, respectively. The net profit attributable to the parent company was RMB113 million, RMB1.55 billion and RMB1.75 billion, respectively, down 85% and up 120% and 1362.7% yoy, respectively. Earnings in the third quarter hit a record high.

In terms of profitability, the gross margin in the first three quarters reached 17.7%, 20.5% and 22.3%, respectively, down 1.4 ppts, and up 5.2 ppts and 8.5 ppts yoy. The gross margin in the third quarter also set new record high for the Company. In addition to the low base in the same period last year, the substantial increase in gross margin was mainly due to the expanded proportion of high-end models in the automotive sector and the increased contribution of BYD Electronic(285@HK) (BYD Electronics recorded a net profit of RMB1.86 billion in Q3, up 312%).

The Company expects its net profit in the fourth quarter to be in the range of RMB786 million to RMB1,186 million, up 2356% yoy and down 43% qoq, respectively by the median. This is mainly based on expectations of the industry boom in the fourth quarter and sufficient orders in hand. We believe that the Company's guidance is conservative, and it is expected to exceed expectations in the fourth quarter.

Stock price catalyst lies in valuation reshaping

BYD has completed the introduction of strategic investment in the semiconductor business and the accelerated expansion of external supply customers for blade batteries. The spin-off listing of other sectors such as cloud rail, new energy commercial vehicles and photovoltaics may be successively achieved in the future. The improvement in operational efficiency and value reshaping brought about by the spin-off will push up the Company's current potential value.

It is worth noted that the Company announced the manufacturing of the customized D1 model in cooperation with DiDi. If the product strength is recognized, the sales volume of the 2B end is expected to achieve a breakthrough, while opening up the Company's imagination of future in-depth participation in the field of shared travel.

The Company recently announced that it intends to issue no more than 183 million H shares to raise funds for replenishing working capital, repaying interest-bearing debt, R&D investment, and general corporate purposes. We believe that although the additional issuance will dilute profits in the short term, it will help the Company move lightly in the critical period when it is about to enter a new development stage. Besides, it will help the Company rapidly expand production capacity and market share, advance its position on the high-quality track, and consolidate and expand its leading edge.

Investment Thesis

Therefore, although there are various challenges in the future, we believe that the Company is entering into a growth period with more stability and sustainability.

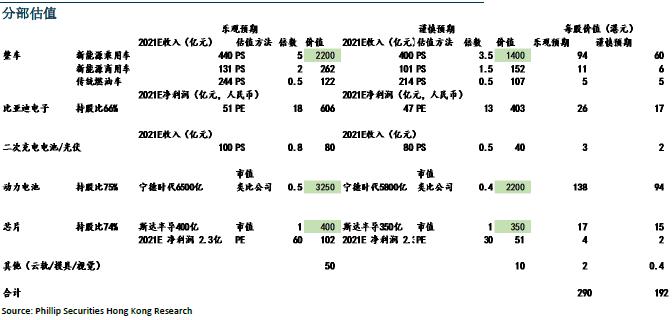

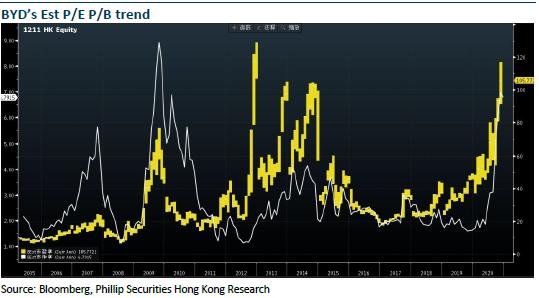

In terms of STOP valuation adopt, we give the original business (automobile, mobile phone, rechargeable battery and photovoltaic business) 139/89 HK$/per share, power battery business and semiconductor business from two assumptions of optimistic expectation and cautious expectation. 138/94 and 12.5/8.9 HK$/per share, the overall valuation is respectively 290/192 HK$/per share, implying 60% and 6% upside respectively. For comprehensive consideration, we given the target price of 241 HK$, corresponding to 2020/2021/2022 130 /99/72x P/E, 9.8/8.9/8.0x P/B, BUY rating.

(Closing price as at 9 December)

Risk

Sales of NEVs is not as good as expected

New business risk

Slow-down of Hand-set components business

Financials

Click Here for PDF format...