Investment Summary

Results Improved Significantly in Q2

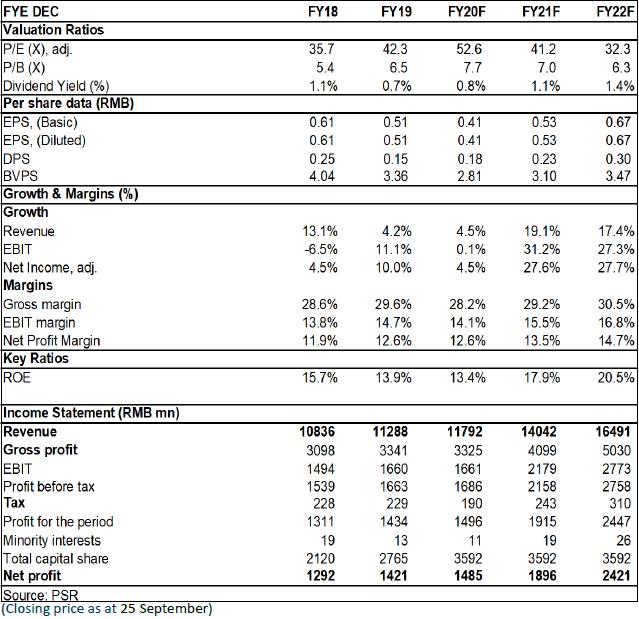

Sanhua Intelligent Controls reported revenue of RMB5.318 billion in H1, down 8.8% yoy, and the net profit attributable to the owners of the parent company was RMB643 million, down 7.14% yoy. Of this total, the revenue of Q2 was RMB2.835 billion, down 7.1% yoy, and the net profit attributable to the owners of the parent company was RMB432 million, which was basically the same yoy. It only slightly decreased by 0.5%, which was significantly smaller than the decline of18.3% in Q1. The interim dividend per share is RMB0.1, and the dividend payout rate is 55.6%.

Under the Influence of the Epidemic, the Gross Margin Decreased Slightly, and the Expense Ratio was Basically the Same

During the reporting period, the company's gross margin was 27.8%, down by 0.5 ppts yoy, mainly due to the decline in gross margin in the automotive parts and components business. The period expense ratio rose by 0.5 ppts to 14.72%. In addition, derivatives held by the company appreciated and government subsidies increased, and the final net profit margin rose by 0.24 ppts to 12.05% compared with the same period last year. In H1, the net operating cash flow was RMB1.1 billion, up 33% yoy, a dramatic improvement.

Rapid Growth of New Energy Vehicle Business

When viewed from different sectors, the revenue of the refrigeration business reached RMB4.368 billion, down 13.8% yoy, mainly due to the fact that Aweco, and Microchannel are still heavily affected by the overseas epidemic, which hold back the overall performance of the refrigeration business. The gross margin of the refrigeration business reached 27.6%, down by 0.12 ppts yoy, but still better than the industry average. Since mid-May, refrigeration business sales have increased significantly, and orders have been gradually released. After the release of the new energy efficiency standard for air conditioners, the improvement of the permeability of high energy-efficient VF air conditioners will stimulate the market demand for electronic expansion valves, which is expected to keep growing. At present, the proportion of air conditioners with electronic expansion valves around the world is about 30% with a promising market space.

The revenue of the automotive parts and components business reached RMB950 million, a sharp increase of 24.3% yoy, of which the revenue of the new energy vehicle business was about RMB540 million, a surge of 65% yoy, mainly due to the increase in the Europe subsidy for new energy vehicles in H1 and the release of new energy models by the company's customers. But at the same time, the rapid growth of new projects has led to increased investment in R&D, equipment and factories, resulting in an increase in amortization, and the increase in the proportion of purchased parts has also put pressure on gross margin. The gross margin of the automotive parts and components sector was 28.9%, down 3.6 ppts yoy. In the future, with the release of the company's key customers Tesla and Volkswagen MEB platform models, the gross margin will gradually return to 30%.

The company's customer base of new energy vehicle business has been continuously expanding, while realizing a breakthrough in Japanese customers this year, becoming the supplier of Toyota, achieving the full coverage of Germany, the United States and Japan, and further optimizing the customer structure, which also helps to consolidate company's leading position of thermal management products.

Investment Thesis

Sanhua Intelligent Controls is the leading company of refrigeration parts and components with obvious technical advantages in its products. The thermal management of new energy vehicles, dishwashers and cold-chain logistics are all promising business areas in line with the general direction of social development in the future, making the company's future performance growth more concrete. The company actively promotes integrated module projects among existing customers, which is expected to further increase its product unit price and profitability.

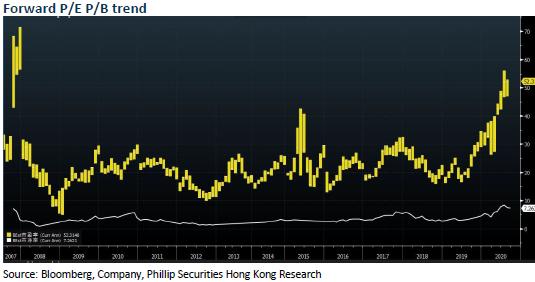

As for valuation, we expected diluted EPS of the Company to RMB0.41/0.53/0.67 of 2020/2021/2022. And we accordingly gave the target price to RMB24, respectively 58/45.5/35.6x P/E for 2020/2021/2022. "Accumulate" rating. (Closing price as at 25 September)

Risk

Progress of new production line is below expectations

Electric vehicle sales fall short of expectations

Macroeconomic downturn affects product demand

Sharply rising raw material prices or sharply falling product prices

Financials

Click Here for PDF format...