|

CMGE(302)

Analysis¡G

CMGE Technology Group (302) is a IP-based game operator and publisher, focusing primarily on IPs relating to well-known cultural products and art works, such as icons or characters from popular animations, novels, and motion pictures, which have a significant fan base, market acceptance and commercial value. According to its positive profit alert, the Group is expected to record an increase of approximately 70% to 85% in its adjusted net profit for the year ended 31 December 2019, as compared to that of approximately RMB340 million for the previous year. This increase was mainly due to the launch of several popular new games, the strong performance of the Group`s existing games and the contributions from two operating subsidiaries, namely Beijing Wenmai Hudong Technology Company Limited and Softstar Technology (Beijing) Company Limited, which were acquired by the Group in 2018. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $3.37, Target Price: $3.70, Cut Loss Price: $3.20

|

CHINA TOWER(788)

Analysis¡G

China Tower is the world`s largest telecommunications tower infrastructure supplier. The three major businesses include tower business (macro station business, micro station business), room division business, and cross-industry site application and information services. The scale reached 1.967 million (global share 44.43%). We expect that after the epidemic this year, operators` 5G capital expenditures are expected to increase significantly, with a compound annual growth rate of 15% from 2020-2022. The number of new 5G base stations is expected to reach 600,000-700,000 in 2020, and the company is expected to benefit first.

Strategy¡G

Buy-in Price: $1.80, Target Price: $2.30, Cut Loss Price: $1.50

Teikoku Sen-I Co., Ltd (3302)

Founded in 1887 and established in 1907 by Teikoku Seima, its predecessor. Major business segments include the Disaster Prevention & Preparedness Business, which deals with various types of fire hoses, disaster prevention equipment, search equipment and alarms, and the Textile Business which deals with hemp and functional fibers.For FY2019/12 results announced on 14/2, net sales increased by 19.3% to 35.393 billion yen compared to the previous year, and operating income increased by 25.4% to 5.612 billion yen. Sales of the Disaster Prevention & Preparedness Business increased 31.4% to 28.235 billion yen, contributing to increased sales and profit. In addition to the expansion in sales of large-scale disaster prevention materials and security equipment for airports, sales of rescue work vehicles and airport chemical fire trucks were also firm.For its FY2020/12 plan, net sales is expected to decrease by 9.6% to 32.0 billion yen, and operating income to decrease by 34.1% to 3.7 billion yen. There is a consideration for a decline due to a temporary upside in the initial plan for the previous fiscal year (net sales of 30.0 billion yen and operating income of 45.0 billion yen). In addition to sales expansion of large-scale water supply and drainage systems for flood-related social problems, the products of the Disaster Prevention & Preparedness Business, namely pandemic (new infectious diseases)- related products as well as products for decontamination outside hospitals, that cater to prevention of the spread of COVID-19 deserve our attention.Target Price : 2,000 yenBuy Price : 1,800 yenCut-Loss : 1,700 yen

|

|

|

CEB WATER (1857.HK) - Results of 2019 exceed expectations, price and capacity both rise to promote development

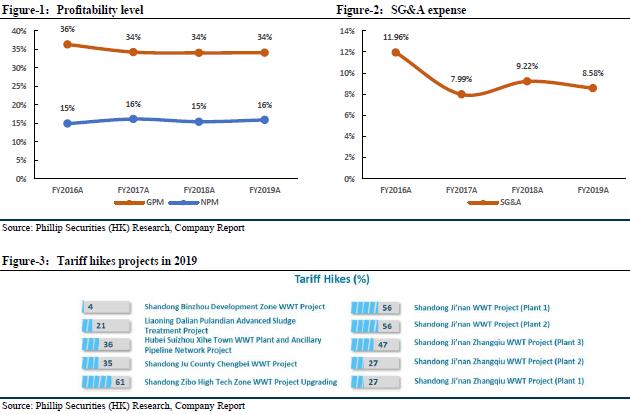

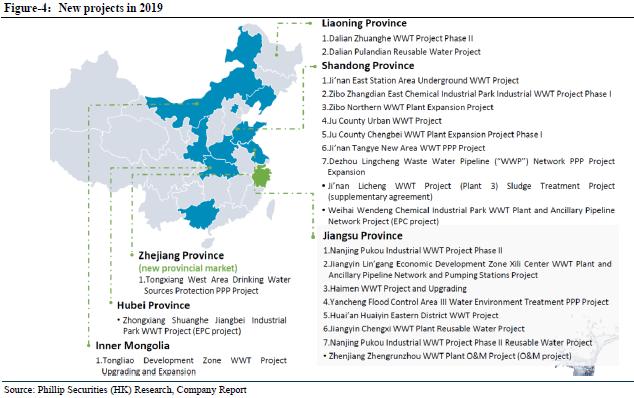

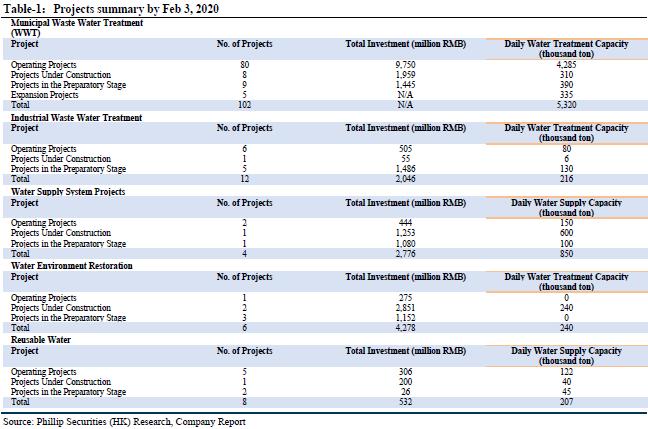

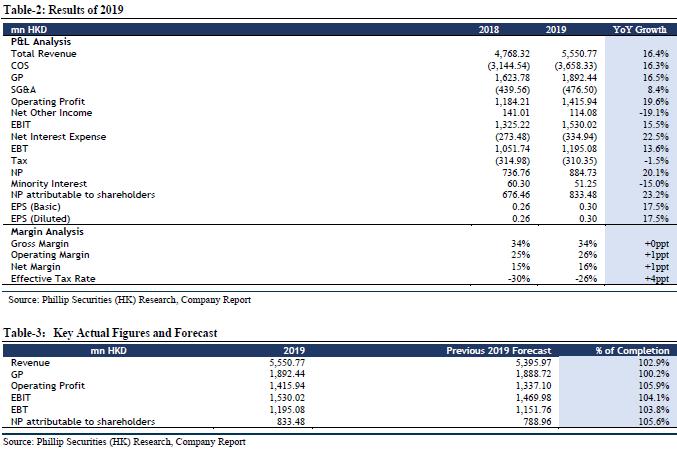

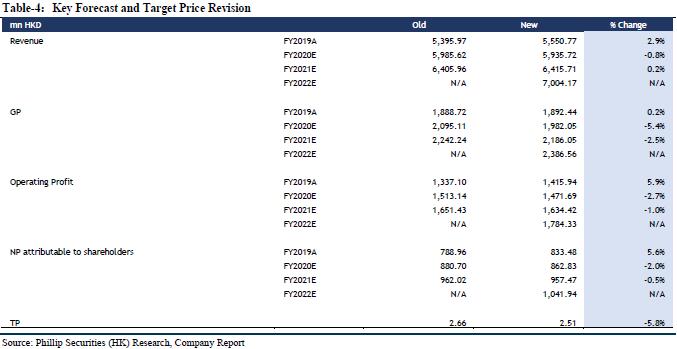

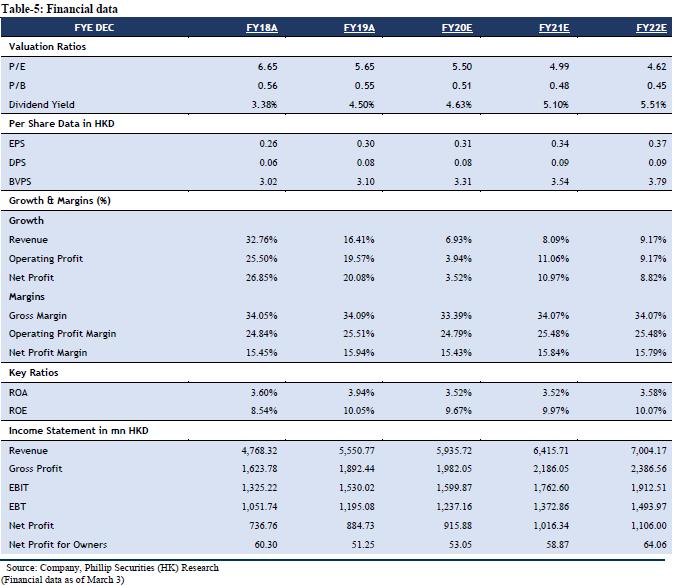

Company UpdateAs of 2019, the company has invested and held 1 raw water protection project, 3 water supply projects, 96 municipal sewage treatment projects, 12 industrial wastewater treatment projects, 1 leachate treatment project, 8 reclaimed water reuse projects, 6 basin treatment projects and 2 sewage source heat pump projects, while undertaking 2 EPC projects and 1 O&M project. The total design capacity is 850,000 cubic meters of water per day, 5.14 million cubic meters of sewage per day, and 206.6 thousand cubic meters of reclaimed water per day. The sewage source heat pump project can provide heating and cooling services for an area of 295,000 square meters. It includes 101 operating projects, 1 completed project, 14 projects under construction, and 16 preparatory projects, of which the daily water treatment capacity of the preparatory projects reaches 1.15 million cubic meters. In 2019, the company obtained a total of 18 new projects and signed a supplementary agreement, including 1 raw water protection project, 13 sewage treatment projects, 3 reclaimed water reuse projects, 1 sewage pipe network project and 1 existing Supplementary agreement for wastewater treatment projects. The newly increased capacity is 655,000 cubic meters of sewage per day, 85,000 cubic meters of daily water supply, 600,000 cubic meters of daily water supply, and 200 tons of daily sludge treatment and disposal. A total of 10 sewage treatment plants of the company were approved to raise water prices, with price adjustments ranging from 4% to 61%. A total of 18 projects of the company are under construction, with a design capacity of 354,100 cubic meters of sewage per day, 80,000 cubic meters of daily water supply, and 200 tons of sludge per day. 18 projects were completed and put into operation, with a design capacity of 440,000 cubic meters of sewage per day, 40,000 cubic meters of reclaimed water, 150,000 cubic meters of daily water supply, and 50 tons of sludge per day. 31 projects under construction, involving a daily water treatment capacity of about 790,000 cubic meters, and a daily sludge treatment of 250 tons. The company's operating projects have been steadily improved. In 2019, it will treat about 1.43 billion cubic meters of sewage and supply about 17.65 million cubic meters of reclaimed water, an increase of 13% and 10% year-on-year. The company's business capacity has steadily expanded. It has now spread to 10 provinces, municipalities and autonomous regions. Various engineering construction projects have been steadily advanced. The quality of operation and management projects has gradually increased, laying a foundation for the further development of the company's performance. In 2019, the company recorded revenue of HKD 5.55 billion, a year-on-year increase of 16%, an increase of 2.4 percentage points from the first three quarters of 2019. The increase in revenue was mainly due to an increase of HKD 300 million in construction revenue, an increase of HKD 300 million in operating income, an increase of HKD 76 million in financial revenue, and an increase of HKD 99 million in technical services revenue, representing year-on-year growth of 11%, 25%, 10% and 98%. The above-mentioned increase in revenue was mainly due to the increase in new projects, the operation of some new projects and the increase in water prices of some projects. The company's gross profit was HKD 1.89 billion, a year-on-year increase of 17%, which was 2.1 percentage points lower than the growth rate of gross profit in the first three quarters of 2019. The gross profit margin was maintained at 34% because the revenue share of construction business (about 24% gross profit margin) and operating services (about 47% gross profit margin) was similar to the previous year. Among them, construction revenue, construction contract revenue and technical service revenue totaled approximately 58%. Profit attributable to equity holders of the company was HKD 830 million, an increase of 23% year-on-year, and an increase of 5.9 percentage points from the first three quarters of 2019. The company's various operating indicators exceeded our expectations, reflecting the company's good project growth and cost management capabilities. We believe that the impact of the new pneumonia epidemic on the company is relatively limited. Although the shutdown of some industrial enterprises has affected the wastewater treatment capacity of the company's industrial park, a slight increase in municipal domestic sewage offsets this impact, and the industrial wastewater treatment capacity is expected to gradually recover in the near future, and I believe that it will soon return to normal levels. In terms of construction projects, the company's resumption of work after the holiday this year has been delayed compared to previous years, but it has gradually resumed work. I believe the government's encouragement of resumption of production will gradually ease the shutdown happening. In addition, the company's liability ratio increased slightly in 2019, an increase of 2.1 percentage points from last year to 57.9%. However, the return on shareholders` equity also increased by 1.4 percentage points to 9.9%, reflecting the improvement of the company's profitability. The dividend payout ratio increased slightly by 2 percentage points to 25%. The company's management believes that there is still room for improvement in the future dividend payout ratio. In addition, the company expects capital expenditure of approximately HKD 3 billion in 2020, which will maintain approximately the same growth rate as in 2019. Adjust TP and maintain "BUY" Rating We adjusted our forecast for FY20/FY21/FY22 incomes to HKD 5.936/6.416/7.004 billion, showing increases of 6.93%/8.09%/9.17% YoY; net profit attributable to shareholders were HKD 863/957/1,042 million, with increase of 3.52%/10.97%/8.82% YoY; the corresponding EPS was HKD 0.3090/0.3404/0.3677. The target price was adjusted to HKD 2.51, corresponding to FY20/FY21/FY22 8.11x/7.36x/6.81x PE, which was +47.39% higher than the current price (HKD 1.70 as of March 3, 2020), maintaining a ¡§BUY¡¨ rating.

RiskProject progress fail expectations; Industry policy; M&A fails expectations. �Financials

Click Here for PDF format...

| Recommendation on 10-3-2020 | | Recommendation | BUY | | Price on Recommendation Date | $ 1.700 | | Suggested purchase price | N/A | | Target Price | $ 2.510 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2020 Phillip Securities (HK) Ltd. All Rights Reserved.

|