Investment Summary

The revenue is reduced 24% in H1 due to COVID-19, and sees a strong rebound in Q2

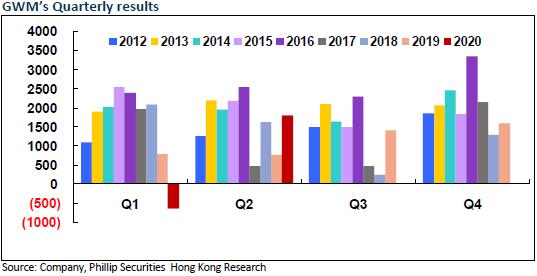

Affected by COVID-19 pandemic, GreatWall Motors reported a revenue of RMB35,929 million in H1, down by 13.17% yoy. The net profit attributable to the parent company was RMB11,46 million, down by 24.46% yoy. The net profit attributable to the parent company excluding non-recurring items was RMB802 million, down by 35.34% yoy. Despite a net loss of RMB650 million in Q1 due to the pandemic, in Q2, the Company witnessed an industry-led recovery and a turnaround, with significant rebound in its results: The net profit attributable to the parent company was RMB1,796 million, a strong surge of 141.47% yoy. The net profit attributable to the parent company excluding non-recurring items was RMB1.55 billion, a big increase of 159.58% yoy.

Sales structure is improved and profitability is outstanding

In H1, the Company sold 395,000 vehicles accumulatively, down by 20% yoy. In particular, the sales growth in Q2 turned positive, up by 17% yoy, a significant improvement from -47% in Q1, and better than the industry average. It was the main reason for the strong results in Q2. Meanwhile, the optimization of the sales structure and exchange gains led to a substantial reduction in financial expenses, which is also an important driving force.In terms of the sales structure, the Company recorded outstanding sales of Haval H9 and Great Wall P with high unit price and profit, which greatly improved the average sale price and profit of single vehicle. In Q2, the profit of single vehicle returned to a high level of RMB7,367. Underpinned by the positive scale economy of sales growth and the optimization of the sales structure, the Company's gross margin reached 17.6% in Q2, up by 4 ppts yoy and up by 8.3 ppts qoq. It drove the overall gross margin in H2 to rise 1.1 ppts to 14.72 ppts yoy.

Meanwhile, the Company's expenses were properly controlled. In Q2, the administrative expense ratio decreased by 0.19 ppts yoy. The R&D expenses were basically the same. Due to increase in transportation expenses and wages, the sales expenses rose slightly by 0.4 ppts.

The Company starts the year of products in 2021 with forward-looking innovation of three major technology brands

In H2, the Company will launch models including Haval Big Dog, the third-generation Haval H6, Tank 300, and ORA Good Cat. More new models (approximately ten models) equipped with new technologies and new power are also planned to be launched in 2021, including fuel vehicles, hybrid power vehicles and EV models. The year 2021 will be the year of products for Great Wall Motors. With the opening of the new model cycle, we expect that new platforms and new models will facilitate the Company to further enhance its competitiveness.

In July of this year, Great Wall Motors released the three major technology brands of "Lemon", "Tank" and "Coffee Intelligence", covering the whole-industry-chain value innovation and technology system of automobile R&D, design, production and automobile life. In particular, "Lemon" and "Tank" are modular vehicle platforms, covering the wheelbase ranges of 2,650-3,005mm and 2,750-3,750mm, respectively. "Tank" is more off-road. "Coffee Intelligence" is an intelligent vehicle system, covering intelligent cockpit, intelligent driving and intelligent electronic and electrical architecture.

With the constant increase of platform-based products, the Company will shorten the model development cycle and weaken the generalization of parts in the future to increase the product competitiveness. As a result, its profitability is expected to continue to increase. In 2019, the Company has achieved mass production of Level 2 models. It plans to commercialize Level 3 autonomous driving technology in 2021, and achieve autonomous driving technology that is above Level 4 in 2023. In terms of ecological integration of mobile travel services, the Company has built an ecosystem of smart travel services together with strategic partners such as Tencent, Baidu, China Telecom, China Unicom, and China Mobile, to fully launch a new strategic era of transformation to a global technology travel company.

Investment Thesis

The government fastened to remove restrictions of pickup one by one to accelerate economy recovery. Therefore, a new growth cycle of the pickup industry is expected. As a unquestionable leader, GWM launched its high-end pickup series of "Pao", which complying with the future pickup consumption trend of being high-end and industrialized. There is great potential for GWM's pickup business in the long run.

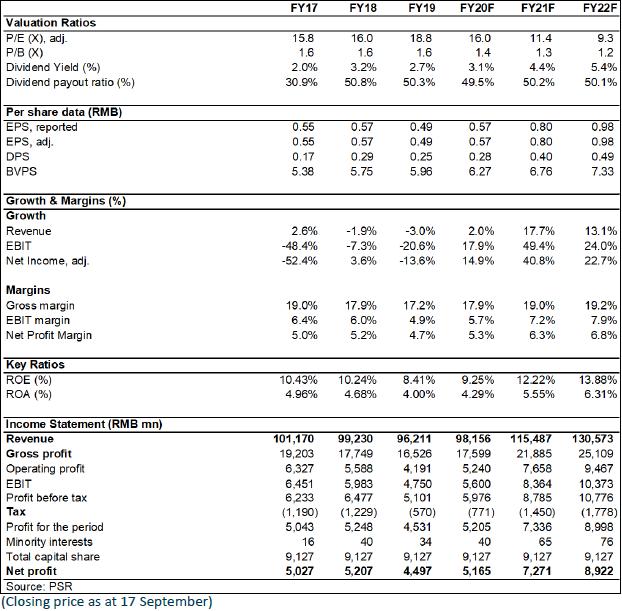

In terms of valuation, we adjust our target price to HK$11.7, equivalent to 18/13/10.5x P/E and 1.6/1.5/1.4x P/B ratio in 2020/2021/2022. We reaffirm the rating of ¡§Accumulate¡¨. (Closing price as at 17 September)

Risk

New vehicle sales fall short of expectations

The SUV market dramatically worsens

The progress of new energy vehicle/Pickup is poorer than expectations

Financials

Click Here for PDF format...