Investment Summary

Semir Group was established in 1996, opened the first Semir brand store in 1997, and started a brand extension strategy in 2002, founded the children's clothing brand "balabala" and established the company's predecessor. The company's mainly engaged in product design, brand management, supply chain management and channel development business. Its brands mainly include adult leisure brand "Semir", children's clothing brand "balabala", "MarColor" and "mini balabala". The company has now developed into a dual-leading position in the domestic casualwear clothing and children's clothing industries. According to the China National Garment Association, the company ranks 8th in the national apparel industry based on 2019 operating income. In addition, according to euromonitor, balabala ranks first in the children's clothing market with 6.9%, which is 5.3 pct higher than the second place, Anta Kid. In 2019, the company's revenue from children's clothing business was approximately RMB 12.66 billion, of which 2.97 billion came from the Kidiliz Group, which was transferred in September, an increase of 43.5% year-on-year, and its casual apparel revenue was RMB 6.54 billion, a YoY decrease of 3.6%.

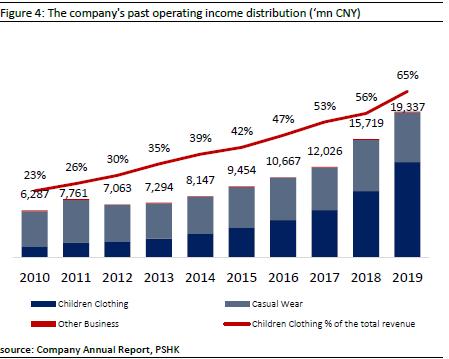

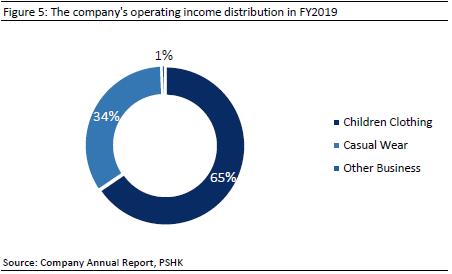

The company's revenue mainly comes from children's wear and casual wear business. Revenue from children's wear business has grown rapidly in recent years. The casual wear business maintained steady growth, with CAGR of approximately 4.28% from 2012 to 2019. In 2019, the company recorded a total of RMB 19.337 billion, of which 65.49% came from children's wear and 33.84% came from casual wear business. The proportion of children's clothing business revenue has continued to rise in the past decade. In 2017, it recorded RMB 6.322 billion, accounting for 52.56% of total 2017 revenue. For the first time, it surpassed the revenue contribution of casualwear business and became the company's major source of revenue.

Unlike women's clothing, men's clothing and sportswear, China's children's clothing industry is in a period of rapid growth and is a popular market segment in China's clothing industry. Because children are in the rapid growth stage, they have a higher demand for clothing replacement, and the replacement frequency is higher than that of adults. The average replacement is about 15-20 pieces per year, compared with about 10 pieces per year for adults. On the other hand, based on the Chinese people's concept of attaching importance to the next generation, the price sensitivity of children's daily expenses is relatively low and the pursuit of quality features. Compared with adult clothing, parents are more willing to consume and are willing to pay for children's clothing brands. In summary, China's children's clothing industry has a broad market prospect.

Valuation and Investment Recommendation

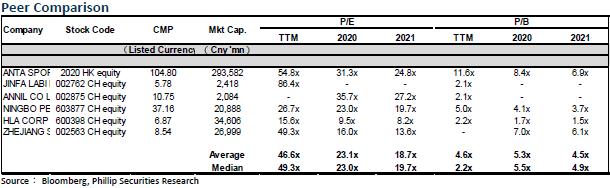

Semir Apparel has taken a leading position in the domestic children's and casual wear markets. We estimate that the company's FY20E/FY21E/FY22E net profit attributable to the parent will be RMB 576 million/1.441 billion RMB 16.79 billion, corresponding to FY20E/FY21E/FY22E earnings per share of RMB 21.35/53.38/62.21 cents, giving a target price of 12 months 10.68, P/E corresponding to FY20E/FY21E/FY22E of 50.0x/20.0x/17.2x.

(Current price as of November 18)

Risk

1) The impact of the new crown pneumonia continues 2) The positioning overlap between brands

Company Profile

Semir Group was established in 1996, opened the first Semir brand store in 1997, and started a brand extension strategy in 2002, founded the children's clothing brand "balabala" and established the company's predecessor. The company's mainly engaged in product design, brand management, supply chain management and channel development business. Its brands mainly include adult leisure brand "Semir", children's clothing brand "balabala", "MarColor" and "mini balabala". The company has now developed into a dual-leading position in the domestic casualwear clothing and children's clothing industries. According to the China National Garment Association, the company ranks 8th in the national apparel industry based on 2019 operating income. In addition, according to euromonitor, balabala ranks first in the children's clothing market with 6.9%, which is 5.3 pct higher than the second place, Anta Kid. In 2019, the company's revenue from children's clothing business was approximately RMB 12.66 billion, of which 2.97 billion came from the Kidiliz Group, which was transferred in September, an increase of 43.5% year-on-year, and its casual apparel revenue was RMB 6.54 billion, a YoY decrease of 3.6%.

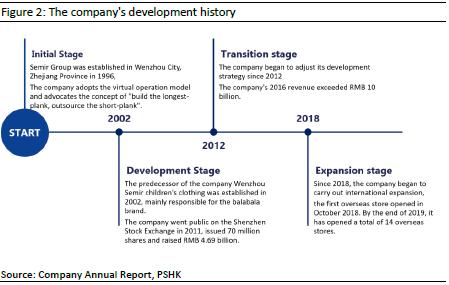

Company development process

The company's development history can be divided into 4 stages

Initial Stage (1996-2001)

Semir Group was established in Wenzhou City, Zhejiang Province in 1996, and opened its first Semir brand store in Xuzhou City, Jiangsu Province in 1997. The company adopts the virtual operation model and advocates the concept of "build the longest-plank, outsource the short-plank". Production and sales are outsourced. The company concentrates on R&D design, brand promotion and information construction.

Development Stage (2002-2011)

The predecessor of the company Wenzhou Semir children's clothing was established in 2002, mainly responsible for the design, outsourcing production and sales of the balabala brand. In 2007, the company rectified its structure and changed to a limited company and renamed Zhejiang Balabala childrens clothing Limited by Share Ltd (®ý¦¿¤Ú©Ô¤Ú©Ôµ£¸ËªÑ¥÷¦³¤½¥q) In 2008, the company reorganized its assets and acquired the Semir brand casualwear business from the controlling shareholder Semir Group and several actual controllers, and changed its name to Zhejiang Semir Garment Co., Ltd. (®ý¦¿´Ë°¨ªA¹¢ªÑ¥÷¦³¤½¥q). The company went public on the Shenzhen Stock Exchange in 2011, issued 70 million shares and raised RMB 4.69 billion.

Transition stage (2012-2017)

In response to changes in the industry, the company began to adjust its development strategy since 2012, including brand upgrades, establishment of channel models, product transformation, and supply chain optimization. At the same time, the company also began to implement the Amoeba management model, deepened the operation of the performance appraisal system, and established an incentive system and promotion system to increase the enthusiasm of employees. The company's 2016 revenue exceeded RMB 10 billion.

Expansion stage (2018-now)

Since 2018, the company began to carry out international expansion, actively carry out overseas mergers and acquisitions, cooperate with overseas designers, and opened up the first overseas store in October 2018. By the end of 2019, it has opened a total of 14 overseas stores.

Expand the brand matrix through different forms

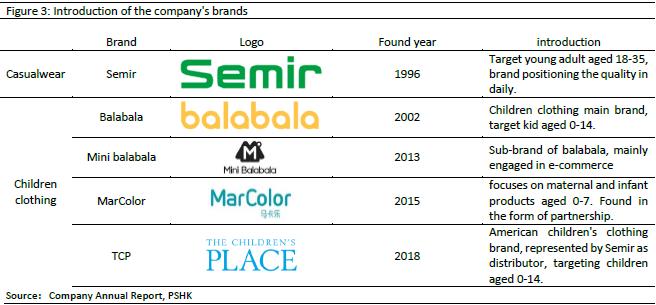

The company's business is mainly divided into casual wear and children's wear. Among them, casual wear is mainly based on the "Semir" brand, while the children's wear business is based on "Balabara". Semir brand was established in 1996, targeting customers aged 18-35, focusing on cost-effective products. The Balabala brand was founded in 2002. Its products are mainly professional and fashionable children's wear, targeting children's wear groups aged 0-14. In addition to the main brands, the company also adopted a multi-brand strategy to further cover the two major market segments. The company has established a rich brand matrix through endogenous cultivation, partnership system, acquisitions, and strategic cooperation.

Financial Analysis

Revenue analysis

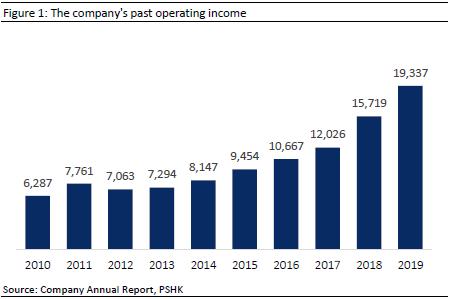

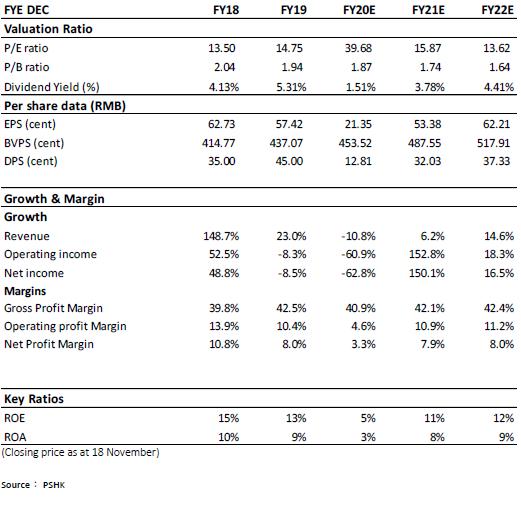

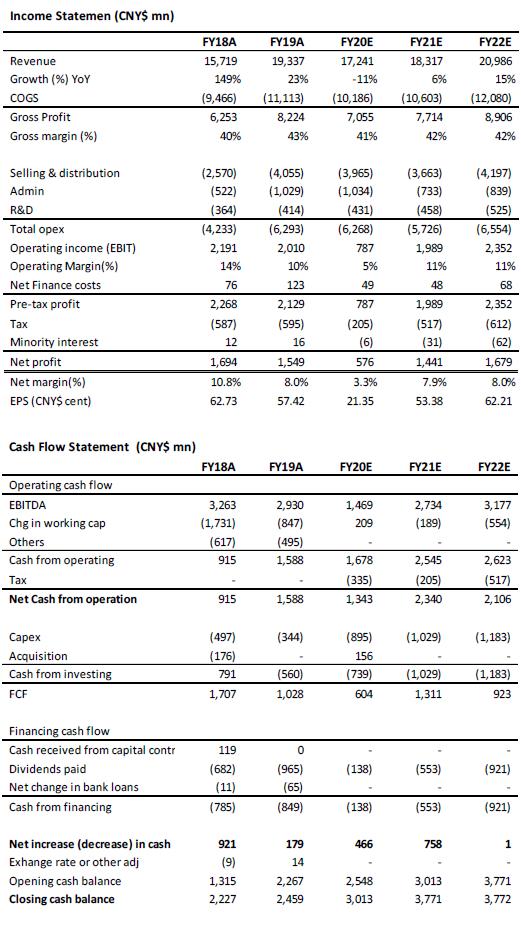

y adjusted its development strategy in 2012, its revenue increased YoY. From 2012 to 2019, the company's revenue and net income grew at CAGR of 15.47% and 10.54% respectively. For the whole year of 2019, the company achieved total revenue of approximately RMB 19.337 billion, an increase of 23.01% over the same period of the previous year, and net profit attributable to the parent of RMB 1.549 billion, a YoY decrease of 8.52%.

From the perspective of revenue composition, the company's revenue mainly comes from children's wear and casual wear business. Revenue from children's wear business has grown rapidly in recent years. The casual wear business maintained steady growth, with CAGR of approximately 4.28% from 2012 to 2019. In 2019, the company recorded a total of RMB 19.337 billion, of which 65.49% came from children's wear and 33.84% came from casual wear business. The proportion of children's clothing business revenue has continued to rise in the past decade. In 2017, it recorded RMB 6.322 billion, accounting for 52.56% of total 2017 revenue. For the first time, it surpassed the revenue contribution of casualwear business and became the company's major source of revenue.

�

Profitability

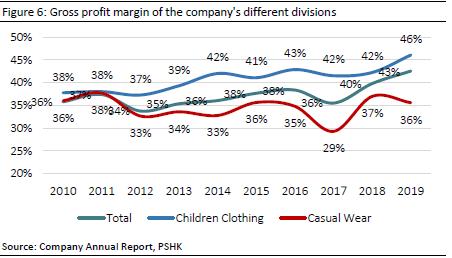

In terms of profitability, the company's GPM has continued to improve in the past three years. The GPM in 2017/2018/2019 were 35.51%/39.78%/42.53% respectively. The main reason is that the proportion of children's clothing business with higher GPM has increased. Drive the overall GPM. The GPM of the children's clothing business in 2017/2018/2019 was 41.52%/42.23%/46.06%, mainly due to the incorporation of Kidiliz, which has a higher GPM. In 2019, Kidiliz's GPM was 62.13%. The average GPM of the casual apparel business is about 35%. In 2017, due to inventory backlog and discount promotions, it was only 29.31%. The GPM of the business in 2018/2019 was 36.98%/35.60%, respectively.

Expenses for the period

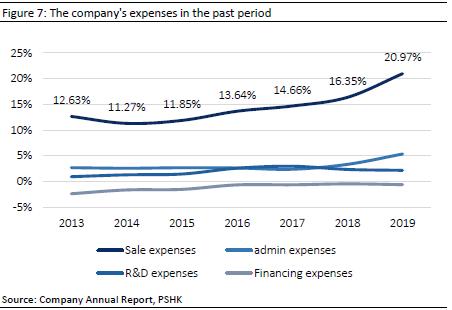

In the first three quarters of 2020, the company's expense of the period/total revenue increased by 5.39 pct to 33.36% YoY, of which the sales expense ratio increased by 3.8 pct to 26.42%, and the management expense ratio increased by 1.22 pct from the same period to 5.49%. Mainly due to the impact of the epidemic, the company increased its promotional discount when destocking.

In terms of the trend of the company's expense of period ratio,it has continued to rise, from 11.76% in 2010 to 27.80% in 2019, and the sales expense ratio and admin expense ratio increased by 11.7/3.36 pct respectively. The acquisition of Kidiliz has a significant impact on the company's sales expenses and management expenses. The sales expense ratio/management expense ratio increased by 6.31/2.95 pct from 2017 to 2019. Among the sales expenses, mainly due to Kidiliz's high-proportion direct sales model, the increase in salary, rental fees and promotional expenses incurred. Compared with 2017, the salary, rental and promotional expenses for the whole year of 2019 increased by nearly 89%, 92% and 125% respectively.

Casual wear Business

Semir, Quality in daily

In the early days of the product listing, the main target consumer group was young people aged 16-25. The products were divided into two major product lines: vitality and fashion. With the high growth of consumption in the domestic apparel market and younger consumption, Semir's brand revenue grew rapidly from 2008 to 2012. However, since 2012, competition in the apparel market has intensified, and channel and supply chain management have become a major challenge for the industry. In this context, the company's inventory backlog is serious, revenue has declined, and the relatively low level of income and purchasing power of brand-positioned consumer groups has begun to appear. The company began reforms in brand, channel and supply chain in 2012, and returned to the growth track in 2014. In 2019, the company officially proposed the development direction of focusing on new youth, expanding the target customer group upward, and positioning young people aged 18-35 years old and put forward the brand value proposition of "quality in daily ", and pay more attention to consumers` daily life in terms of design, materials and collocation.

Invest resources in R&D

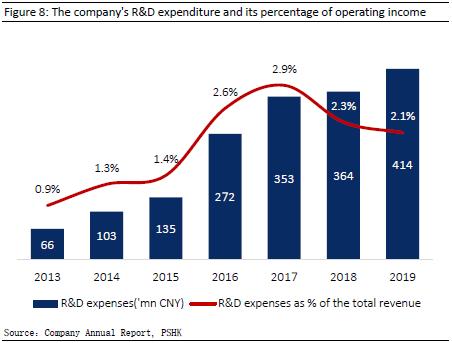

In recent years, the company has continued to increase its resources in design and R&D. In 2019, the company's R&D expenditure was approximately RMB 410 million, accounting for 2.14% of operating income. Compared with other leading casual apparel brands in China, Semir's R&D expenses and expense ratios are both the highest. During the same period, the research and development expenses of HLA, Peacebird and Metersbonwe fashion were RMB 67 million, 108 million and 109 million respectively. The company has independently established 48 research and development projects, 1 invention patent authorization, 7 utility model patent authorizations, and 15 appearance design patent authorizations, including the core fabric "Semir Cotton" used throughout the seasons of the main products. Create skin-friendly, breathable and soft fabrics to meet consumer needs.

IP co-branded response was enthusiastic

In order to increase brand exposure, the company continues to increase cooperating with other designers. In 2019, it launched a cooperative limited product series with brands such as Meihua and Tyakasha, and cooperated with well-known designer Li Dengting on the New Year's New Year series which brought a good response. In July 2020, the company signed a contract with the FunPlus Phoenix E-sports Club, an opinion leader in the field of e-sports, and launched a new brand campaign. The company demonstrates the integration of the brand with young people in the cooperation, and the co-branded products use the language that only the old fans of e-sports can understand as the product design, which is recognized by the younger generation.

Children's clothing business covers all ages

In terms of children's clothing, the company has achieved full-category and full-age (0-14 years) coverage through a multi-brand matrix. Since its listing, the children's clothing business has continued to record positive growth. From RMB 550 million in 2008 to RMB 12.66 billion in 2019, the CAGR was as high as 33%. Except for the LSD growth in 2012 when the industry faced inventory pressure, it increased by more than 20% YoY in other periods. In 2018, the company, without the impact of Kidiliz consolidation, children's clothing revenue still recorded RMB 8.047 billion, YoY increase of 27.30%. In 2019, Kidiliz contributed 2.969 billion yuan in revenue. After excluding Kidiliz's revenue contribution, the company's children's clothing business recorded 9.69 billion yuan, a year-on-year increase of 20.47%.

Balabala

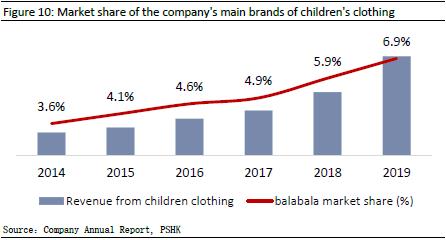

The main brand of children's clothing business, balabala, was founded in 2002. It is targeted at the general children's market. Anta Kid in second place leads 5.3 pct. At the same time, the company is also distributor of North American children's clothing brand ¡§The Children's Place¡¨ and other brands.

The company expands the children's clothing multi-brand matrix through self-cultivation, partnership model and brand distributor. Among them, Mini Balabala was found by the company in 2013 and focuses on online sales. In 2019, the brand growth rate reached 68%. In the same year, it entered the top 5 children's wear list on Tmall Double Eleven festival. The other brand, MarColor, focuses on maternal and infant products aged 0-7. It was founded in 2015 as a partner and has an outstanding performance, with a growth rate of 59% in 2019.

Industry Analysis

Industry characteristics make product replacement rate high

Unlike women's clothing, men's clothing and sportswear, China's children's clothing industry is in a period of rapid growth and is a popular market segment in China's clothing industry. Because children are in the rapid growth stage, they have a higher demand for clothing replacement, and the replacement frequency is higher than that of adults. The average replacement is about 15-20 pieces per year, compared with about 10 pieces per year for adults. On the other hand, based on the Chinese people's concept of attaching importance to the next generation, the price sensitivity of children's daily expenses is relatively low and the pursuit of quality features. Compared with adult clothing, parents are more willing to consume and are willing to pay for children's clothing brands. In summary, China's children's clothing industry has a broad market prospect.

China's children's clothing market is in a growth stage

Compared with other countries, China's children's clothing market started late and began to develop in the early 1990s. With the improvement of people's living standards, the demand for children's clothing has begun to show a diversified trend. At the same time, domestic children's clothing brands have gradually risen, and overseas children's clothing brands have also entered the market. However, compared with the men's and women's clothing market, the overall development of the Chinese children's clothing market is still in the early stages of development.

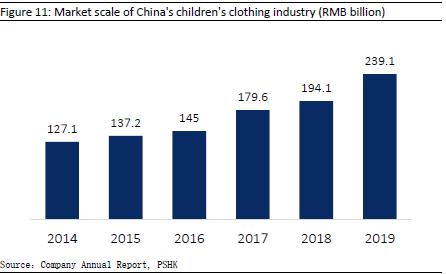

Among all clothing sub-sectors, the boom of the children's clothing market is second only to sportswear, and the market scale has grown relatively fast. According to Euromonitor statistics, China's children's clothing market reached 239.15 billion yuan in 2019, and the CAGR reached 13.5% from 2014 to 2019.

As the post-80s/90s enter the peak of marriage and childbirth, starting in 2012, China ushered in the fourth baby boom. At the same time, in November 2013 and October 2015, China successively relaxed the "one-child" policy and implemented "two-child " policies. Driven by the dual factors of the baby boom and the liberalization of the second-child policy, the domestic second-child fertility rate has seen a significant increase. The post-80s and post-90s parents have a stronger concept of prenatal and post-natal care. In the context of the rising per capita income of national residents, the per capita consumption level of children's clothing in China continues to increase. According to Euromonitor's statistics, in 2019, the per capita consumption of children's clothing in China reached RMB 1,018, and the CAGR reached 12.6% from 2014 to 2019. The growth rate was relatively fast and became the main driving force for the growth of China's children's clothing market.

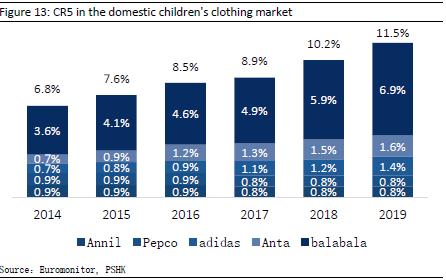

Market concentration continues to increase

Compared with adult wear, children's wear has lower fashion demand and higher functional demand. Therefore, the scale effect of enterprises is more obvious, and the industry concentration continues to increase. From 2014 to 2019, the CR5 of China's children's clothing industry increased from 6.8% to 11.5%, of which balabala accounted for 6.9% in 2019, making it the industry's number one leader. In the period of a weak economy, leading companies rely on their excellent inventory management capabilities and pipeline operating efficiency to cross the down cycle, and their market share will be further increased, accelerating the survival of the fittest in the industry, and thereby steadily increasing industry concentration.

On the other hand, the children's clothing industry is easier to achieve increased concentration than adult clothing. The main reason is that from the demand side, children do not have the ability to consume, and the decisions are made by parents. When purchasing, comfort and safety are more important than fashion, and large-scale enterprises can produce standardized products. It is easier to realize the scale effect, and the industry concentration is thus improved. On the other hand, the younger generation of consumers has a new consumption concept and has a stronger willingness to consume branded and quality products. At the same time, the increase in the disposable income of residents is conducive to consumption upgrades, so branded children's clothing will be more accessible Market share and expand concentration. On the supply side, the channels and industry specifications of small and medium brands are relatively uncompetitive. Online and offline traffic is increasingly concentrated on brands. Maternal and child consumption is a type of consumption that focuses on physical experience. Offline channels have become increasingly fierce for the survival of the fittest by brands.

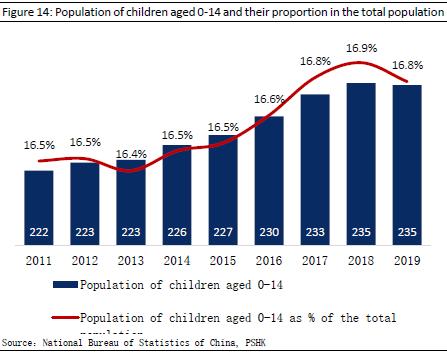

According to data from the National Bureau of Statistics of China, the number of children in China has shown an overall upward trend from 2010 to 2019; in 2019, the number of children aged 0-14 in China was 235 million, and the population accounted for 16.78%. The huge number of children is the basis for the vigorous development of China's children's clothing industry. In the context of the continuous popularization and strengthening of the concept of prenatal and postnatal care, the per capita consumption expenditure of children's clothing in China will continue to rise, providing support for the continued expansion of the children's clothing industry market. It is expected that the size of China's children's clothing market will grow rapidly with a CAGR of 12.1% in the next few years, and the market size is expected to exceed 400 billion yuan in 2024.

Company competitive advantage

Impressive sales during 11 - 11 festival

While the company is developing offline channels, its online sales channels have performed well, maintaining a rapid development trend. In 2019, Tmall Double 11 set a new record of single-day transaction volume for Double 11 with RMB 1.380 billion. Children's clothing brand balabala sold 510 million yuan in a single store on Tmall Double 11 in 2019, ranking first in the maternal and child industry for the fifth consecutive year, while the baby brand Minibalabala It also ranks fifth in the Tmall children's clothing industry. In terms of marketing, the company engaged in live broadcasts and short videos which are popular in recent years. Semir's e-commerce brands Semir and balabala are eye-catching. In Tmall Double 11, balabala ranked first among brands in the maternal and infant industry. In terms of video, Semir's e-commerce's coverage rate of short videos on the entire storefront in 19 years increased by 136% YoY, while TikTok's video playback volume exceeded 30 million.

Spin off Kidiliz business

In order to expand the company's overseas business, Semir completed the acquisition of Sofiza SAS for 110 million euros in cash in 2018, thereby taking over the French mid-to-high-end children's Kidiliz. However, due to the continued economic downturn in Europe in the past two years, the main brand business revenue of the Kidiliz Group has continued Decline, the number of stores has decreased year by year, and the main business has suffered serious losses. Kidiliz's high-proportion self-operated model has also increased the company's sales expenses. In 2019, Kidiliz Group's revenue was 3.02 billion yuan, but its operating profit lost 297 million yuan, and its net loss was 307 million yuan. Especially after the global outbreak of the COVID-19. Kidiliz Group's main operating regions in France and Italy and the entire European market economy suffered heavy losses. The operating risks were further amplified, which adversely affected Semir's performance and brought significant damage to future operating results. Certainty.

On July 20, Semir apparel issued an announcement announcing that it intends to sell 100% of the assets and business of its wholly-owned subsidiary French Sofiza to Semir Group Co., Ltd. and the acting in concert with the controlling shareholder. After completing the equity transfer in September, the Semir Group promised that during the holding of Sofiza's assets and interests, Sofiza's assets will not develop new business operations or expand existing businesses in China. Kidiliz released the report in September, and the losses from July to August are still recorded in the report.

Valuation and Investment Recommendation

Semir Apparel has taken a leading position in the domestic children's and casual wear markets. The acquisition of Kidiliz's business in 2018 has brought significant revenue growth to the company, but at the same time it has also significantly increased the company's period expenses. In addition, the epidemic situation in Europe has not improved. Kidiliz The loss brought by the company expanded. The company is expected to improve its profitability after divesting Kidiliz. The company has a leading advantage on the children's clothing track and is expected to bring continuous growth to the company.

Based on 1) After the divestiture of Kidiliz, it will have a short-term impact on the company's children's clothing segment revenue, but the company has its own brand balabala in the children's clothing business to continue to provide growth, and it is expected that the children's clothing business will be stable and expanded. 2) After the divestment of Kidiliz, the company has improved its management and sales expenses, and its overall profitability has been improved. We estimate that the company's FY20E/FY21E/FY22E net profit attributable to the parent will be RMB 576 million/1.441 billion RMB 16.79 billion, corresponding to FY20E/FY21E/FY22E earnings per share of RMB 21.35/53.38/62.21 cents, giving a target price of 12 months 10.68, P/E corresponding to FY20E/FY21E/FY22E of 50.0x/20.0x/17.2x.(Current price as of November 18)

Risk

1) The impact of COVID-19 continues

2) Overlapping positioning between brands

Financials

Click Here for PDF format...