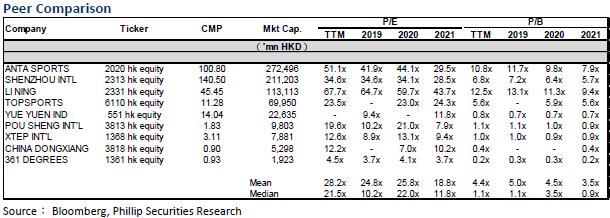

Investment Summary

Xtep International's main brands recorded a MDS increase in retail sell-through in the Q3, and the discount level was flat QoQ , higher than normal. Inventory levels have improved on a quarterly basis, and retail inventory turnover has been shortened to approximately 5 months. Based on the operating data for the Q3, we adjusted our valuation model and lowered FY20E/FY21E earnings per share to RMB 19.11/29.74 cents respectively. Considering the development of other brands of the company and the development of national policies, the company raised its 12-month target price to $3.68.

The main brand recorded positive growth and outperformed its peers

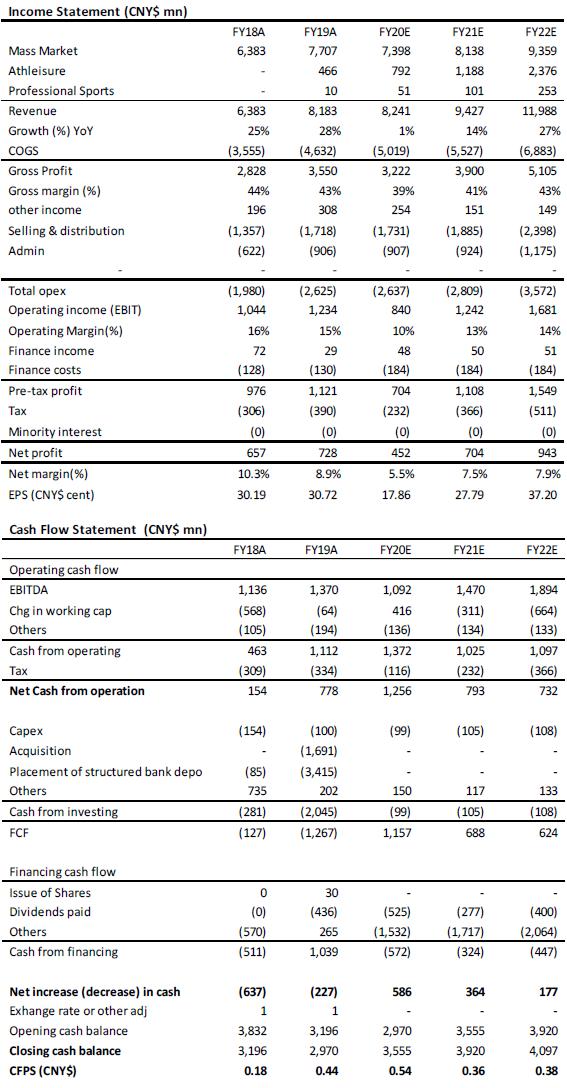

Xtep announced the Q3 operating data of the Xtep main brand on October 16. The retail sales-through growth of the main brand recorded a MSD growth compared with the same period last year, which is in line with our expectations. Sales performance continued to improve QoQ. In 1Q20/2Q20, Xtep's main brand grew by a negative 20%-25%/negative LSD compared YoY, returning to a positive growth track. The performance in the Q3 is better than its peers. In terms of monthly breakdown of the third quarter, the sales of the main brand in July and August were basically flat/LSD growth compared YoY. Sales recorded a significant improvement in September, estimated to be about LDD growth. In terms of channels, both online and offline recorded positive growth, while online sales growth is better than offline.

Inventory levels continue to improve quarterly. The retail inventory turnover period in 3Q20 is about 5 months, which is an improvement from 5 to 5.5 months in 2Q20. The current company's main goal is still to reduce inventory levels. Regarding the discount level, the retail discount level of the main brand remained flat quarterly, maintaining at a rate of 30% to 35%, which is higher than the normal level of 20% to 25%. It is expected to return to normal levels in 1Q21. In Q1 this year, the company proposed to exchange Q1 products with Q3 products to ease the inventory pressure of the retailers. It is expected that the company will cooperate with online sales promotion activities such as "Double 11" in November for promotion.

Other brands` overseas business affected

Affected by the epidemic, the company also lowered the full-year sales target of K-Swiss and Palladium from approximately RMB 900 million to approximately RMB 800 million, mainly due to the severe epidemic in Europe and the United States, and the brand's overseas business was more affected than expected. The brand is expected to postpone until next year and begin to record profits. Saucony and Merrell are expected to record 50 million in revenue for the year. The goal of opening stores throughout the year remains unchanged, 30-50 Saucony and Merrell; 30-50 Palladium.

Valuation model update

The retail sales of the company's main brand in the third quarter were in line with our expectations, but the discount level has not improved. Therefore, we lower the full-year revenue expectation of Xtep's main brand from the original expectation and adjust to minus 5% from the same period last year. In terms of GPM, the GPM of the main brand has also been reduced from the original 40% by 1 pct to 39%. The main reasons include 1) the discount level is still high and 2) the proportion of online sales of the main brand has increased, and the fixed rate of online sales is higher than offline Low 3) The proportion of children's clothing sales increased, and the GPM of children's clothing was lower.

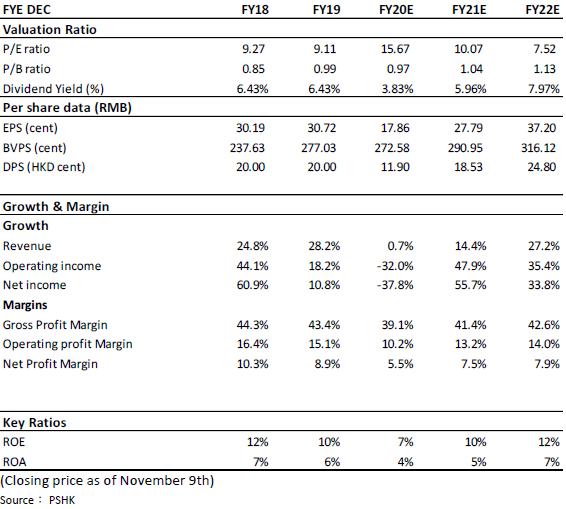

(Closing price as at 9 November)

Valuation and Investment Recommendation

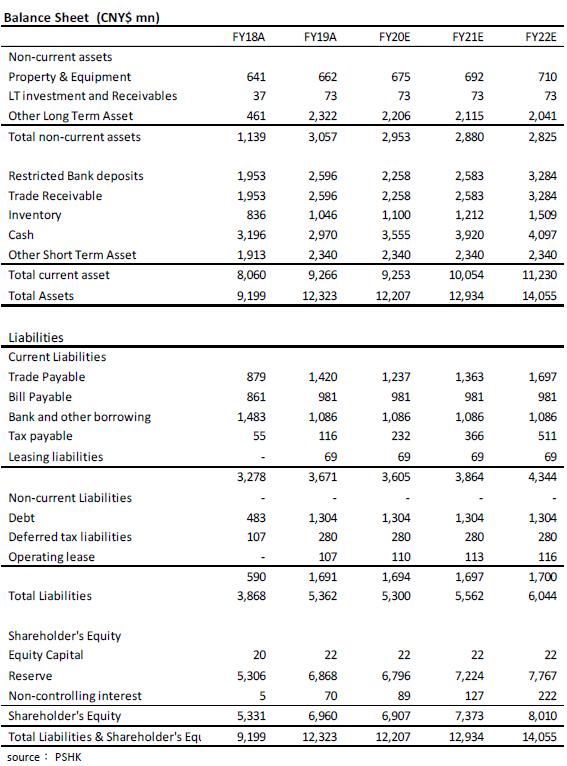

The impact of the epidemic on the company continues, but the sales and inventory levels of the main brands continue to improve quarterly, and perform better than other peers. Due to the impact of overseas business, other brands are expected to reduce revenue and record losses throughout the year. The goal of opening stores throughout the year is maintained. The four new brands have a large potential for growth in the Greater China region. In the future, the company will develop the brands in the form of direct operation, which is expected to increase the company's current GPM. Considering that the company's new brands currently have lower GPM, directly operated model can effectively increase the GPM of the new brand to 50-60%, with huge potential for future growth. It is estimated that the company's EPS for FY20E/FY21E is RMB 17.86/27.79 cents, giving the company a target price of $3.43, which corresponds to a FY20E/FY21E market earnings ratio of 17.09x/11.00x.

(Closing price as of November 9th)

Financials

Click Here for PDF format...