Investment Summary

Company profile¡GGlobal Leader of Refrigeration Components

Zhejiang Sanhua Intelligent (Sanhua) is leading HVAC&R OEM manufacturer of controls and components. The company's products mainly include:

1) 4-way reversing valves, electronic expansion valves, solenoid valves, micro-channel heat exchangers and Omega pumps that are mainly applied in fields such as air-conditioning, refrigerator, cold chain logistic and dish-washing machine.

2) Thermostatic expansion valves, receivers, electronic expansion valves and electronic pumps that are mainly applied in thermal management of passenger vehicles such as traditional fuel-fired vehicles, hybrid electric vehicles and electric vehicles.

Sanhua was founded in 1994 and was listed on the Shenzhen Stock Exchange in 2005. The founder Zhang Daocai and his two sons, Zhang Yabo and Zhang Shaobo, are actual controllers of the Company, hold approximate 60% of the Company's shares, with relatively concentrated shares and stable shareholding structure. In 2012, the Company entered the market of white goods components such as dish-washing machines, coffee makers and washing machines through the acquisition of German Aweco. In 2015 and 2017, the Company joined the micro-channel business and vehicle component business of the large shareholder through private placement. Since then, the Company has developed domestic and overseas markets (divided by region) and two sectors(divided by industry) of household appliance components and thermal management of vehicles; The revenue of four business units (divided by production)including refrigeration, micro channels, vehicle components and Aweco respectively covered a proportion of 55%, 11%, 13% and 10% (data in 2018)

The development of over 30 years has made Sanhua lead the global market of HVAC&R controls and components. The products of the Company such as electronic expansion valves, 4-way reversing valves, solenoid valves, micro-channel heat exchangers and Omega pumps have the highest occupancy rate across the world. The market proportion of service valves, thermostatic expansion valves for vehicles and receivers rank top among the world. The global occupancy rate of electronic expansion valves, 4-way reversing valves, micro-channel heat exchangers and service valves is 39%, 49%, 30% and 35%, respectively. At the same time, the Company focuses on the R&D of air-conditioners of new energy vehicles and products of thermal management and becomes the first Chinese company to receive the PACEAWARD of Automotive News of America.

Overseas merger and acquisition and high-quality asset of large shareholders constantly improve the overall product strength of the Company. Since the listing, the Company's result has maintained steady, rapid growth. Its revenue increased from RMB133 million in 2002 to RMB10.84 billion in 2018 with the annual compound growth rate of 31.6%. The net profit rate increased from RMB16 million to RMB1.29 billion, with the compound growth rate of 31.3%. The Company's profitability is relatively strong with the current gross profit margin of approximate 30%, net profit margin of 12%, ROE of 15% to 16% and asset-liability ratio of 37% only. The HVAC&R unit contributes most to gross profit and Aweco contributes the least due to relatively high production cost in Europe.

Globalization Layout with Increasing Overseas Proportion

Headquarters of the Company is located in Shaoxing, Zhejiang. But Sanhua emphasizes the expansion in global map and establishes overseas factories in America, Mexico, Poland and Thailand to cover the overseas market. The Company has established stable partnerships with world-leaders refrigeration manufacturers such as Panasonic, Daikin, Mitsubishi, Toshiba, Hitachi, Fujitsu, LG, Samsung, Carrier, Trane, York, Gree, Midea, and Haier and has become the supplier of giants of international vehicle and components such as Valeo, Mahle, Volkswagen, Mercedes-Benz, BMW, Volvo, Tesla and GM.

The product competitiveness incurred from continuous research and development and the expanding customer base lay a preferable foundation for the revenue growth of the Company. What's more, thanks to the overseas production bases and network, oversea orders keep rising and the yoy growth rate of revenue in recent years has increased over 20% with the generally growing proportion of over 50% of overall revenue.

Consolidated Position as Refrigeration Leader

The Company owns leading technology, market share and consolidated leading position in refrigeration business. At present, the average ownership of air conditions is 1.4 air conditioners per household in China's urban areas and approximately 0.6 in rural areas. Compared with Japan, whose average ownership of air conditioners was 2.9, there is still a lot to improve in China's average ownership of air conditioners. Moreover, the increasing penetration rate of variable frequency air conditioners and central air conditioners will promote the demand for products of the Company. The recovery of China's real estate cycle may drive consolidated growth in the Company's refrigeration business from mid- and short-term perspectives.

Thermal management of new energy may turn into the new result growth engine

Sanhua is one of the domestic companies implementing thermal management of new energy early. Its products have entered the supply chain of new energy vehicle platform of the tier-1 vehicle factories in Europe and the United States such as Volkswagen, Daimler, BMW, GM, Audi, Volvo, PSA, Jaguar and Land Rover. Its domestic customers include vehicle factories such as Geely, BYD, SAIC and Weilai. At present, The Company has over tens of billions of orders on hand. The Company is the supplier of Tesla's Model3, providing electronic expansion valves, electronic oil pumps, oil coolers, water-cooling plates and battery cooling fluid and supplying approximately RMB1300 for each vehicle. Many overseas new energy manufacturers will successively begin production from mid- and short-term perspectives. In the future, the revenue of the Company's thermal management of new energy may exceed the one in refrigeration, turning into a new result growth engine.

Profound potential in the business of dish-washing machine components of Aweco, the subsidiary.

Aweco, with a history of 50 years, is the honoured component manufacturer in Europe and has been reckoned as the tier-1 supplier of the core parts of dish-washing machines by household appliance customers for a long time. The proportion of dish-washing machine business is more than 80% and the Company's customers include famous brands such as BSH, Whirlpool, Philips and Electrolux. The penetration rate of dish-washing machines in China is less than 2%, which is far behind the 80% of Europe, 50% of the United States and 8% of East Asia. With the transformation in consumption concepts and the beginning of the aging society, the domestic industry of dish-washing machines hold profound potentials that will directly benefit Aweco. After the acquisition, the Company moved the factories in German to Poland and the factories in Shanghai to Wuhu step by step. With the improved production capacity and decreasing production cost, the profitability of Aweco will be generally strengthened.

Investment Thesis

Sanhua is the leading manufacturer of refrigeration components and owns significant advantages. Thermal management of new energy vehicles, dish-washing machines and cold chain logistics are broad markets meeting future social development. The certainty of growth in the Company's future result is relatively high.

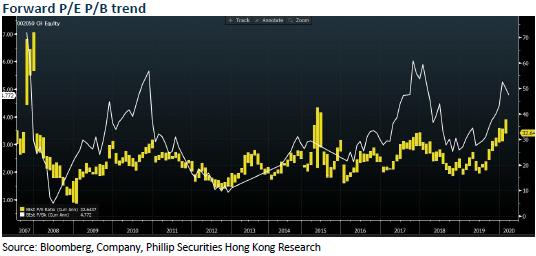

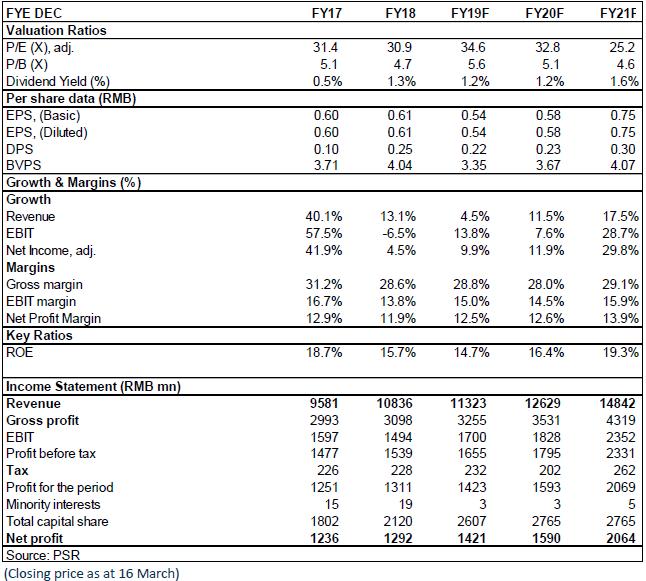

As for valuation, we expected diluted EPS of the Company to RMB0.54/0.58/0.75 of 2019/2020/2021. And we accordingly gave the target price to RMB22.4, respectively 41/39/30x P/E for 2019/2020/2021. "Accumulate" rating. (Closing price as at 16 March)

Risk

Progress of new production line is below expectations

Electric vehicle sales fall short of expectations

Macroeconomic downturn affects product demand

Sharply rising raw material prices or sharply falling product prices

Financials

Click Here for PDF format...