|

NEWBORNTOWN(9911)

Analysis¡G

Newborn Town Inc. (9911) is a mobile app developer and mobile advertising platform services provider based on AI technologies. The Group generates revenue mainly from the traffic monetisation of its self-developed mobile apps and the provision of mobile advertising services to advertisers as an ad agency through its proprietary advertising platform. According to its positive profit alert, the Group is expected to record an increase of no less than 30% in its revenue from contracts with customers for the year ended 31 December 2019 and an increase of no less than 60% in its adjusted net profit. The expected increase is primarily a result of rapid growth in revenue from proprietary app traffic monetisation business leveraged by user base accumulation and upgraded monetisation efficiency and the Group`s continued efforts to proactively expand the PRC market. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $2.40, Target Price: $2.80, Cut Loss Price: $2.20

|

A-LIVING(3319)

Analysis¡G

The company is a well-known property management service provider, which is spun off from Agile Group (3383). The company is able to provide a comprehensive service portfolio and has three main business areas, namely property management services, non-owner value-added services and owner value-added services, forming an integrated service range covering the entire property management value chain. The outbreak of this epidemic highlights the value of property management stocks.

Strategy¡G

Buy-in Price: $34.00, Target Price: $41.00, Cut Loss Price: $27.00

ITOCHU Advanced Logistics Investment Corporation (3493)

Established in May 2018 then listed in Sep 2018. Is a distribution facility REIT sponsoring ITOCHU, which is strong in lifestyle consumption-related businesses that have a high affinity with distribution. Their flagship property is the ¡§i Missions Park Inzai¡¨ in Chiba Prefecture.For FY2019/7 (Feb-Jul) results announced on 13/9, operating revenue increased by 32.1% to 1.718 billion yen compared to the previous period (FY2019/1), operating income increased by 9.9% to 810 million yen and distribution per unit including profit excess was 2,311 yen. I Missions Park Inzai and i Missions Park Moriya 2 were additionally acquired at 4.99 billion yen. Total acquisition price was 58.83 billion yen.For FY2020/1 period, operating revenue increased by 2.7% to 1.764 billion yen compared to the previous period (FY2019/7), operating income increased by 1.5% to 822 million yen and distribution per unit including profit excess increased by 2.4% to 2,366 yen. Predicted annual dividend interest based on the closing price on 20/2 is 3.78%. In addition to having their strength to be stable cash flow from tenants who are mainly clients of ITOCHU Group and the group itself, it is predicted that future expansion of e-commerce will support the demand of distribution facilitiesTarget Price : 130,000 yenBuy Price : 124,000 yenCut-Loss : 120,000 yen

|

|

|

CANVEST ENV (1381.HK) - Relevant policies issued, sector with high certainty

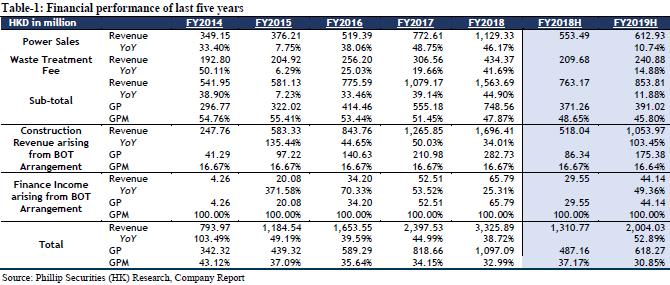

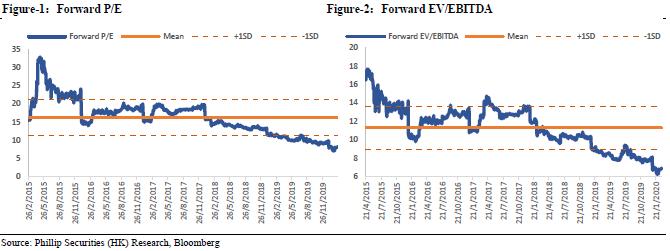

Event UpdateOn January 20, 2020, the Ministry of Finance, the National Reform Commission and the National Energy Administration jointly issued "Several Opinions on Promoting the Healthy Development of Non-aqueous Renewable Energy Power Generation" and "About Printing and Distribution Notice of the "Administrative Measures for Renewable Energy Electricity Price Additional Funds", the "Opinions " pointed out that the current subsidy method should be improved to settle expenditures and reasonably determine the scale of new subsidy projects; fully guarantee the continuation of policies and reasonable incomes on existing projects. For the renewable energy power generation projects that have been approved (recorded) in accordance with regulations, all units have been connected to the grid, and reviewed and included in the subsidy list, the central government subsidy quota will be determined based on reasonable utilization hours. For existing projects that have been voluntarily converted to parity projects, the finance and energy authorities will provide policy support in terms of preferential payment of subsidies and the scale of new projects. Subsequently, on February 6, the National Development and Reform Commission issued the "Notice on Implementing Several Opinions on Promoting the Healthy Development of Non-aqueous Renewable Energy Power Generation and Accelerating the Compilation of Medium- and Long-Term Special Plans for Domestic Waste Incineration and Power Generation." It requires the compilation of special mid-to-long-term plans for domestic waste incineration and power generation, and prepare them before March 31, 2020. "Notice" pointed out that the national renewable energy price supplementary subsidy funds are preferentially used for projects included in special planning. For those provinces (autonomous regions and municipalities) that is not received a special plan by development and reform commissions before March 31, 2020, in principle, the subsidy funds needed for new domestic waste incineration power generation projects should be settled by the provinces (autonomous regions and municipalities) where they are located. It's believed that electricity price subsidies, as an important part of project investment returns, have made great contributions to cultivating high-quality companies, promoting technological progress, and promoting industrial development. But at the same time, due to the amount of waste treatment guarantee and the price adjustment clauses of the treatment service fee when the project contract is signed, the company has a certain bargaining power, which can offset the impact of the national subsidy and decline to a certain extent, and maintain corporate profits. Refining management of single project, improving operating efficiency while reducing operating costs, bring synergistic effects between projects, and sharing fixed costs, will also be an alternative development direction for waste incineration enterprises. According to statistics from the data center of the E20 Research Institute, from January to December 2019, China has released more than 150 waste incineration projects with a total investment of more than 58 billion RMB. We believe that although the suspension of construction projects will have a negative impact on enterprises due to the epidemic situation in early 2020, the stability of operating projects and the increase in the requirements for waste disposal by the epidemic will also benefit the relevant sectors. According to the company's disclosure, on January 20, 2020, the company's subsidiary, Canvest Kewei, had obtained the PPP concession right for Yingkou WTE Plant in Yingkou City, Liaoning Province. The total daily municipal solid waste processing capacity would be 2,250 tons. The Yingkou WTE plant will be constructed in two phases, of which the processing capacity of the first phase is 1,500 tons and the processing capacity of the second phase is 750 tons. The garbage disposal fee is expected to be RMB 66 per ton, while the construction cost is approximately RMB 50 to 60 per ton. The company's total processing capacity is currently estimated to be approximately 42,680 tons, and the processing capacity has been steadily increased. Maintain ¡§BUY¡¨ investment ratingWe are still optimistic about the performance of WTE companies in 2020, and the issuances of related policies have also alleviated investors` concerns about the decline of the country subsidies. With company's high-quality projects in hand and cooperation with SIIC, and through the support of policies such as the Yangtze River Delta development plan and the Yangtze River Protection, it is expected the company would have a stable performance in 2020. We fine-tuned the model and revised TP to HKD 5.06, corresponding to PE of FY19/FY20/FY21 14.20x/12.13x/10.26x, with a +34.31% potential increase from the current price (HKD3.77 as of February 25, 2020), maintaining "Buy" investment rating.

RiskFail expectations of project progress; policy risk of electricity price allowance; fail expectations of acquisition of new projects Financials

Click Here for PDF format...

| Recommendation on 3-3-2020 | | Recommendation | BUY | | Price on Recommendation Date | $ 3.770 | | Suggested purchase price | N/A | | Target Price | $ 5.060 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2020 Phillip Securities (HK) Ltd. All Rights Reserved.

|