|

CR ASIA(831)

Analysis¡G

Despite the fact that the Hong Kong society endured serious disruptions that significantly impacted the retail industry amid weakening consumer sentiment and declining tourism, Convenience Retail Asia (831) has taken quick actions to adjust its marketing and category management programmes as well as putting a very tight control on operating expenses and capital expenditure so as to minimize the unfavourable financial impact. As a result, the Group was able to achieve solid performance. For the financial year ended 31 December, 2019, the Group`s turnover increased 5.9% to HK$5632 million and net profit rose 13.3% to HK$208 million. The Board of Directors has resolved to declare a final dividend of 19 cents per share and a special dividend of 21 cents per share. Total dividend for the year increased 109% to 46 cents, translating into a dividend yield of 12%. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $3.75, Target Price: $4.05, Cut Loss Price: $3.60

|

S-ENJOY SERVICE(1755)

Analysis¡G

The company is a property management service company under the Seazeng Group. relying on the Seazeng Group`s real estate projects, it ranks 13th in 2019 among the top 100 property service companies in China. The company`s contracted area reached 133 million square meters. In the future, with the sales growth of the Seazeng Group, the company`s performance will continue to be promoted. In addition, as the number of agency projects increases, the scale effect rose and management expense ratio decrease, and the gross profit margin is expected to increase.

Strategy¡G

Buy-in Price: $15.00, Target Price: $20.00, Cut Loss Price: $12.40

Nissui Pharmaceutical Co., Ltd (4550)

Established in 1935 as a subsidiary of Nippon Suisan (1332). Operates two business segments, namely the Clinical Diagnostics Business manufacturing, purchasing and selling diagnostic agents/test drugs, diagnostic equipment and raw materials, and the Pharmaceuticals Business handling pharmaceuticals and health foods.For 3Q (Apr-Dec) results of FY2020/3 announced on 3/2, net sales increased by 0.9% to 9.318 billion yen compared to the same period the previous year, and operating income decreased by 18.0% to 770 million yen. While sales in both business segments had increased, profits were impacted by a 15.6% YoY decrease in operating income in the Clinical Diagnostics Business where pricing had remained severe due to the unchanging government's policy of reducing medical expenses.For its full year plan, net sales is expected to increase by 6.0% to 13.3 billion yen compared to the previous year, and operating income to increase by 1.3% to 1.33 billion yen. With concerns about the global spread of COVID-19, we can expect the company to strengthen its efforts in clinical diagnostics for the said infection. Company has a high percentage of transactions with its parent company, and as a result, its independence as a subsidiary in a parent-child listing situation is an ongoing concern, and attention may need to focus on its corporate governance.Target Price : 1,295 yenBuy Price : 1,245 yenCut-Loss : 1,225 yen

|

|

|

GAC (2238.HK) - The Epidemic has a Short-term Hurt, But the Effect will be Limited in the Long Run

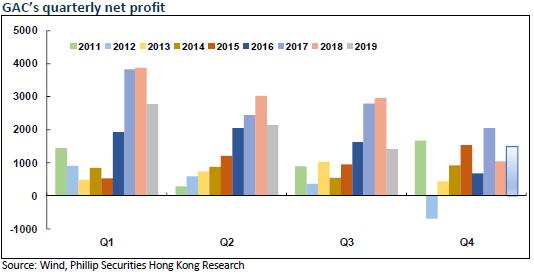

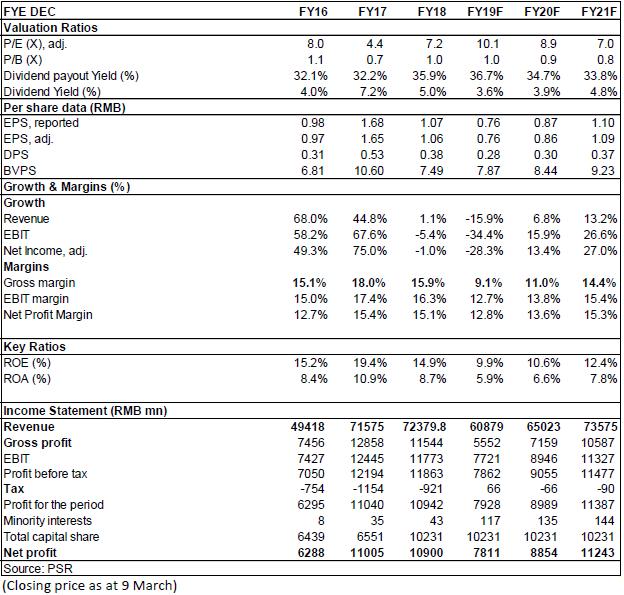

Investment SummarySales Volume maintain Steadily in 2019: Japanese JVs Maintained Strong Momentum While Self-Brand Gradually Improved since H2 Domestic automobile market trend was downward through 2019 with an overall decrease of 9%. GAC outperformed the industry due to strong Japanese JV brands, achieving a sales volume of 2.0622 million for the year, down by approximately 4% yoy. The sales volume of GAC Honda was 771,000 units, up by 4% yoy. Among popular vehicle models, average monthly sales of the 10th generation Accord was approximately 20,000 units. Annual sales volumes of both Crider and Vezel exceeded 100,000 units. The sales volume of GAC Toyota for the year was 682,000 units, increasing by 17.6% yoy, which was a lot higher than the average. Hot models like Levin, Camry, CHR, and Highlander were best sellers in respective segments. Compared with that of Honda and Toyota, annual sales volumes of joint venture brands like GAC Fiat and GAC Mitsubishi showed different ranges of decline. Sales volume of GAC Fiat in 2019 was 73,900 units, down by 40.96% yoy, while sales volume of GAC Mitsubishi for the year was 133,000 units, down by 7.64% yoy. Annual sales volume of self-brand GAC Trumpchi was 384,600 units, down by 28.14% yoy. Product upgrade and actively reducing dealer inventory were the theme of 2019. It came to our attention that monthly sales has slightly improved since 2019H2. The Epidemic has a Short-term Hurt on Automobile Market, But the Effect will be Limited in the Long Run It was estimated that automobile sales in the first quarter of 2020 will be strongly suppressed by the epidemic. We predicted that sales volume of automobiles will decrease by more than 40% yoy in 2020Q1 and a rebound will not come until April. However, the epidemic also emphasizes the convenience of having a private car, which might help boost demand of first-time car buyers. In the medium term, suppressed demand of purchasing vehicles will be frequently released starting from the second quarter. Pro-consumption Policy introduced by government later will also be helpful of stimulating consumption potential. But the epidemic will definitely have a negative effect on the annual sales volume as it will have on macro economy. Industry recovery that was supposed to happen in later half of 2019 will be accordingly postponed. The effect epidemic had on market will be limited in the long run because a trend of industrial chain marching towards middle and high-end part of the value chain characterized as four modernization (intelligent, distributed, mobile, and participatory) remains unchanged. The fact that whether automobile manufacturers can make prospective and timely adjustments in response program, marketing model and supply chain management will be a critical factor of measuring their future competitive strength. Policies Introduced by Guangzhou Government to Support Automobile Industry will Benefit GAC the Most A policy on automobile consumption was introduced by Guangzhou government in early March, which indicates that quota of vehicle licence will soon increase 100,000. Meanwhile, allowance up to RMB10,000 will be distributed to individual consumers if they purchase new-energy vehicles and RMB3,000 allowance will be distributed to those replacing their old vehicles with new ones on China VI vehicle emission standards. We believe that the policy will promote consumption in Guangzhou City and as an automobile manufacturer with biggest market share in the area, GAC will benefit the most from it. It is possible that governments in other domestic cities might follow suit in the future. Japanese joint venture brands are estimated to maintain a strong momentum of growth through 2020. GAC Honda Breeze launched in November last year and GAC Toyota Wildlander launched in February this year will continue to enhance product matrix of joint ventures in 2020. Furthermore, GAC Toyota will launch EV version of CHR and Mirai hydrogen-powered vehicle this year, while GAC Honda will launch the 4th generation Fit, Inspire Hybrid, Avancier Facelift and other new models. The production expansion project of GAC Toyota and GAC Honda is expected to be put into production at the end of the year. Each of the production capacity will increase by 120,000 to 240,000 units, which will accumulate strength for the development in the next stage. The new generation of Trumpchi is quite competitive compared with competitors. It was launched in November last year and went into mass production smoothly, which helped dramatically improve sales of GAC self-developed brand. Its future performance is worth looking forward to. Investment ThesisWe revised the Company's 2019/2020/2021 earnings forecast. We give the "Accumulate" rating with the target price to HKD 9.5, equivalent to 11/9.8/7.7x P/E and 1.1/1.0/0.9x P/B ratio in 2019/2020/2021. (Closing price as at 9 March)

Financials

Click Here for PDF format...

| Recommendation on 12-3-2020 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 8.660 | | Suggested purchase price | N/A | | Target Price | $ 9.500 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2020 Phillip Securities (HK) Ltd. All Rights Reserved.

|