|

FSE SERVICES(331)

Analysis¡G

FSE Services (331) has 4 business segments, namely E&M Engineering, Environmental Management Services, Facility Services, Laundry. During the six months ended 31 December 2019, the Group recorded revenue amounting to HK$2,420.3 million, representing a decrease of 4.4%, as compared with the same period of 2018. However, profit attributable to shareholders increased by 3.7% to HK$144 million, mainly reflecting the stable gross profit contribution with an overall savings in general and administrative expenses despite the one-off professional fees for the acquisition of the property and facility management services business. The interim dividend was increased by 26.7%, representing a payout ratio of 54.1%, much higher compared to 32.6% in the same period of 2018. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $3.75, Target Price: $4.20, Cut Loss Price: $3.55

|

CHINASOFT INT`L(354)

Analysis¡G

China Software International is a leading large-scale comprehensive software and information service company in China. Since its establishment, it has successively established strategic cooperative relationships with major customers such as Microsoft, Huawei, and Tencent. Huawei is the company`s largest customer, accounting for 53% of its revenue. In recent years, the company has opened up a new segment of cloud intelligent business for transformation and upgrade by integrating the existing business. This business segment has developed rapidly and its gross profit margin has become an important source of profit for the company. In the future, independent and controllable research and development of Huawei`s R & D outsourcing will drive performance back to high growth.

Strategy¡G

Buy-in Price: $4.70, Target Price: $6.50, Cut Loss Price: $3.70

Aeon Financial Services¡]8570¡^

Established in 1981 as a subsidiary of JUSCO (currently AEON (8267)). Carries out the financial services business of AEON Group. Following the change to a business firm (previously a bank holding company) on 1/4, their accounting period changed from end March to end February.For 3Q (Apr-Dec) results of FY2020/3 announced on 14/2, operating revenue increased by 9.8% to 356.12 billion yen compared to the previous period and operating income decreased by 17.3% to 43.139 billion yen. Despite a contribution in revenue increase due to a strengthening of services to members acquired through the government's promotion of cashless payments, the increase in the provision for doubtful receivables in the ASEAN region and Hong Kong, etc. have affected, which led to a decrease in profit.For its FY2020/2 full year plan, operating revenue is expected to be 430 billion yen and operating income to be 70 billion yen. Rate of change compared to the previous period is undisclosed due to a change in the accounting period. In the government's Future Investment Meeting, overseas expansion of the Japan standardised QR code (JPQR) via mutual entry of standards between various Asian countries was included in the growth strategy execution plan. There are expectations of a change in the important.Target Price : 1,850 yenBuy Price : 1,712 yenCut-Loss : 1,655 yen

|

|

|

CEB WATER (1857.HK) - Results of 2019 exceed expectations, price and capacity both rise to promote development

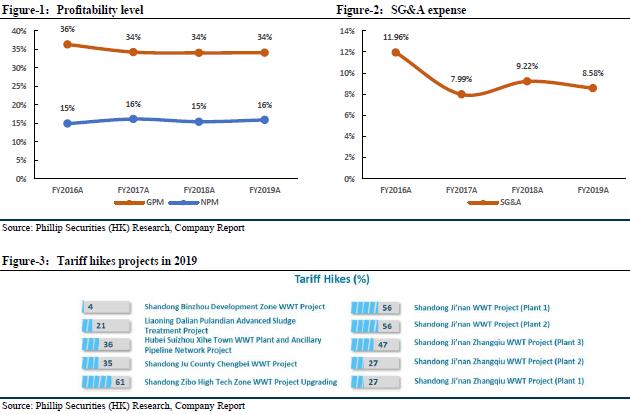

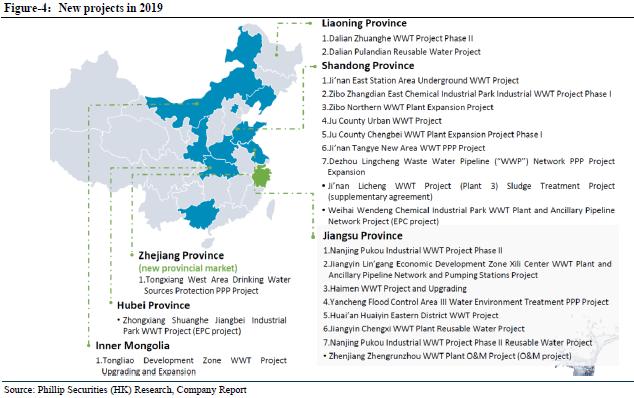

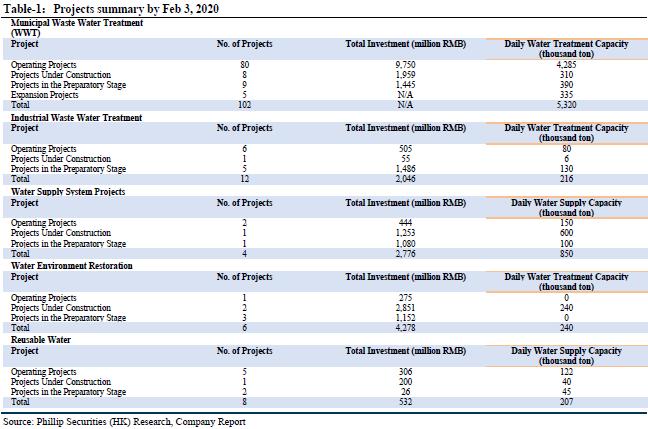

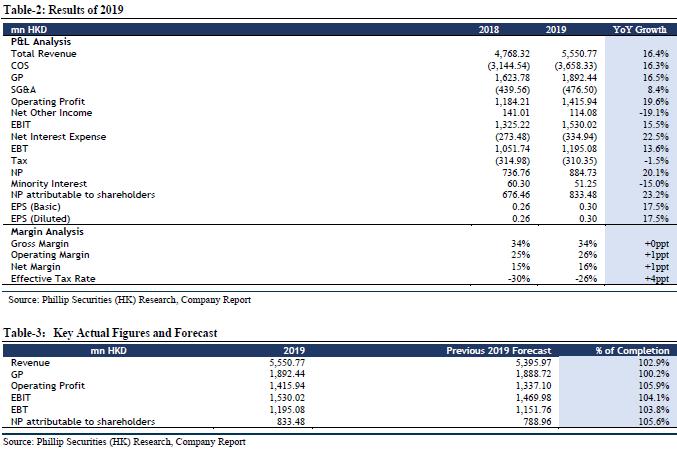

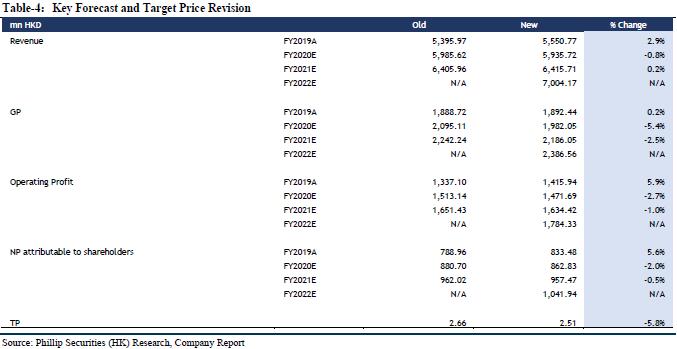

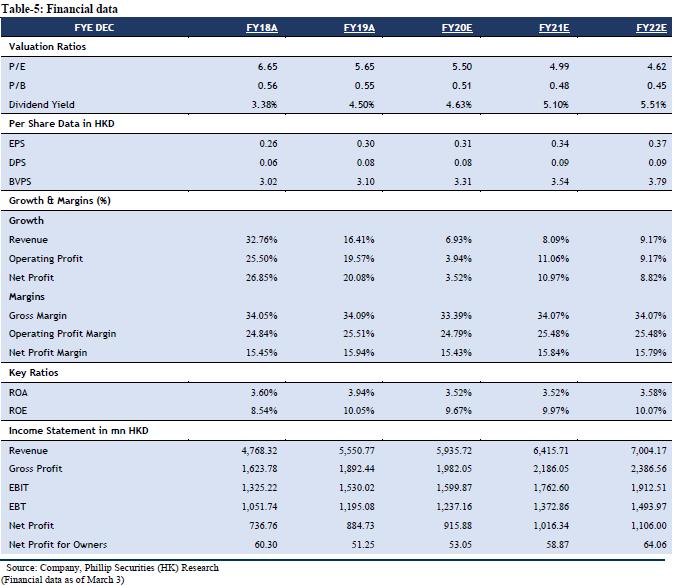

Company UpdateAs of 2019, the company has invested and held 1 raw water protection project, 3 water supply projects, 96 municipal sewage treatment projects, 12 industrial wastewater treatment projects, 1 leachate treatment project, 8 reclaimed water reuse projects, 6 basin treatment projects and 2 sewage source heat pump projects, while undertaking 2 EPC projects and 1 O&M project. The total design capacity is 850,000 cubic meters of water per day, 5.14 million cubic meters of sewage per day, and 206.6 thousand cubic meters of reclaimed water per day. The sewage source heat pump project can provide heating and cooling services for an area of 295,000 square meters. It includes 101 operating projects, 1 completed project, 14 projects under construction, and 16 preparatory projects, of which the daily water treatment capacity of the preparatory projects reaches 1.15 million cubic meters. In 2019, the company obtained a total of 18 new projects and signed a supplementary agreement, including 1 raw water protection project, 13 sewage treatment projects, 3 reclaimed water reuse projects, 1 sewage pipe network project and 1 existing Supplementary agreement for wastewater treatment projects. The newly increased capacity is 655,000 cubic meters of sewage per day, 85,000 cubic meters of daily water supply, 600,000 cubic meters of daily water supply, and 200 tons of daily sludge treatment and disposal. A total of 10 sewage treatment plants of the company were approved to raise water prices, with price adjustments ranging from 4% to 61%. A total of 18 projects of the company are under construction, with a design capacity of 354,100 cubic meters of sewage per day, 80,000 cubic meters of daily water supply, and 200 tons of sludge per day. 18 projects were completed and put into operation, with a design capacity of 440,000 cubic meters of sewage per day, 40,000 cubic meters of reclaimed water, 150,000 cubic meters of daily water supply, and 50 tons of sludge per day. 31 projects under construction, involving a daily water treatment capacity of about 790,000 cubic meters, and a daily sludge treatment of 250 tons. The company's operating projects have been steadily improved. In 2019, it will treat about 1.43 billion cubic meters of sewage and supply about 17.65 million cubic meters of reclaimed water, an increase of 13% and 10% year-on-year. The company's business capacity has steadily expanded. It has now spread to 10 provinces, municipalities and autonomous regions. Various engineering construction projects have been steadily advanced. The quality of operation and management projects has gradually increased, laying a foundation for the further development of the company's performance. In 2019, the company recorded revenue of HKD 5.55 billion, a year-on-year increase of 16%, an increase of 2.4 percentage points from the first three quarters of 2019. The increase in revenue was mainly due to an increase of HKD 300 million in construction revenue, an increase of HKD 300 million in operating income, an increase of HKD 76 million in financial revenue, and an increase of HKD 99 million in technical services revenue, representing year-on-year growth of 11%, 25%, 10% and 98%. The above-mentioned increase in revenue was mainly due to the increase in new projects, the operation of some new projects and the increase in water prices of some projects. The company's gross profit was HKD 1.89 billion, a year-on-year increase of 17%, which was 2.1 percentage points lower than the growth rate of gross profit in the first three quarters of 2019. The gross profit margin was maintained at 34% because the revenue share of construction business (about 24% gross profit margin) and operating services (about 47% gross profit margin) was similar to the previous year. Among them, construction revenue, construction contract revenue and technical service revenue totaled approximately 58%. Profit attributable to equity holders of the company was HKD 830 million, an increase of 23% year-on-year, and an increase of 5.9 percentage points from the first three quarters of 2019. The company's various operating indicators exceeded our expectations, reflecting the company's good project growth and cost management capabilities. We believe that the impact of the new pneumonia epidemic on the company is relatively limited. Although the shutdown of some industrial enterprises has affected the wastewater treatment capacity of the company's industrial park, a slight increase in municipal domestic sewage offsets this impact, and the industrial wastewater treatment capacity is expected to gradually recover in the near future, and I believe that it will soon return to normal levels. In terms of construction projects, the company's resumption of work after the holiday this year has been delayed compared to previous years, but it has gradually resumed work. I believe the government's encouragement of resumption of production will gradually ease the shutdown happening. In addition, the company's liability ratio increased slightly in 2019, an increase of 2.1 percentage points from last year to 57.9%. However, the return on shareholders` equity also increased by 1.4 percentage points to 9.9%, reflecting the improvement of the company's profitability. The dividend payout ratio increased slightly by 2 percentage points to 25%. The company's management believes that there is still room for improvement in the future dividend payout ratio. In addition, the company expects capital expenditure of approximately HKD 3 billion in 2020, which will maintain approximately the same growth rate as in 2019. Adjust TP and maintain "BUY" Rating We adjusted our forecast for FY20/FY21/FY22 incomes to HKD 5.936/6.416/7.004 billion, showing increases of 6.93%/8.09%/9.17% YoY; net profit attributable to shareholders were HKD 863/957/1,042 million, with increase of 3.52%/10.97%/8.82% YoY; the corresponding EPS was HKD 0.3090/0.3404/0.3677. The target price was adjusted to HKD 2.51, corresponding to FY20/FY21/FY22 8.11x/7.36x/6.81x PE, which was +47.39% higher than the current price (HKD 1.70 as of March 3, 2020), maintaining a ¡§BUY¡¨ rating.

RiskProject progress fail expectations; Industry policy; M&A fails expectations. �Financials

Click Here for PDF format...

| Recommendation on 5-3-2020 | | Recommendation | BUY | | Price on Recommendation Date | $ 1.700 | | Suggested purchase price | N/A | | Target Price | $ 2.510 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2020 Phillip Securities (HK) Ltd. All Rights Reserved.

|