Investment Summary

Obvious drop in online ticketing subsidies

In order to compete for market shares, we have seen the market leaders in online ticketing sector, such as Maoyan and Ali Picture, spending significant amount of online ticket subsidies in recent years. Nonetheless, due to the stable market leading position of Maoyan in online movie ticketing sector, we do not think that it is necessary for Maoyan to keep spending a significant amount on subsidies in the future. In fact, the company's marketing and promotion cost (which mainly includes subsidy expenses) as a percentage of online ticketing revenue has been dropping in recent years. The decrease of online ticketing subsidy expense in 2019 was also the major reason for the company's first ever-yearly positive earnings recorded in 2019. We expect that the company can continue the decreasing trend of subsidy expense as percentage of online ticketing revenue in the future.

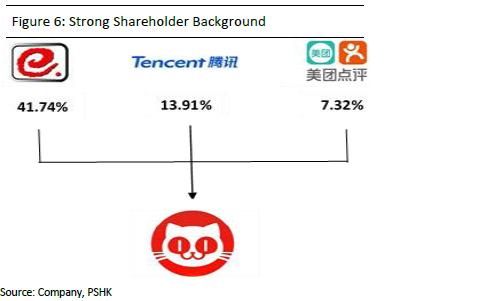

Strategic support from the strong shareholder's background

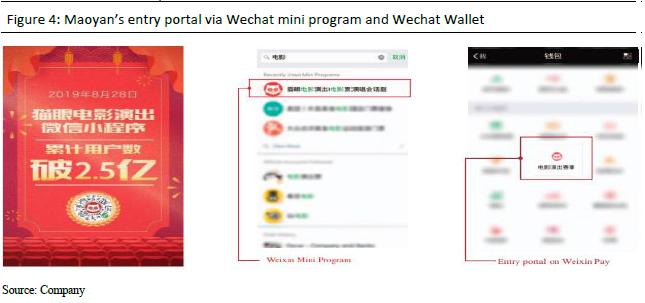

The company has received significant strategic support from its shareholders which includes Tencent, Meituan and Enlight. Their support facilitated the huge expansion and enhanced the users experience of the company. The company obtains free entry portals from Wechat and Meituan App, which allow the company to benefit from the huge user traffic of Tencent and Meituan. In August 2019, the number of users of Maoyan's Wechat mini program has reached 250 million, which is nearly 30% of the total internet users in China. In July 2019, the company has launched the ¡§TenMao¡¨ Alliance along with Tencent. Maoyan and Tencent will take advantage of their rich resources, extensive data and advanced products across various entertainment sectors to deepen the cooperation and create a superior entertainment experience for Chinese consumers.

Ongoing Upstream Ventures

Maoyan has received intensive B-end and C-end data from the cinemas and its users. The Maoyan Research Institute, which is a leading analysis platform in the entertainment industry, was set up specifically to apply big data analysis on these data (both B-end and C-end data) and make analyses on user's preference and needs. The analysis can be used to facilitate decision making process in promotion and distribution for movies and come up with a more effective and cost efficient marketing and distribution strategy for each movies. By leveraging on its strong big data capabilities, Maoyan has expanded its business quickly along the value chain and has already become the largest lead distributor for domestic movies in 2018. We believe the movie distribution business will be one of the key driver for the company's future. Besides movie promotion and distribution, Maoyan is also aggressively extending into upstream production investment, which we believe is another potential driver for the company in the future. In march 2019, Maoyan has invested into Huanxi Media Group Limited, which is a renowned film company, and has established a strategic partnership with it. This investment allows Maoyan to make production investment on Huanxi Media's top quality movies and TV dramas in priority to others movie producers.

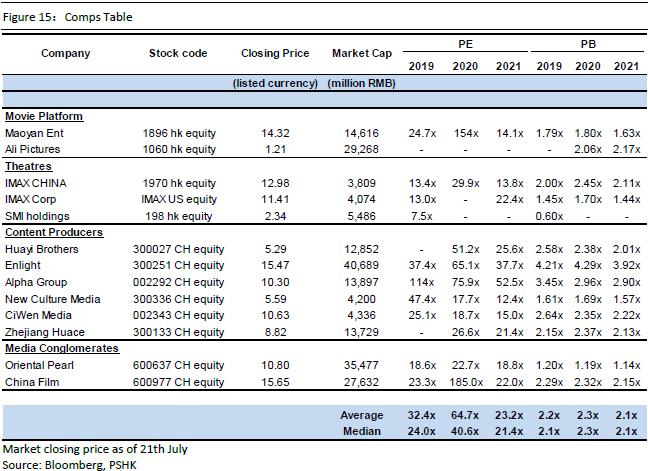

Valuation

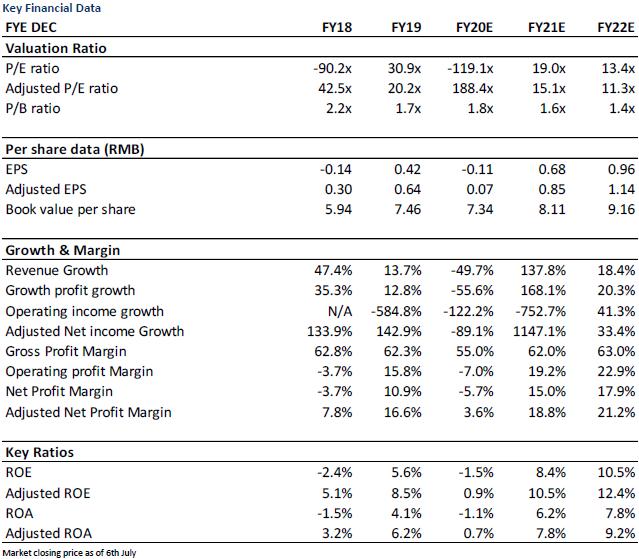

We believe the company's 2020 performance will be hugely affected by the COVID-19 outbreak, in line with the announcement of the company on 22nd May. But it is unlikely to affect the company's long term growth. We forecast the company's adjusted EPS are RMB 0.07/0.85/1.14 in 2020/2021/2022. We have set a target price of 16.6HKD, which implies a PE ratio of 17.5x/13.1x on the company's 2021/2022 adjusted EPS. We initiate with an ¡§Accumulate¡¨ rating. (Market closing price as of 21th July) (exchange rate: RMB 0.9/HKD)

Risk

1) The COVID-19 last longer than expected 2) The box office of movies in China recovered slower than expected 3) Upward Ventures of the company is less effective than expected

Industry Review and Forecast

The China's movie market is expected to continue its growth in future

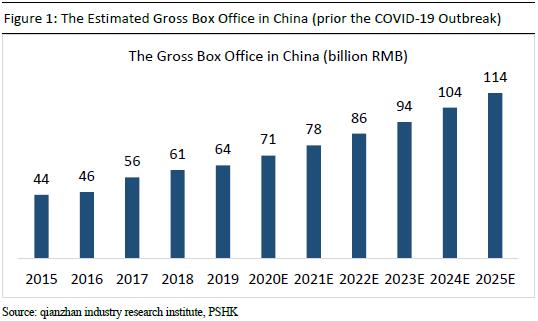

The china's movie market is already the second largest in the world, just behind the US's market. According to QianZhan industry research institute, the gross box office in China has rose from RMB 55.9 billion in 2017 to RMB 64.3 billion in 2019, with a CAGR of 7.3%. The gross box office in China is expected to grow to 114 billion RMB in 2025, with a CAGR of 10.1% from 2019 to 2025. These estimates were made prior the COVID-19 outbreak.

The growth in the Chinese movie markets was mainly attributed by the following factors.

1) The availability of a greater number of high quality domestic movies has propelled the growth of China's movie industry. According to the China Film Administration, the number of domestic movies released increased from 229 in 2012 to 422 in 2019, as movie genres become more diversified and with higher quality. The percentage of gross box office contributed by domestic movies has increased from 49% in 2012 to 64% in 2019.

2) China is witnessing a rapid development of its movie infrastructure. According to IResearch, although China already has the highest number of movie screens in the world, the nation's number of screens and movie admission per capita are still at a much lower level compared with those of the United States. This indicates a huge growth opportunity.

3) China's movie market currently still relies hugely on ticket sales with gross box office in China accounting for 73.5% of the total market size in 2017. As China's movie market continues to develop, more revenue streams have become available, ie, movie merchandise products and in-cinema food and beverages.

The online movie ticketing market

According to IResearch, the online penetration rate of movie ticketing in China has increased from 18.4% in 2012 to 85.5% in the nine months ended September 30, 2018. It is expected that the online penetration rate will remain stable in the future. The online movie ticketing industry used to be more fragmented. With the intensive use of user incentives and trend of mergers and combinations, the market is relatively concentrated now. According to IResearch, the largest and the second largest market participant in the sector have a total of 90%+ market share in terms of total GMV of the ticketing business in 2019.

The online entertainment event ticketing market

The current online penetration rate of entertainment event ticketing in China is at a relatively low level. According to IResearch, this penetration rate will rise to 78.9% in 2022. Further, the sector is relatively fragmented. In recent years, established online movie ticketing service providers have entered the online entertainment event ticketing market by leveraging on their user base to cross-sell entertainment event tickets. The entertainment event market is still nascent with considerable growing potential, the leading online movie ticketing service providers can benefit hugely by leveraging and capitalizing on the scale of their online movie ticketing services user base and their experience in online marketing and promotion.

Entertainment content services

China's entertainment industry is fragmented with a large number of participants along the value chain from content production/investment to promotion and distribution and across entertainment content formats, such as movies, TV series, web series, web movies, variety shows as well as entertainment events. Internet-empowered entertainment content service platforms have emerged to connect consumers with vertical players such as production companies and distributors and empower different industry participants to optimize operating results, leveraging their large user base, data analytics capabilities and industry resources. The traditional market participants and the Internet-empowered entertainment content service platforms both have their own advantages. Internet-empowered entertainment platforms possess the user base and insights required to compete with traditional market participants, while traditional market participants have more established industry knowledge and operational expertise in the sector. Platforms with a large user base and extensive industry resources are likely to better understand the audience's preferences and industry needs, allowing them to conduct their businesses more effectively and efficiently.

COVID-19 impact

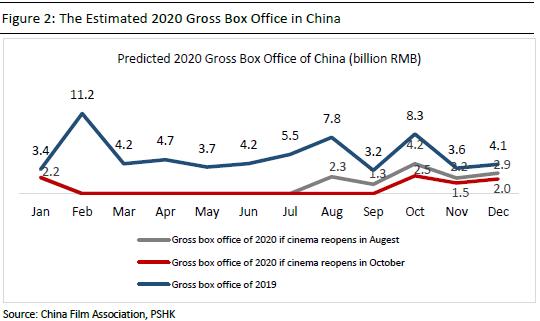

Cinemas in Mainland China have been closed for half a year. The entire movie industry has been stalled, from production and distribution to screening. On 20th July, the cinemas located in ¡§low risk¡¨ area in China have finally begun reopening. According to the China Film Association, the Gross box office of China in 2020 Q1 was RMB 2.24 billion down by 88% yoy. The gross box ticket of China in 2020 is expected to be RMB 12.8 billion /RMB 6.0 billion if the all cinemas in China resume operation in August/October, according to China Film Association. Ever since the outbreak, the Chinese Government has issued multiple policies with the aim to help ease the impact on the movie industry in China (including subsidies, tax relief, lending out loans etc.) According to the China Film Association, 58% of the Cinemas found these policies helpful.

Company Overview and its Competitive Advantages

A leading Internet empowered entertainment platform

Maoyan's revenue stream is separated into 3 main parts.

1) Online Entertainment ticketing services

The company provides online entertainment ticketing services which includes movie ticketing and entertainment event ticketing (concerts and sport events etc). The company is already the obvious leader in the movie ticketing sector with more than 60% of the market shares in terms of the GMV of online ticketing services. Maoyan is cooperating with 95%+ of cinemas in China covering more than 600 cities. In terms of Entertainment event ticketing business, Maoyan is currently the second largest in providing entertainment event ticketing services in terms of market share. Maoyan is charging a commission fee ranging from 4%-8%/3%-30% for each movie /entertainment event ticket sold through its platform.

2) Entertainment Content Services

By leveraging the company's big data capabilities, the company is able to develop profound insights on the user and industry to help its business partner to create suitable promotional strategies their movies. Besides that, the company has also carried out vertical integration and starting to participate in movie projects as distributor and/or producers. In terms of the distribution business, Maoyan has leveraged its big data analysis and has established itself a brand name in the movie distribution sector by becoming the largest lead distributor of domestic movies in 2018. The fee received as lead distributor/ co distributors typically ranges from 5% to 12%/ 1% to 2% respectively. In terms of Movie Production business, the company is aggressively extending its business into upstream production investments in recent year.

3) Advertising and e- commerce businesses

Maoyan provides advertising services to advertisers by placing media content on its mobile platforms. In addition, the company provide entertainment e ¡V commerce services such as preordering in-venue food and beverages, IP-derivatives merchandise and movie ticker members.

A more diversified revenue mix

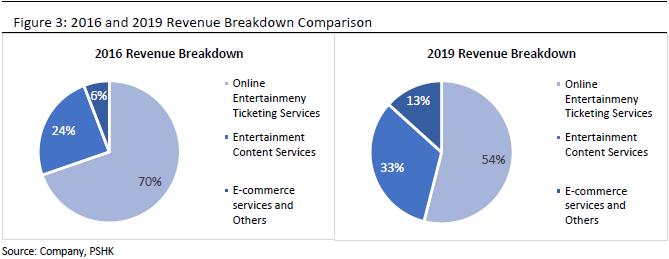

The company has become less reliant on its online ticketing business as the revenue contribution from online ticketing business as a % of total revenue has gradually decreased. This % was 54% in 2019 and it was down by a lot comparing to the 70%, 59% and 61% in 2016,2017 and 2018 respectively. Since the online penetration of ticketing services as well as the market share of the company in movie online ticketing services are already at a very high level. In addition, the growth of the gross box office in China is expected to be slow in the future (CAGR of 10% from 2019 to 2025 according to QianZhan industry research institute). Therefore, the company will not be able to sustain its high growth in the future if it is only relying on its online ticketing business. We believe the entertainment content business of the company will be the main growth driver for the company in the future. The company's revenue from entertainment content services has increased by 31% yoy in 2019.

Obvious drop in online ticketing subsidies

The online ticketing segment used to be more fragmented, with many small to medium sized online ticketing service providers in the segments. In order to compete for market shares, we have seen the market leaders in online movie ticketing sector, such as Maoyan and Ali Picture, spending significant amount of online ticket subsidies. The ¡§subsidies for market share¡¨ strategy is no longer appeared strange to us as we have seen this strategy been used in multiple segments such as the e-commerce and food delivery platform, in recent years. Nonetheless, the market is now relatively concentrated with Maoyan and Ali picture owning 90%+ of the market share in terms of GMV of online ticketing and the online penetration is relatively high at 85%+, we do not think that it is necessary for the Maoyan to keep spending a significant amount on subsidies in the future. In fact, the amount of marketing and promotion cost (which mainly includes subsidy expenses) as a percentage of online ticketing revenue have been dropping in recent years. The market and promotion cost as a percentage of online ticketing revenue were 86%, 76% and 56% in 2017, 2018 and 2019 respectively. The decrease of subsidies in 2019 was also the major reason for the company's first ever-yearly positive earnings recorded in 2019. We expect that the company can continue the decreasing trend of subsidies as percentage of total online ticketing revenue in the future.

Strategic support from the strong shareholder's background

The company has received significant strategic support from its shareholders which includes Tencent, Meituan and Enlight. Their support facilitated the huge expansion and enhanced the users experience of the company.

1) Tencent:

Maoyan and Tencent have formed a strategic partnership in 2017 and Tencent has set up a free entry portal to Maoyan's platform on Wechat App and QQ App. This partnership makes Maoyan the only entertainment platform embedded in Weixin and QQ App. This allows Maoyan to benefit from the huge user base of Tencent. In August 2019, the number of users of Maoyan's Wechat mini program has reached 250 million, which is nearly 30% of the total internet users in China, according to 44th Statistical Report on the Internet Development in China by China Internet Network Information Center. Besides that, the company also cooperates with Tencent Pictures, Penguin Pictures, Tencent Video and other Tencent platforms and enjoys certain preferred rights in online movie and entertainment ticketing services as well as the distribution, promotion and production of movies and other entertainment content. In July 2019, the company has launched the ¡§TenMao¡¨ Alliance along with Tencent. Maoyan and Tencent will take advantage of their rich resources, extensive data and advanced products across various entertainment sectors to deepen the cooperation and create a superior entertainment experience for Chinese consumers.

2)Meituan

Maoyan is the exclusive business partner in entertainment ticketing and services on Meituan app and Dianping app. The strategic partnership also allows Maoyan to set up a free entry portal on these Apps. The strategic partnership is up until September 2022.

3) Enlight

Enlight has sufficient resources and expertise in the TV and movie production industry in China. Maoyan and Enlight Media has signed a strategic agreement in 2018 which includes cooperation in various aspects including movie productions and distribution cooperation.

Clear online ticketing business model, with relatively strong liquidity

The business model of Maoyan's online ticketing business can be decomposed into 3 steps.

1) By leveraging the huge user traffic of Maoyan's platform itself and the platform of its strategic partners, Maoyan can deliver the details of newly released movies to the users effectively. Users can also write movie reviews on Maoyan's platform and share it on his/her wechat moments, which further enlarges the company's reach on users.

2) After delivering details of movies to the users, users can purchase movie tickets on Maoyan's system via the entry portal of Wechat /Meituan App or Maoyan's platform itself. By setting up a SaaS system on every cinemas partnering up Maoyan, Maoyan can receive information from each cinemas (including timetables of movies and available seats for each screening). Thus, the platform can provide real time cinema seat selection to the users.

3) Maoyan is acting as an agent between end consumers and cinemas. It will charge for a commission rate ranging from 4-8%.

Ongoing Upstream Ventures

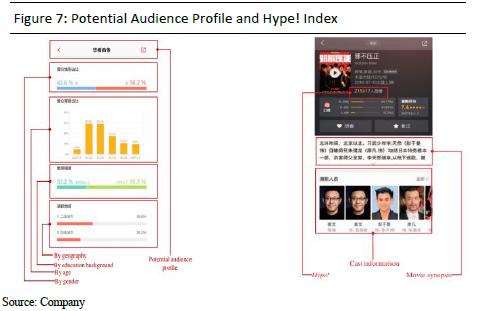

While providing SaaS solution to the cinemas, Maoyan is also receiving intensive B-end (business end) data (including operation data and real-time box office statistics) from these cinemas at the same time. In addition, Maoyan has already accumulated a gigantic C-end (customer end) database from its huge user traffic (including the part contributed by Tencent and Meituan). The Maoyan Research Institute, which is a leading analysis platform in the entertainment industry, was set up specifically to apply big data analysis on these data (both B-end and C-end data) and make analyses on user's preference and needs. The analysis can be used to facilitate decision making process in promotion and distribution for movies as well as coming up with a more effective and cost efficient marketing and distribution strategy for each movies.

One of the most exciting features of Maoyan's big data analysis is that it can come up with a Potential Audience Profile, which shows the age, gender, education background etc of each movie's potential audience. Maoyan and its business partner can then use this information to adjust their marketing and distribution strategies and focus on the appropriate channels with the optimal timing to reach viewers who are most likely to react favorably. Further, Maoyan can also generate a ¡§Hype! index¡¨ for each movie, which is a statistic that indicates the user anticipation level for a movie prior its release. This index is extremely helpful for Maoyan and its business partners to determine the optimal pricing strategies for each movie in order to maximize their operational results.

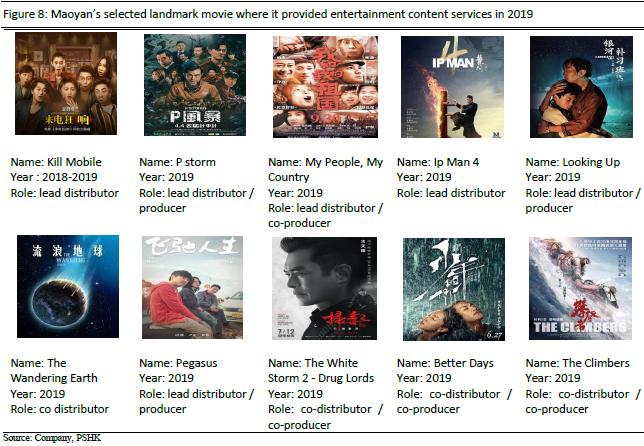

By leveraging on its strong big data capabilities, Maoyan has expanded its business quickly along the value chain and has already become the largest lead distributor for domestic movies in terms of China gross box office just only 2 years after its first involvement as lead distributor for movies. In 2019, the company has acted as the lead distributor for 14 movies with a total gross box office of 7.4 billion RMB. We believe the movie distribution business will be one of the key driver for the company's future.

Besides movie promotion and distribution, Maoyan is also aggressively extending into upstream production investment, which we believe is another potential driver for the company in the future. In march 2019, Maoyan has invested into Huanxi Media Group Limited, which is a renowned film company, and has established a strategic partnership with it. This investment allows Maoyan to make production investment on Huanxi Media's top quality movies and TV dramas in priority to others movie producers. Despite that the earnings from production and investments of movies / TV dramas are volatile by nature. However, Maoyan can provide valuable market-oriented advices on productions (ie cast selections, shooting and editing styles) and distributions to the lead producer by leveraging on its big data capabilities. This can greatly improve the return on investments of Movie / TV dramas.

The COVID ¡V 19 impact

Despite the huge impact of COVID-19, we believe that since the company has sufficient cash on hand and has a relatively high ability to resist risk. We expect that the epidemic will only affect the company's short term performance and will not affect the company's long term growth. The company operating performance should resume normal before 2021. In addition, we believe that many small to mid-sized movie distributors and producers may face bankruptcy during the COVID-19 period. Thus, we expect Maoyan, the largest lead distributor for domestic movies in China, can potentially increase its market share after the outbreak by further consolidate the movie production and distribution sector in China.

Financial Analysis and Forecast

Operating indicator

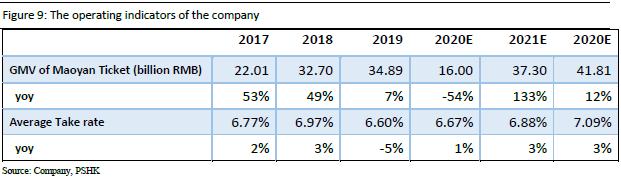

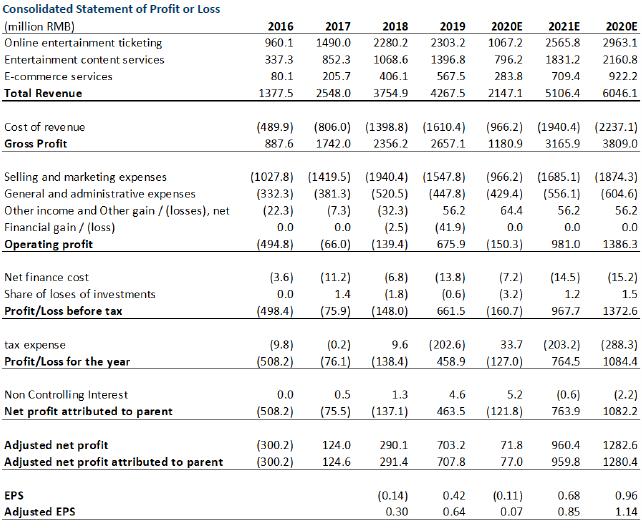

We believe that the Covid-19 outbreak has a huge negative impact on the company's total ticketing GMV in 2020. Cinemas in Mainland China have been closed for half a year and have only started reopening on 20th July. Besides that, many live events (including concerts) are held via the internet during the year. Thus, we believe the total ticketing GMV of the company will drop hugely in 2020, and after that, it will normalize to the pre Covid-19's relatively high level in 2021 and 2022. We forecast that the total ticketing GMV of 2020/2021/2022 are RMB 16.0/37.3/41.8 billion respectively, up by -54%/201%/12% yoy.

On the other hand, the company's leading position in online movie ticketing sector is relatively solid. We also expect that the market share of the company's online entertainment event ticketing sector will rise in the future. Hence, the company's bargaining power is likely to increase and we expect the company's average take rate from its ticketing business will therefore have a steady rise each year for the following years. We forecast the average online ticketing take rate of the company are 6.67%/6.88%/7.09% in 2020/2021/2022 respectively, up by 1%/3%/3% yoy.

Revenue

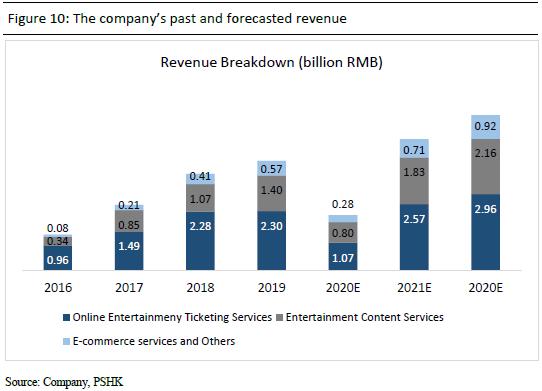

The company's revenue has increased from RMB 1.38 billion in 2016 to RMB 4.27 billion is 2019, with a CAGR of 45% from 2016-2019. We forecast the company's revenue of 2020/2021/2022 are RMB 2.15/5.11/6.05 billion, with a CAGR of 12% from 2019-2022. As affected by the COVID-19, we expect that the company's revenue of 2020 will down by 50% yoy. Among all revenue sources of the company, we believe that the epidemic will have the greatest impact on the company's revenue of online ticketing in 2020 and we forecast that it will drop to RMB 1.07 billion, down by 54% yoy. In addition, the company's revenue generated from entertainment content services/ advertising services and e-commerce services are forecasted to be RMB 0.80/0.28 billion, also down by 43%/50% yoy.

We believe that the Chinese movie industry will gradually recover in 2020 H2. Hence, we expect the company's revenue will be able to resume to the high level prior the epidemic in 2021 and 2022. The revenue contributed by online ticketing business is forecasted to be RMB 2.57 billion in 2021, up by 11% /140% comparing to the figure in 2019/2020. This figure is expected to rise by 15% in 2022 and reach RMB 2.96 billion. This growth will be mainly driven by the increase in live entertainment ticketing online penetration rate and the growing market share of the company in this sector. On the other hand, we forecast that the company's revenue in entertainment content services in 2021/2022 are RMB 1.83/2.16 billion, up by 130%/18%. The main driving force behind this growth will be the company's big data analysis and its continuing upward ventures. Regarding to the advertising and e-commerce business, we expect there will be a huge growth in 2021 onwards. Nonetheless it will still remain relatively insignificant comparing to the total revenue. We forecast it will rise to RMB 0.71/0.92 billion in 2021/2022, up by 150%/30% yoy.

Gross Profit and Gross Margin

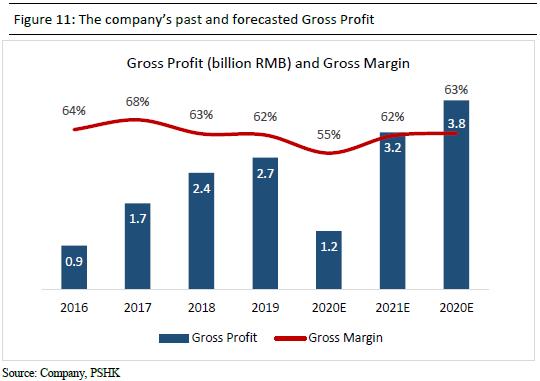

The company's gross margin is relatively stable for the past few years (floating between 62%-68%). However, as a result of the Covid-19 epidemic, we believe the average movie ticket price will drop in 2020H2 (after the re-operation of cinemas) in order to attract more audiences. This will have a negative impact on the gross margin of the company in 2020. We forecast it will drop to 55%. Nonetheless, as the movie industry gradually recover, as well as the increase of revenue contribution by the relatively higher gross margin businesses (including, movie distribution, e-commerce and advertising) of the company, we expect the gross margin of the company will rise in 2021 and 2022 and reach 62% and 63% respectively. We forecast that the gross profit of the company are RMB 1.2/3.2/3.8 billion respectively in 2020/2021/2022, up by -56%/168%/20% yoy.

Operating Profit and Operating Margin

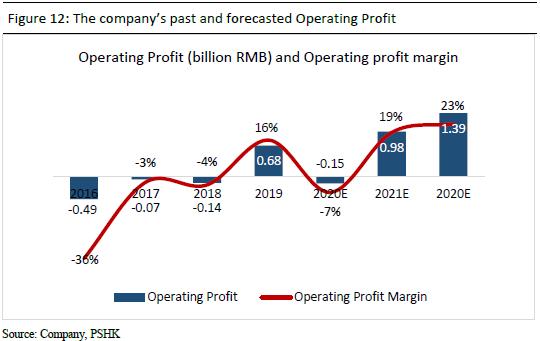

The company's selling and distribution expense as % of revenue has an obvious decreasing trend for the past few years as the ticketing subsidy expense as % of revenue decreases. We believe the company can continue this decreasing trend in the future since the company's leading position is solid. Nonetheless, since we expect the company revenue will drop significantly in 2020, hence, this expense ratio is expected to rise in 2020. We expect the selling and distribution expenses as % of revenue are 45%/33%/31% in 2020/2021/2022. On the other hand, since the company's administrative expense is relatively fixed, therefore the administrative expense as % of revenue in 2020 will be high at 20%. After the epidemic, it will normalize to 11%/10% in 2021/2022. We forecast the company's operating profit in 2020/2021/2022 are RMB -0.15/0.98/1.39 billion, with the corresponding operating margin at -7%/19%/23%.

Adjusted Net Profit Attributed to Parent and Adjusted EPS

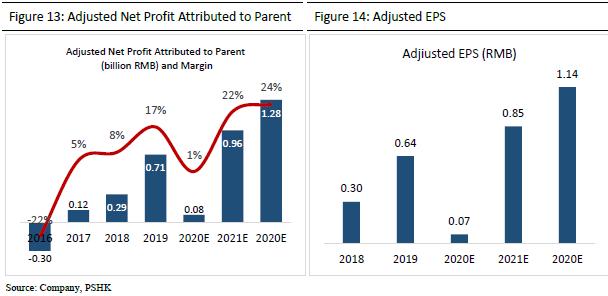

We believe that comparing with Net profit attributed to parents, adjusted net profit attributed to parent can better reflect the company's result and performance. This is because the Net profit attributed to parents is after the deduction of the equity-settled share-based expense and amortization of intangible assets resulting from business combinations, which are one-off non-operating expenses. We forecast the adjusted net profit attributed to parent are RMB 0.08/0.96/1.28 billion, with corresponding adjusted EPS at RMB 0.07/0.85/1.14.

Valuation

We have set a target price of 16.6HKD

We believe the company's 2020 performance will be hugely affected by the COVID-19 outbreak, in line with the announcement of the company on 22nd May. But it is unlikely to affect the company's long term growth. We forecast the company's adjusted EPS are RMB 0.07/0.85/1.14 in 2020/2021/2022. We have set a target price of 16.6HKD, which implies a PE ratio of 17.5x/13.1x on the company's 2021/2022 adjusted EPS. We initiate with an ¡§Accumulate¡¨ rating. (Market closing price as of 21th July) (exchange rate: RMB 0.9/HKD)

Financials

Click Here for PDF format...