Investment Summary

Razer (the Company) is the world's leading lifestyle brand for gamers. The triple-headed snake trademark of Razer is one of the most recognized logos in the global gaming and esports communities. With a fan base that spans every continent, the Company has designed and built the world's largest gamer-focused ecosystem of hardware, software and services.

The world's largest integrated ecosystem brings a superior life experience

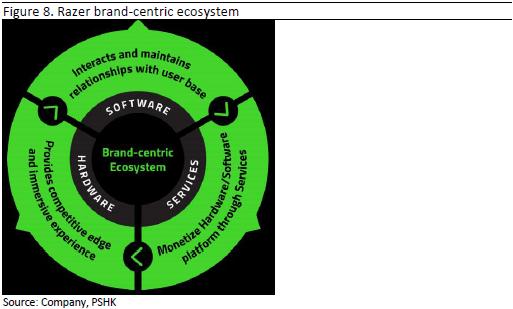

The Company builds an integrated ecosystem of "hardware, software, and services" for players through its own product lines and services. The core of the Company's ecosystem is the Razer software platform. The Company's platforms include Razer Synapse, Razer Chroma, and Razer Cortex. The Company uses these software products to maintain interaction with users to collect data for analysis (including user game performance indicators, behavioral data, and game preferences, etc.), which able to gain an in-depth understanding of the user base. Most of the Company's hardware products are "connected devices" which can connect to the ecosystem through software. For example, users use the Razer Chroma Symphony Connection Module to connect the mouse, keyboard, and computer case to bring a unique illusion lighting experience. After successfully attracting these users to become a loyal user, the Company can monetize its business through Razer Gold and Fintech business.

The core business continues to benefit from ¡§stay-at-home"

The global 'stay-at-home` situation has boosted user engagement with gaming and esports to record levels. The Company's 2020 interim results performed strongly. Revenue hit a record high in history, reaching US$447.5 million, up by 25.3% year-on-year, mainly due to the strong growth of the entire peripheral equipment portfolio. Among them, the hardware business increased by 26% year-on-year to US$382.7 million; the revenue of the software and services segment increased by 79.3% to US$64 million. Gross profit improved by 30.1% next year to US$98.53 million, and gross profit margin improved from 21.2% in the same period last year to 22.0% in the same period this year.

Monetize the brand through financial technology

The Company was founded in 2005. Over the years, it has established a brand popular among young people with high-quality products and services. The Company has one of the largest online social media followings globally among games and esports brands. As of October 15, 2020, the Company had more than 10 million "likes" on Facebook, 6.19 million followers on Instagram, 3.34 million followers on Twitter, 1.72 million subscribers on Youtube, and 440 thousand followers on Weibo, and the software business had over 100 million registered users. When these users recognize the brand, they will be willing to use other products or services launched by the Company. We believe that the Company can take advantage on its brand and huge fans base to grow rapidly in the Fintech business.

Valuation and Investment Recommendation

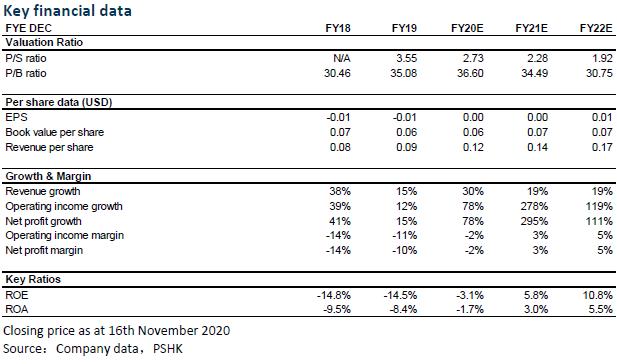

As of the closing price on November 16, the Company's dynamic price-to-sales ratio (TTM) was 3.21. We believe that based on the Company's sound fundamentals, the Company is the industry leader and its business has grown strongly. We give the Company a target price to sales ratio of 3.0x in 2021.We expect the Company's 2020/2021/2022 revenue per share to be US$0.12/0.14/0.17, and a twelve-month target price of HK$3.27, corresponding to the P/S ratio of the revenue per share for 2020/2021/2022 is 3.58x/3.00x/2.52x. Buy rating is given for the first coverage. (Exchange rate: 7.78 USD/HKD) (Current price as of 16th November 2020)

Industry analytics

With the rapid growth amid rising consumer interest and publisher investment¡Acompetitive gaming¡]E-sports¡^have developed rapidly in the past few years and became new growth driver in the game field. The global game peripherals market has emerged with the launch of various games such as first-person shooting¡Breal-time strategy¡Bmultiplayer online battles, and massively multiplayer online role-playing.

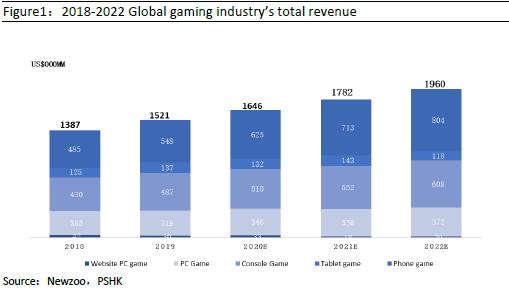

Steady growth in the global gaming industry

With the increased penetration of the Internet, the global game market has continued to grow. According to Newzoo, the global gaming industry's total revenue recorded US$152.1 billion in 2019, exceeding the combined revenue of the film and music industries. From 2018 to 2022, the global game market revenue rose from US$138.7 billion to US$196 billion, with a compound annual growth rate of 9%. In 2019, mobile games (smartphone and tablet games) are the largest segment, accounting for 45% of the market size, the console market is the second with 32%, and PC games are the third with 21%. They expect that mobile games will continue to grow, while the console market will maintain its share with the launch of Sony's Play Station 5 (PS5), and PC games will maintain steady growth due to the continuous launch of competitive games, but the market share will reduce.

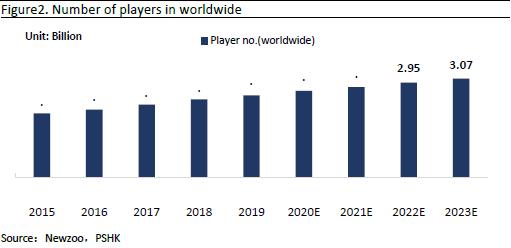

The number of players in worldwide continues to grow

According to Newzoo, in 2019, the number of active players worldwide was approximately 2.5 billion. As the number of active players will grow at a compound annual growth rate of 4.7%, starting from 2019, it is expected that this number will reach approximately 3.1 billion by 2023. The growth is driven by emerging markets, mainly due to the penetration rate of the Internet and the popularity of smart phones.

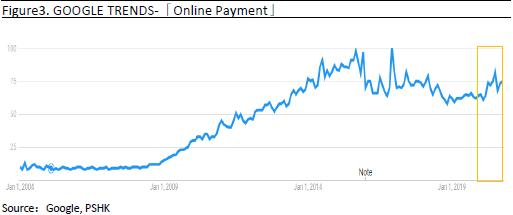

Covid-19 accelerates the development of electronic payment

With the continuous advancement of technology and the increase in mobile Internet penetration, global consumer payment methods have changed in recent years, and the application of electronic payments in various industries continued to increase. Especially with the emergence of COVID-19, consumers tend to reduce cash transactions in order to reduce the health risks caused by exposure to cash when making payments, and the utilization rate of contactless electronic payments has increased significantly. From the latest Google Trends search trends, the number of searches for the word "Online payment" rose in 2009. From February 2020 to August 2020, the search for "Online Payment" increased by 34%. As cashless payment methods are widely accepted by consumers, electronic payment instead of cash will become a global trend.

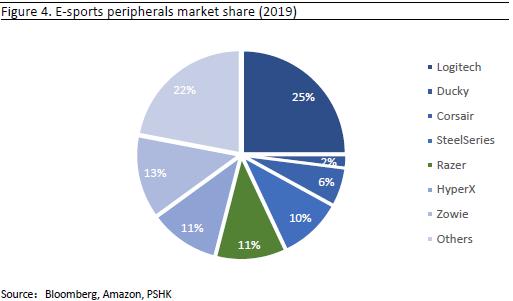

With industry consolidation, market concentration will increase

The industry is in monopolistic competition. According to Bloomberg, Logitech is the leader in the gaming peripherals industry, with a market share of 25%. Zowie ranks second with a market share of 13%. Razer ranked third with 11%. As players continue to search for the best specifications and features, some companies that lack innovation and cost control capabilities will gradually be eliminated, and market-leading companies can take the opportunity to slowly expand.

Company profile

Razer Founded in 2005, Razer has dual headquarters in Irvine and Singapore. It has 18 offices around the world. It is known as a world's leading lifestyle brand for gamers. It was listed on the main board of Hong Kong exchange in 2017. The Company's main business includes 1) hardware business, 2) software business, and 3) services.

1) Hardware business refers to the development and sales of game peripherals and systems(laptops)

The Company's hardware, which includes premium gaming peripherals (including high-precision mice, fully customizable keyboards, audio devices, mouse mats and gaming console controllers). It's hardware won numerous awards from major magazines over the years. For example, Razer was awarded the ¡§Best of CES¡¨ by the US Consumer Electronics Show, which is the eighth time the Company won this honor.

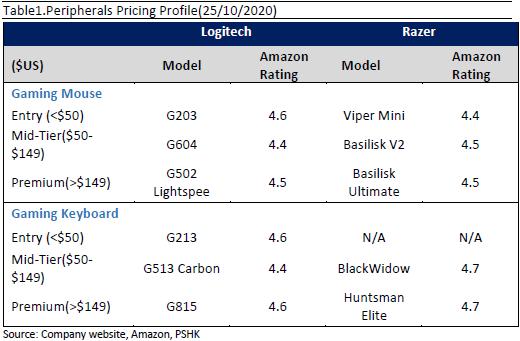

The price range of Razer's product line varies, but gamers who constantly seek the best specifications and features tend to purchase the best devices they can afford. The Company's gaming mouse and gaming keyboard retail for $25-$150. According to Amazon.com, Razer's mid-to-high-end products score higher than Logitechs`. The Company also announced that its products sales well on Amazon Prime Day dated 13-14 October 2020, In particular, its PC game mice harvested seven out of the top ten spots, and eight out of ten for its game keyboards. It can be seen that Razer's products are popular in the industry.

System products refers to the sale high-end gaming laptops, external graphics card boxes (eGPUs), chassis, computer accessories, etc. According to company report, its premium gaming laptop brand ranks as first in the United States. Razer's laptops are developed in cooperation with Intel and Nvdia, which are highly efficient and portable without losing a sense of style.

2) The software business refers to Razer's unique ecosystem. The core part of the Company's ecosystem is the Razer software platform. The Company's platforms include the Internet of Things platform Razer Synapse, a software platform for users to use hardware devices; Razer Chroma, its exclusive RGB lighting technology system; and Razer Cortex, a full-featured game launcher, game optimization program, Game aggregator and price comparator.

3) The service business includes Razer Gold virtual credit points and Razer Fintech.

Razer Gold virtual credit score is one of the world's largest independent virtual credit score platforms for digital entertainment. Players can purchase zGold (virtual points) and exchange it for digital content and items from various content providers. Since the Company's comprehensive acquisition of "MOL Global" in 2018, the Company has increased its business development. In 2020 interim results, users in more than 130 countries can now purchase Razer Gold virtual credits from more than 4 million channel touchpoints.

Razer Fintech is mainly to provide online and offline e-wallet solutions for business to business (B2B) and business to customer (B2C). According to the Company's 2020 interim results, Razer Fintech has generated a total payment transaction size of US$1.8 billion (2019: US$2.1 billion). The Company also takes its brand advantages to extend its financial business to the Razer Youth Bank platform, providing young people with a comprehensive banking service experience.

�Investment Highlights

The world's largest integrated ecosystem brings a superior life experience

The Company builds an integrated ecosystem of "hardware, software, and services" for players through its own product lines and services. The core of the Company's ecosystem is the Razer software platform. The Company's platforms include Razer Synapse, Razer Chroma, and Razer Cortex. The Company uses these software products to maintain interaction with users to collect data for analysis (including user game performance indicators, behavioral data, and game preferences, etc.), which able to gain an in-depth understanding of the user base. Most of the Company's hardware products are "connected devices" which can connect to the ecosystem through software. For example, users use the Razer Chroma Symphony Connection Module to connect the mouse, keyboard, and computer case to bring a unique illusion lighting experience. After successfully attracting these users to become a loyal user, the Company can monetize its business through Razer Gold and Fintech business.

The core business continues to benefit from ¡§stay-at-home"

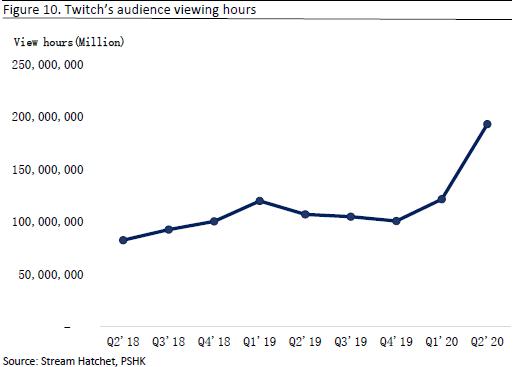

The global 'stay-at-home` situation has boosted user engagement with gaming and esports to record levels. The Company's 2020 interim results performed strongly. Revenue hit a record high in history, reaching US$447.5 million, up by 25.3% year-on-year, mainly due to the strong growth of the entire peripheral equipment portfolio. Among them, the hardware business increased by 26% year-on-year to US$382.7 million; the revenue of the software and services segment increased by 79.3% to US$64 million. Gross profit improved by 30.1% next year to US$98.53 million, and gross profit margin improved from 21.2% in the same period last year to 22.0% in the same period this year. The software business continued to expand. The total number of accounts increased by 42.8% year-on-year to approximately 100 million, and monthly active users surged by more than 45%. The increase was mainly due to the increase in games, e-sports and live broadcast activities, which drove the strong growth of the Company's software product portfolio. According to Stream Hatchet, the viewing hours of game video streaming platform Twitch surged by 83.1% year-on-year and 58.7% quarter-on-quarter in the Q2 of 2020. Looking ahead, Nvidia's launch of RTX 30 series graphics cards in October 2020 will take PC players` experience to a higher level, while Microsoft and Sony will launch Xbox Series-X and PS5 respectively at the end of the year. We think this will indirectly bring more revenue to the Company next year.

Monetize the brand through financial technology

The Company was founded in 2005. Over the years, it has established a brand popular among young people with high-quality products and services. The Company has one of the largest online social media followings globally among games and esports brands. As of October 15, 2020, the Company had more than 10 million "Likes" on Facebook, 6.19 million followers on Instagram, 3.34 million followers on Twitter, 1.72 million subscribers on Youtube, and 440 thousand followers on Weibo, and the software business had over 100 million registered users. When these users recognize the brand, they will be willing to use other products or services launched by the Company. We believe that the Company can take advantage on its brand and huge fans base to grow rapidly in the Fintech business.

The Company is actively deploying in the financial field. The Company announced that it had reached a strategic cooperation with Franklin Resources Inc. on digital wealth management cooperation. Through this cooperation, the Company and Franklin Templeton will jointly design and create a new-generation digital wealth management platform, providing digital wealth management services and multi-asset solutions, covering investment themes and related investment portfolios, regular savings plans, currency Market funds, other products and investment tools, etc. Franklin Templeton is one of the world's largest asset management companies. It has an absolute advantage in financial management. However, traditional fund companies may not know what young people need and may not bring the experience young people want today. Razer can make up for its shortcomings. The Company clearly understands the needs of young people and brings them a comprehensive banking service experience. In addition, the Company submitted an application for a digital banking license to the Monetary Authority of Singapore this year. The partners include FWD, Sheng Siong Holdings Pte Ltd and Linksure Global, etc. Long-term integration of lifestyle experience with digital banking platforms will reshape the banking industry for the younger generation.

Besides, the Company announced on October 5, 2020 that it will cooperate with Visa, a multinational financial services corporation, to launch the "Razer Card". In addition to basic credit card functions, its biggest feature is that users will flash green when paying with physical cards. The LED lights can foresee that the Company's future digital banking image will be unique and bright, and it will be able to create a profound brand image among young people. Compared with other new digital banks that use high-interest savings or consumption rebates to attract new customers, their customer acquisition costs will be lower and customer retention rates will be higher. In addition, the Company may develop virtual currency transactions in the future. Virtual currency refers to the use of digital accounting to replace physical currency transactions. In fact, zGold itself is also a type of virtual currency. Most of Razer's users are millennial consumers, and their acceptance of virtual currency is very high, and the virtual currency market has huge room for growth.

In addition, Razer Pay is currently one of the largest O2O digital payment networks in Southeast Asia. It's online payment gateway provides more than 110 payment options and is powering a list of blue-chip merchants including Lazada, Grab and Uniqlo. The long-term attractiveness of the Southeast Asian market lies in its demographic advantage. There are about 600 million young people in the region and the middle-class population in the region is growing rapidly, and the Southeast Asian regional government 's favorable policies such as increasing infrastructure construction are all conducive to the continued economic growth of the region and bring great business opportunities to companies operating in the region.

Financial Analysis

Revenue analysis

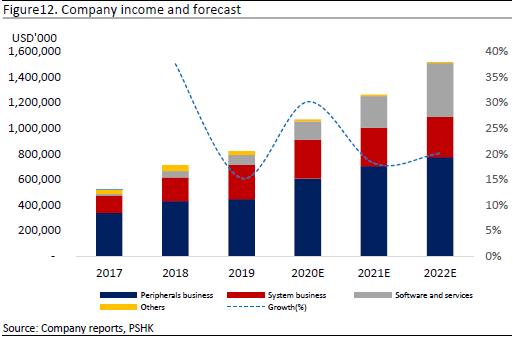

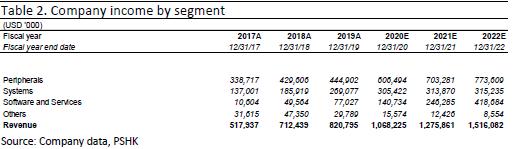

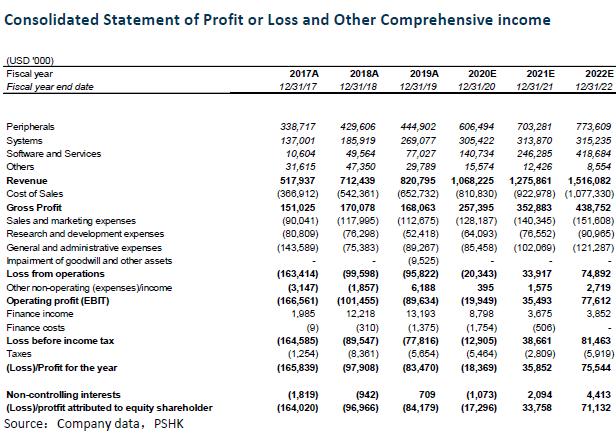

The Company's revenue is mainly divided into three parts, including 1) peripherals business, 2) systems business, and 3) software and services. Among them, the Company's peripherals business revenue for 2017/2018/2019 was US$340/430/440 million, accounting for 65.4%/60.3%/54.2% of total revenue, and the compound annual growth rate was 14.6%. As the supply chain was affected by the COVID-19 in the first half of 2020, the supply chain did not recover until mid-March, resulting in a delay in the release of new products in late April. However, the management indicated that users have strong demand for their products, coupled with the recovery of the supply chain and the advent of different holidays (such as Double 11, Thanksgiving, etc.), we expect strong revenue growth in the second half of the year. In summary, we estimate that the Company's hardware business revenue for 2020/2021/2022 will be US$606/703/773 million, a year-on-year increase of 36.3%/16%%/10%.

The Company's system business revenue for 2017/2018/2019 was US$137/185/269 million, accounting for 26.45%/26.1%/32.78% of the total revenue, with annual compound growth rate of 40%. The management expected the release of the new product series of Blade, the business recorded double-digit growth year-on-year in May and June. Based on our analysis of the Company in the previous article, we expect that the Company's system business will accelerate growth in 2020/2021/2022. We expect the Company's software business revenue for 2020/2021/2022 to be US$ 305/313/315 million, year-on-year. An increase of 13.5%/2.77%/0.43% year-on-year. The 2017/2018/2019 software and services revenue was US$10.6/49.6/77.0 million, accounting for 2.05%/6.96%/9.38% of the total revenue, respectively, with a compound annual growth rate of 170%. and we expect the Company's 2020/2021/2022 service business revenue will be US$141/246/418 million, an increase of 82.7%/75%/70% year-on-year. All in all, we forecast total revenue for 2020/2021/2022 is US$107/128/152 million respectively. The year-on-year growth was 30%/19%/18% respectively.

Costs and expenses analysis

The main cost of the Company is the cost of sales, and the main expenses are sales and marketing expenses, research and development expenses and general and administrative expenses. In 2019, they were US$650/110/52/89 million, accounting for 79.52%/14%/6%/11% of revenue. In terms of sales costs, considering that the Company has begun to provide users with more services and software services, we expect that the Company's sales costs as a percentage of revenue will gradually decline in 2020-2022, and they will be 75.90%/72.20%/71.10%, respectively. This means that we expect the Company's gross profit margin to be 24.1%/27.8%/28.9% in 2020-2022. We believe that sales and marketing expenses, R&D expenses, and general and administrative expenses will be reduced to a certain income ratio due to operating levers. Based on the above, we estimate that the operating costs of the Company in 2020-2022 will be US$ 1.9/1.23/1.45 billion.

EBIT margin analysis

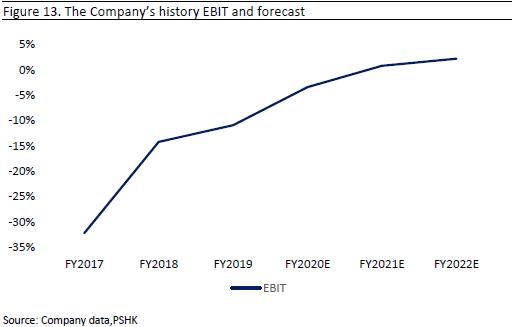

The Company's operating profit (EBIT) margin has remained stable in the past three years, from a negative 32% in 2017 to a negative 11% in 2019. Mainly because the Company has been strictly controlling operating costs and actively exploring new growth drivers. We expect the Company to benefit from the housing economy in 2020. As one of the leaders in e-sports peripheral products, the Company will seize the opportunity to further narrow its operating profit margin to minus 2%. In 2021-2022, the operating profit margin will continue to rise due to the increase in the proportion of software and service businesses. We expect the Company will start to turn positive and reach 2.8% in 2021.

Valuation

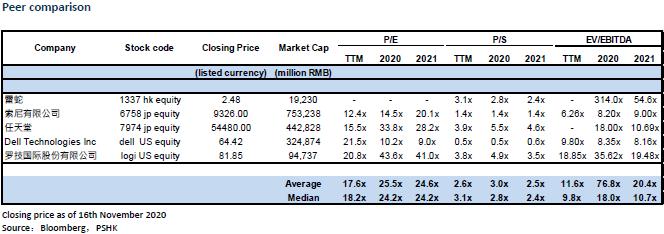

As of the closing price on November 16, the Company's dynamic Price-to-Sales ratio (TTM) was 3.21x. We believe that based on the Company's sound fundamentals, the Company is the industry leader and its business has grown strongly. We give the Company a target price to sales ratio of 3.0x in 2021.

We expect the Company's 2020/2021/2022 revenue per share to be 0.12/0.14/0.17 U.S. dollars, and a twelve-month target price of HK$3.27, corresponding to the P/S ratio of the revenue per share for 2020/2021/2022 is 3.58x/3.00x/2.52x. Buy rating is given for the first coverage. (Exchange rate: 7.78 USD/HKD) (Current price as at 16th November 2020)

Risks

1) COVID-19 outbreak again

2) E-sports growth not as expected

3) The Company's products fail to cater the user trends

Financial statements

Click Here for PDF format...