Backed by the parent company to build up a whole healthcare industry chain group

Genertec Universal Medical Group Company Limited is a diversified medical and health enterprise focusing on fast growing segment of healthrelated industry in China. It was listed in Hong Kong in 2015. The largest shareholder is China General Technology (Group) Holding Company Limited, which is one of the key SOE under direct administration of the PRC central government with medical services and healthcare as its main business, and one of the three SOEs approved by the SASAC with a focus on healthcare industry and a Fortune 500 enterprise. In recent years, the company has continuously expanded the resources of the medical industry, and gradually established focusing on medical services and, surrounding it, developing medical finance, medical technology services, medical digitalization business, medical and elderly care services and medical health insurance in a synchronized manner. The company's business involves two major segments, of which the finance and advisory segment includes finance leasing, advisory services (industry, equipment and financing advisory and clinical department upgrade services) and medical equipment sales, while the hospital group segment includes comprehensive medical services and hospital operation management services and other business.

In the first three quarters of 2019, the company's performance maintained steady growth, of which operating income was 4.986 billion yuan, an increase of 53.28% YoY, and profit for the period was 1.437 billion yuan, an increase of 22.71% YoY, and profit attributable to shareholders also increased more than 10% YoY. In respect of finance and advisory business, net interest margin and net interest spread both increased, non-performing assets ratio kept stable and provision coverage ratio remained at a solid and healthy level. In respect of hospital group business, the company further promoted the reintegration work on spin-off and takeover of medical institutions of SOEs and made positive progress. In the meantime, the company actively integrated its medical resources for steady integration and management of cooperating medical institutions to gradually emerge nationwide medical service network.

The integration and undertaking of SOE hospitals progress smoothly, the consolidation of hospitals is gradually completed

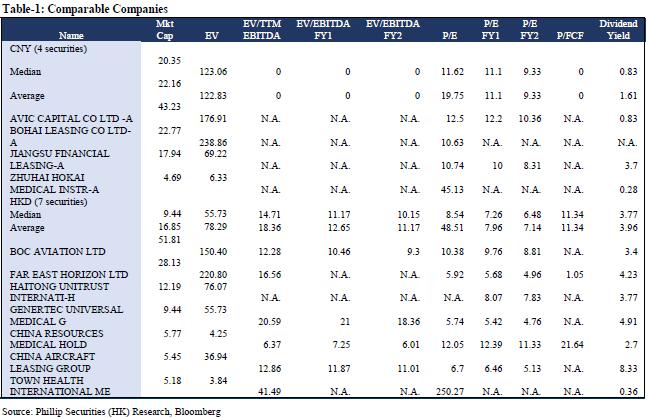

In August 2017, since the joint issue of the Guidance on Deepening the Reform of Educational and Medical Institutions of State-owned Enterprises (Guo Zi Fa Gai Ge [2017] No.134) by six ministries and commissions including the State-owned Assets Supervision and Administration Commission of the State Council, it is required the reform of medical institutions of SOEs by way of spin-off was further carried out and SOEs primarily engaging in healthcare business to integrate resources of other SOEs` medical institutions to achieve centralized management and professional operation by the end of 2018. The company has actively participated in the integration and takeover of their medical institutions through formation of joint ventures and open market bidding, and has made great progress. By the end of 2019, the company has signed contracts with nearly 50 medical institutions through equity control. The total number of opening beds is estimated to be over 14,000. It is expected that the consolidation of most hospitals will be completed by 2020. In addition, as of the first half of 2019, the company has completed the delivery of 16 medical institutions, and the average revenue per bed of the consolidated hospital was 230,000 yuan (annualized 460,000 yuan). The average outpatient expense and inpatient expense were 259 yuan and 9,225 yuan. The company's management estimates that the total number of opening beds in the next 3 to 5 years will reach about 30,000, and the hospital group's revenue will account for more than 50%.

In December 2019, the company made a capital contribution to Yangmei Hospital Management under Yang Quan Coal Industry, holding 51% shares. Yangmei Hospital Management is the promoter of the target hospitals, which are located in Shanxi, Yangquan, with actual capacity of more than 2,100 beds. The target hospitals recorded an aggregated net profit of approximately RMB63.13 million and RMB13.57 million for the year 2017 and 2018, respectively. The Target Hospitals are not-for-profit legal entities, and as of 30 October 2019, the aggregated unaudited book value of assets of the target hospitals were approximately RMB361.58 million. In particular, General Hospital of Yang Quan Coal Industry (Group) Co., Ltd. is a Grade III Class A comprehensive hospital with an actual capacity of 1,155 beds. With sound financial performance, it has competitive advantages in terms of scale, reputation, geographical location and balance level.

Medical finance business keeps growing and asset quality remains healthy level

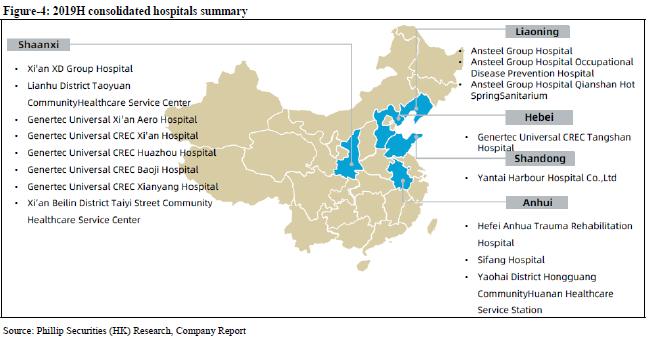

The company achieved interest income of 1.893 billion yuan in the first half of 2019, a YoY increase of 26.2%. The company continued to maintain its leading position in the medical financing leasing market. The medical industry interest income was 1.468 billion yuan, accounting for 77.5%. The net interest margin of financial leasing in the first half of 2019 was 4.28%, an increase of 0.02 ppts compared last year; the net interest spread was 3.45%, an increase of 0.12 ppts, and continued to maintain the industry's excellent level. As of the third quarter of 2019, the company's total assets were 53.692 billion yuan, an increase of 15.0% YoY, maintaining a steady growth. The provision coverage ratio of financial leasing business in the first half of 2019 was 190.27%, an increase of 0.03 ppts compared with 2018. The non-performing asset ratio was 0.80%, a slight decrease of 0.01 ppts compared with 2018.

Refocus recommended with "BUY" rating

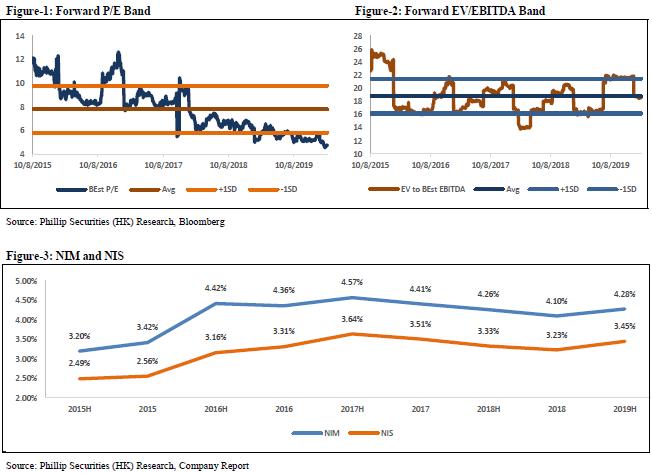

In view of the gradual increase in the company's consolidated hospitals, the steady growth in revenue and asset scale, and the maintenance of a good level of profitability and asset quality, we are optimistic about the future integration of the company's medical resources and the coordinated development in the industry chain, and we recommend refocus on it. We use SOTP for valuation and considering the effects between two major businesses, we adjust the target price to 6.91 HKD, corresponding to FY19 / FY20 / FY21 8.33x/6.54x/5.61x PE, which is +26.48% increase from the current price (HKD 5.46 as of February 18, 2020) , giving "BUY" rating.

Risk

Progress of hospital consolidation fails expectations; New contracts fail expectations; Interest rates risk; Policy risk.

Financials

Click Here for PDF format...