Investment Summary

Excellent Pickup Performance Drives the Sales Volume in June to Surge by 30% YoY

GWM released the latest sales data, with wholesale sales of 82,036 units in June, increasing 29.6% yoy following the approximately 30% surge in May, led the industry against the market trend, and remained the same mom. The sales volume of the four major brands (HAVEL, WEY, GWM Pickup and ORA) were 46,998, 5,653, 26,750, and 2,635, respectively, which increased 1,742 or 3.85%, decreased 1,102 or 16%, increased 19,224 or 255% and decreased 1,127 or 30%, respectively.

The main features of the sales in June are as follows, according to our analysis:

1) The demand of Wingle pickup and high-end pickup of "Pao" was constantly strong, with the monthly sales volume being 11,677 and 15,003 units, respectively, which contributed more than 90% of the increase by increasing 19,514 units yoy.

2) The China VI vehicle emission standards were adopted and the stock was reduced in the same period last year, which lowered the base of some models (M6/H9) last year, explaining around 40% of the increase.

3) The medium-to-high-end SUV (H6/F7/WEY series) was a little weak maybe due to elements including the approach to the end of the product cycle and the shift of production capability, which offset some benefits.

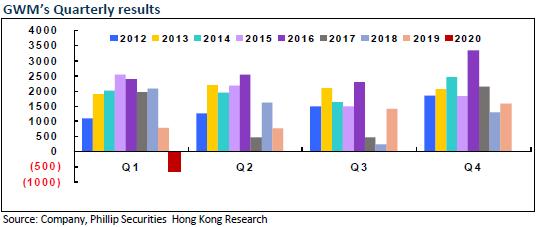

In 2020H1, the Company sold 395,000 units accumulatively, down 20% yoy. Specifically, the growth ratio of Q2 sales volume yoy turned positive, which was up 19%, compared with the -47% in Q1. It was also better than the average of the industry. Export was an exception. It fell by 32% yoy to 20,536 units owing to severe overseas pandemic.

Great Potential of Pickup Business

GWM sold pickups upon its foundation and had rich experience in the domestic pickup sector for decades. Enjoying a market share of approximately 50%, the sum of the 2nd to 7th in the industry, it was absolutely the king of pickup. Previously, pickups are classified as trucks in China and was restricted in terms of passage in cities and lifespan, which negatively affected the development of the pickup industry. The filtration rate of pickups in China was only 1.6%. Yunnan, Hebei, Henan, Liaoning, Hubei and Xinjiang lifted their city entry restriction on pickups one after another since 2016. In 2019, the Ministry of Transport cancelled the two certificates for pickups and promoted the "Three-in-one inspection". This year, Chongqing, Shaanxi, Jilin, Jiangxi, Jiangsu, Ningbo in Zhejiang, Hangzhou and Shanghai also lifted their restrictions one by one to accelerate economy recovery. Therefore, a new growth cycle of the pickup industry is expected. The specification of the high-end pickup series of "Pao" under GWM complied with the future pickup consumption trend of being high-end and industrialized. The series has great potential in the long run.

Increasing Investment to New Platforms and R&D Put Pressure on Short-Term profits

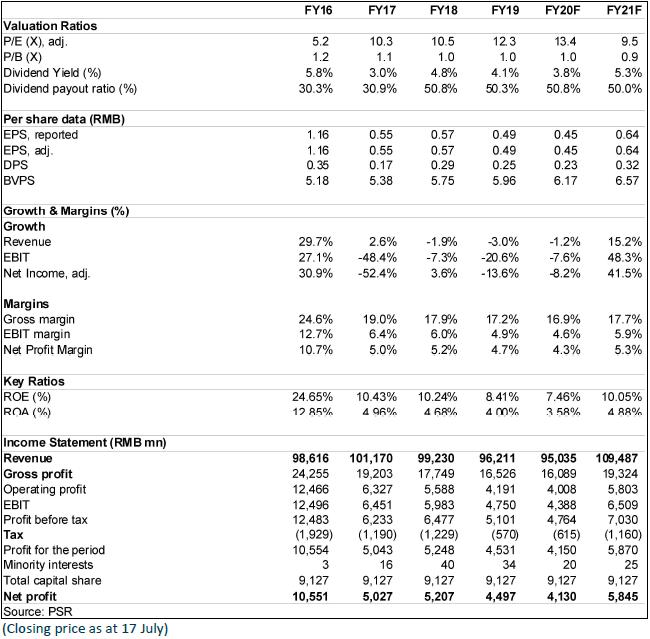

In the recent three years, the Company increased R&D investment and strengthened brand marketing. Given the worsening competition pressure, it proactively adjusted its strategies, enhanced the building of models and brand power of the four major brands of HAVAL, WEY, GWM Pickup and ORA, and expanded the interval of product prices. The enlarged market shares, corporate governance, organizational structure and rewarding mechanism of GWM have been improved, which laid a solid foundation for the future operations efficiency, though the growth rate of income and profits has been affected since 2017. In 2019, the net profits of GWM dropped by 13.6% yoy to RMB4.5 billion. The net loss was RMB650 million due to the impact of the pandemic in Q1 2020.

The Brand New Platform to Initiate New Product Cycle in H2

In Q3 2020, the Company will launch HAVAL Big Dog, a new model based on its brand new module platform and a new H6, which will compensate the weakness of the company's products in terms of lightweight, module and expansion, and provide more diversified engine power specification. With the constant increase of platform-based products, the Company will shorten the model development cycle and weaken the generalization of parts in the future to increase the product competitiveness. As a result, its profitability is expected to increase. With regard to new energy vehicles, ORA will also launch R2, a brand new electric vehicle, and the first fuel cell and hydrogen vehicle is expected to be launched officially in 2022. In addition, the Spotlight Automotive, a joint venture with BMW, is expected to commission in 2022. The brand will be producing MINI fuel-fired cars for export and engaging in research and development of pure electric cars, which also has the potential to manufacture new energy models.

Investment Thesis

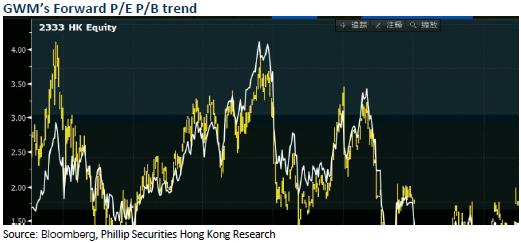

In terms of valuation, we adjust our target price to HK$7.6, equivalent to 15.1/10.7x P/E and 1.1/1.0x P/B ratio in 2020/2021. We give the rating of ¡§Accumulate¡¨. (Closing price as at 20 July)

Risk

New vehicle sales fall short of expectations

The SUV market dramatically worsens

The progress of new energy vehicle/Pickup is poorer than expectations

Financials

Click Here for PDF format...