Investment Summary

The North America Factory Keeps picking up, Partly Compensating for the Slipping Domestic Auto Market

The North American factory that Fuyao has been cultivating for many years has further climbed, partially compensating for the downward pressure in the domestic auto market. In addition, the acquisition of SAM in Germany has been consolidated since March, and the total revenue of Fuyao has continued to grow against doldrums in the car market.

The total revenue of Fuyao in 2019M9 was RMB15.634 billion, with a yoy growth of 3.4%. Net profit was 2.347billion, a decrease of 28% yoy; net profit excluding non-recurring items was 2.13billion, decreasing by 24.5% yoy.

As for 2019Q3, the total revenue reached 5.35 billion, with a yoy increase of 6.1% yoy and net profit was 0.84billion, down by 39.7% yoy; net profit excluding non-recurring items was 0.79billion, decreasing by 20.3% yoy.

The result decrease of the third quarter is due to: 1) RMB450million investment income by selling the equity of Beijing Futong in the same period last year while this year there was no such income; 2) Exchange earnings decreased by RMB50 million compared with the same period last year; 3) Integration cost after acquiring Germany SAM aluminium decorative strip business; 4) domestic car market slows down.

Excluding the influence of the first three factors, Fuyao's EBIT in 2019Q3 fell by about 10%, half of the decrease in the first half of the year, reflecting an improvement in the domestic car market in Q3.

Gross Margin End under Pressure and Expenses Are Well Controlled

The company's gross margin recorded in the first three quarters were 39.08%, 36.1%, 37.24%, respectively, with a yoy decrease of 2.84%,5.9% and 6.9%, respectively. The pressure on the gross margin end is mainly due to 1) the impact of Germany SAM consolidation; 2) the low utilization rate of production capacity, high pressure of product price reduction and increased float glass inventory caused by the depressed car market, and 3) the gross margin of North America business is still in the climbing period, and the expansion of its proportion has lowered the overall gross margin level. The company continued to strengthen cost control, with sales cost ratio, management and research and development cost ratios falling by 0.1/0.4/0.1 ppts yoy, respectively in the third quarter.

Gross Margin under Pressure and Expenses Are Well Controlled

The company's gross margin recorded in the first three quarters were 39.08%, 36.1%, 37.24%, respectively, with a yoy decrease of 2.84, 5.9 and 6.9 ppts, respectively. The pressure on the gross margin is mainly due to 1) the impact of Germany SAM consolidation; 2) the low utilization rate of production capacity, high pressure of product price reduction and increased float glass inventory caused by the depressed car market, and 3) the gross margin of North America business is still in the climbing period, and the expansion of its proportion has lowered the overall gross margin level. The company continued to strengthen cost control, with sales, administrative and R&D expense ratios falling by 0.1/0.4/0.1 ppts yoy, respectively in the third quarter.

The Negative Factors are Dissipating and the Glass Giant Is Starting a New Round of Growth

The company acquired Germany SAM assets of aluminium decorative strip business, and made a large investment in the early stage of integration. In the third quarter alone, it incurred a loss of EUR14.8 million, which encumbered the most on the company's main business. At present, the integration work is progressing smoothly. The losses caused by SAM will be lowered in the fourth quarter. It is expected that the integration will be completed in the first quarter of 2020 and the business will break even the end of 2020. Subsequent companies are expected to cooperate with domestic capacity of aluminium refining/aluminium extrusion to further integrate the industrial chain, strengthen the integration capability of Fuyao's automotive glass and expand new development space.

U.S. factory's target of 3.9 million sets of car glass in 2019 will stay unchanged and will reach 4.6 million sets in 2020. With the improvement of capacity utilization rate, there is still room for improvement in the US market.

It has become a high probability event for the domestic car market to head for a moderately structural recovery after adjustment. The company recently revealed that it has become a glass supplier of window and triangular window for Tesla's Shanghai factory, demonstrating its strength in product and industrial position. It is expected to take a share in Tesla's global expansion in the future.

The company continued to promote the development of products in the direction of safety, energy saving and intelligent integration. The revenue share of high value-added products such as heat insulation glass, soundproof glass, head-up display glass, dimmable, UV protection, hydrophobic glass, solar energy and hemming modularization increased by 2% year on year. The continuous upgrading of product mix provided support for the subsequent increase in gross profit.

Investment Thesis

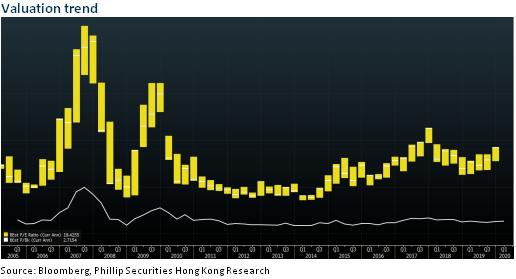

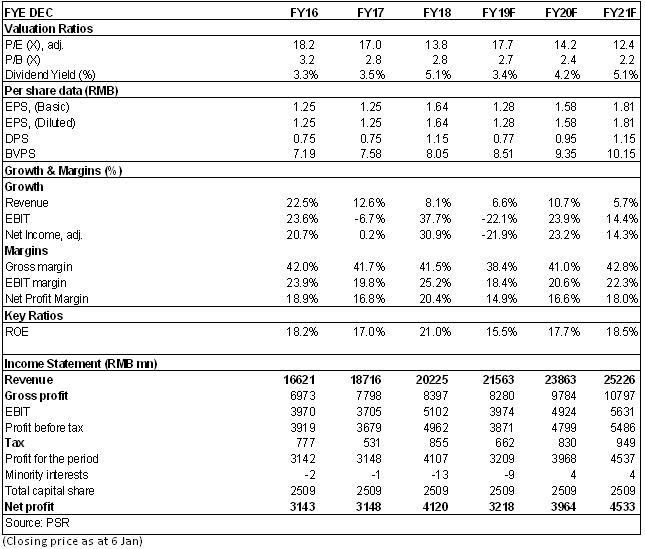

Overall, considering the steady leading position, continuous optimization of the product structure and a high dividend rate provide a greater margin of safety for the Company. We give the "Accumulate" rating¡Awith target price to be HK$28, equivalent to 19.4/15.6/13.6x P/E for 2019/2020/2021E. (Closing price as at 6 Jan)

Risks

Demand for automobiles keeps sluggish; cost of raw materials increases; RMB appreciates

Catalyst

Success market development of overseas automobile market; rebound of domestic demand for automobile; depreciation of RMB

Financials

Click Here for PDF format...