|

|

HEC PHARM(1558)

Analysis¡G

The company expected that it will record a revenue of approximately RMB6,220 million and approximately RMB1,780 million for the year 2019 and Q42019 respectively, representing an increase of approximately 145% and approximately 125% YoY respectively. The expected increase in revenue of the Company is primarily attributed to the continuous increase in the sales revenue of Kewei, the company`s core product; the expansion of portfolio of the company`s products; and increasing penetration of the company`s products in medical institutions across the country as well as the continuous promotion efforts by the company on its products in professional academic market. On 3 January 2020, the company entered into a strategic cooperation framework agreement with CR Pharmaceutical Commercial whereby the company and CR Pharmaceutical Commercial will jointly develop an internet platform dedicated to establishing online channels directly serving end-users and patients by leveraging on the distribution network and drug storage capability of CR Pharmaceutical Commercial, in order to enhance response to unexpected demand for the Company`s core product, Kewei (oseltamivir phosphate) series, across China as well as to improve terminal coverage of other products.

Strategy¡G

Buy-in Price: $41.00, Target Price: $45.00, Cut Loss Price: $38.00

Mitsubishi Estate Co., Ltd. (8802)

Established in 1937. Expands a wide variety of businesses such as the office building business focusing on the leasing of owned buildings, the lifestyle property business focusing on the development and leasing of commercial facilities and distribution facilities, the residential business focusing on the retail of apartments / detached houses, the international business, investment management business, architectural design and engineering business, the hotel and airport business, and the real estate services business, etc.For 1H (Apr-Sep) results of FY2020/3 announced on 7/11, operating revenue decreased by 7.3% to 535.226 billion yen compared to the same period the previous year, operating income decreased by 13.7% to 92.276 billion yen and net income decreased by 22.2% to 48.078 billion yen. Effects from earnings following a property sale recorded in the office building business in the same period the previous year have shown. In the residential business, there has been a decline in the number of recorded sales of houses in apartments.For its FY2020/3 plan announced on 14/5, net sales is expected to increase by 7.7% to 1.36 trillion yen compared to the previous year, operating income to increase by 0.4% to 230 billion yen and net income to increase by 1.8% to 137 billion yen. Percentage of vacant units in the office building business is at 1.98% (as of end Aug 2019). Company owns many prime properties in Marunouchi and is likely to capture the leasing needs of strong buildings.Target Price : 2,230 yenBuy Price : 2,060 yenCut-Loss : 1,950 yen

|

|

|

SH Pharma (2607.HK) - Rapid growth in core segments, promising in innovation transformations

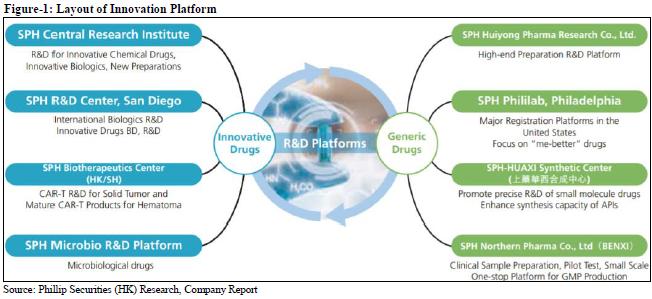

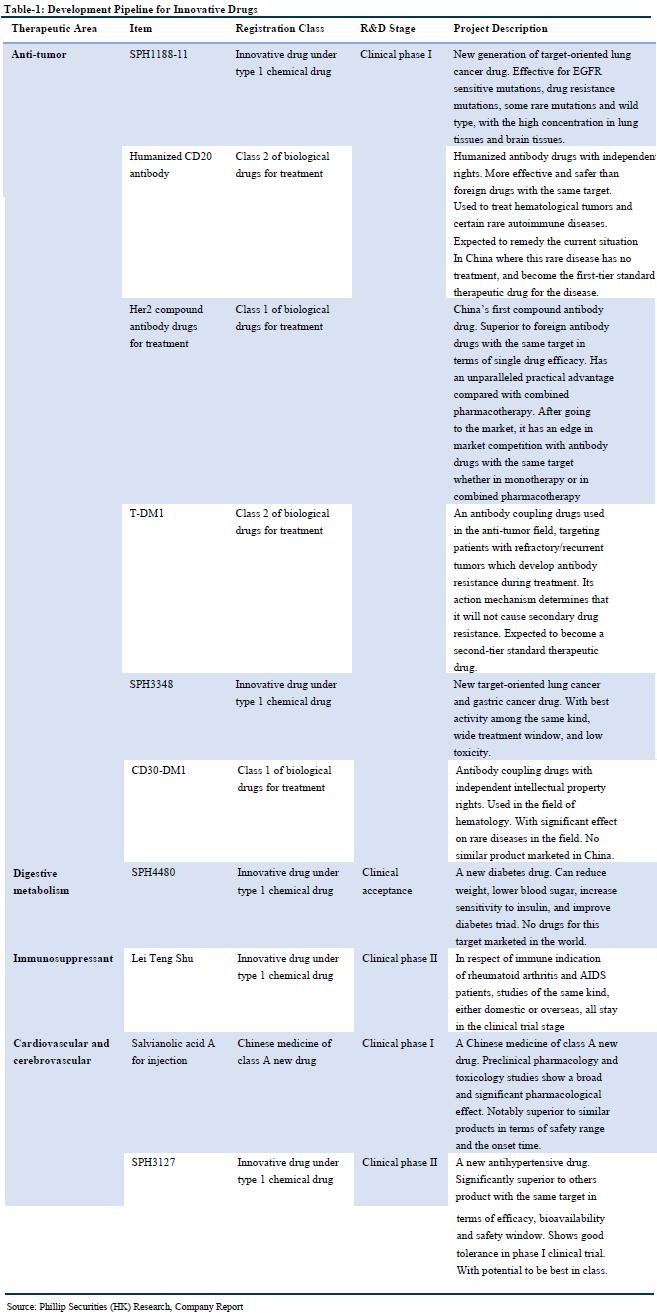

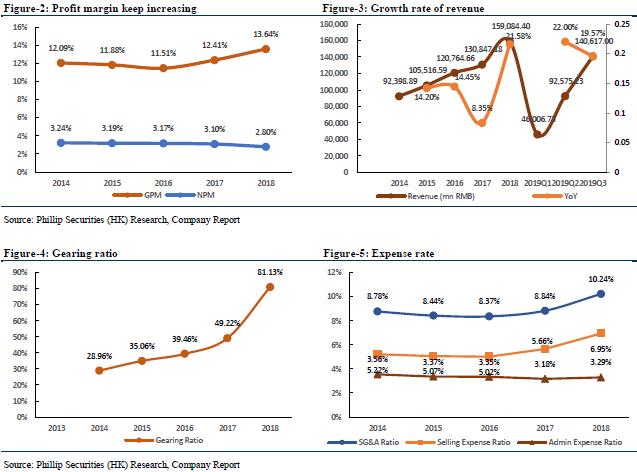

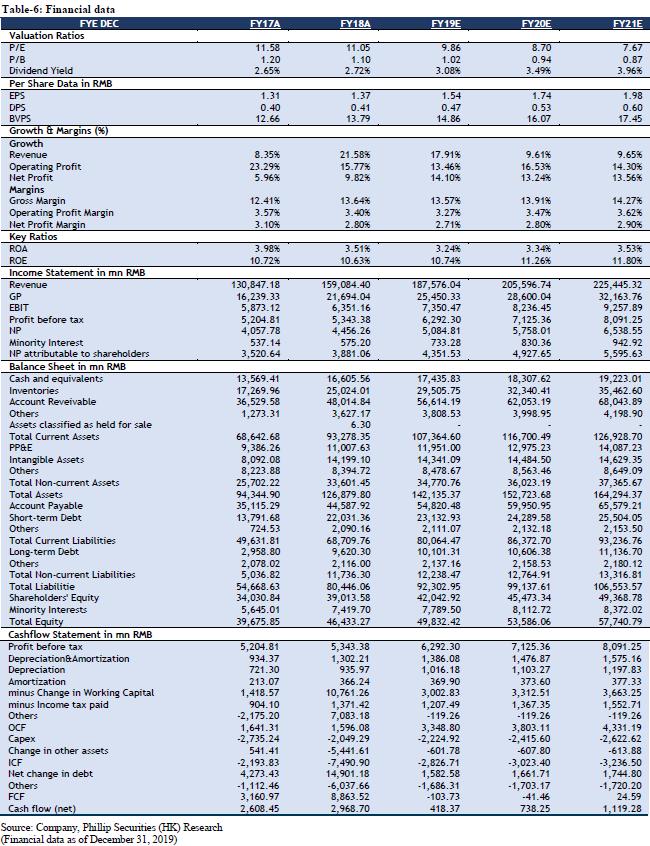

Result UpdateFor the nine months ended September 30, 2019, the company recorded operating income of RMB 146.617 billion, an increase of 19.57% YoY, and its main business continued to grow rapidly. Of which, the pharmaceutical manufacturing sector realized revenue of RMB 17.682 billion, a YoY increase of 24.05%. The pharmaceutical business realized revenue of RMB 129.235 billion, an increase of 18.95% YoY (among which, the pharmaceutical distribution business achieved sales revenue of RMB 121.218 billion, an increase of 18.56% YoY; the pharmaceutical retail business achieved sales revenue of RMB 5.908 billion, an increase of 15.94% YoY). The company realized a net profit attributable to shareholders of listed companies of RMB 3.399 billion, a YoY increase of 0.80%; the main business of the pharmaceutical manufacturing sector contributed a profit of RMB 1.540 billion, a YoY increase of 20.56%; the main business of the pharmaceutical business contributed a profit of RMB 1.526 billion, a YoY increase Increased by 15.73%; the participating companies contributed profits of RMB804 million, an increase of 48.13% YoY. The company's comprehensive gross profit margin was 13.70%, a decrease of 0.11 percentage point compared with the same period last year; the gross profit margin of the pharmaceutical manufacturing sector was 57.54%, a decrease of 0.10 percentage point compared with the same period last year, and the average gross profit margin of 60 key varieties was 71.71%; the gross profit margin of pharmaceutical distribution was 6.40%, a YoY decrease of 0.27 percentage points; the gross profit margin of pharmaceutical retail was 14.10%, a YoY decrease of 1.02 percentage points. Continue to deepen one product one policy, accelerate innovation transformationsIn the pharmaceutical manufacturing sector, the company focuses on key products and continuously increases its market share, such as tanshinone IIA sodium sulfonate injection. From January to September 2019, it realized sales revenue of RMB 1.14 billion, a YoY increase of 76.39%. According to the life cycle of different products, the company has formulated a differentiated terminal strategy, and the promotion effect is significant. In January-September 2019, Ulinastatin for injection achieved sales income of RMB 673 million, a YoY increase of 32.91%; hydroxychloroquine sulfate tablets achieved sales income of RMB 587 million, a YoY increase of 20.56%; Hongyuanda achieved sales income was 366 million yuan, a YoY increase of 31.75%. Eureklin for injection achieved sales of 275 million yuan, a YoY increase of 20.85%. In addition, the company continued to accelerate innovation transformation. From January to September 2019, R & D expenditure was RMB 860 million, an increase of 13.74% YoY; 73 invention patent applications were completed, 24 invention patent authorizations, and 20 utility model authorizations, totaling 117 patents. On September 17, the company signed a joint venture agreement with BIOCAD, the largest biopharmaceutical company in Russia, to introduce adalimumab biosimilars, trastuzumab biosimilars, bevacizumab biosimilars, and PD-1 products. Permanent and exclusive R & D, production, sales and other commercialization rights of the six blockbuster biopharmaceuticals in Greater China, including the joint venture company, will be the sole platform for BIOCAD in Greater China. The company continued to advance the consistency evaluation of the quality and efficacy of generic drugs, further improved the production process and the quality of medicines. As of the end of September, the company has completed more than 40 product specifications for BE testing and application, of which 6 varieties have passed the consistency evaluation. Two varieties of ceftriaxone sodium for injection and lansoprazole for injection have completed a BE test and declared to CDE. Beclometasone propionate inhalation aerosol has been approved for supplementary application, 3 specifications of rosuvastatin calcium tablets have been declared for production, and lenalidomide capsules and rivaroxaban tablets have been completed for BE filing. Capsaicin, a commonly used drug for clinical chemotherapy, has been completed. Tabin has also officially started the BE trial. Pharmaceuticals services continue promoting, expand the terminal marketIn November 2019, the company continued to promote the implementation of new distribution and new retail development strategies, promote the rapid development of advantageous and innovative services, clarify the regional development strategies of key provinces, and continue to promote key provinces such as Guangdong, Shandong, Heilongjiang, Jilin, and Liaoning. The platform construction utilizes the policy opportunities brought by the two-vote system and volume purchase, integrates market resources, and strictly controls the accounts receivable, while quickly seizing the pure-sale terminal market. Among the large varieties, Pfizer's Peer vaccine market has been rapidly expanding, which has led to rapid increase in distribution revenue. During the reporting period, the company achieved 2.122 billion in distribution revenue from vaccine business, a YoY increase of 92.33%. The company has launched a new business, providing efficient and compliant sales channels for imported drugs and new special drugs that are not covered by medical insurance, and after the corresponding products enter the medical insurance, the company's distribution network will be used to provide hospital services. The one-stop service chain of innovative pharmaceutical companies has joined forces to win the general distribution rights for new varieties of large pharmaceuticals.

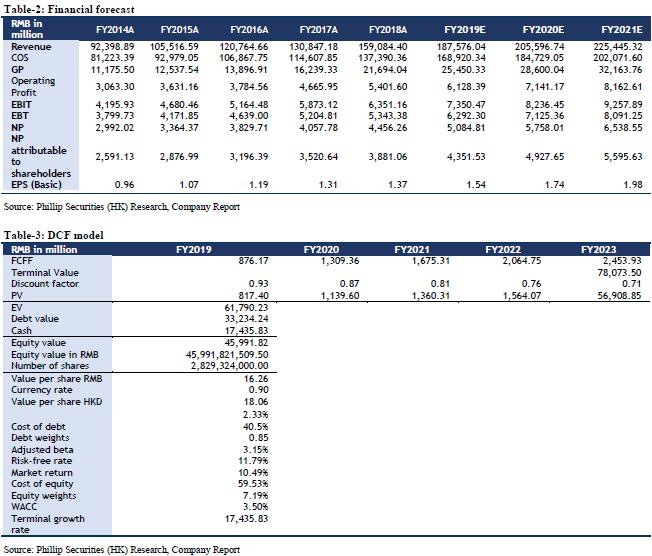

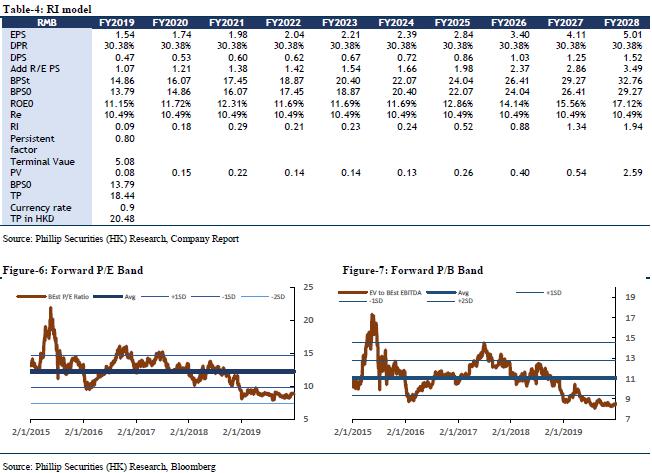

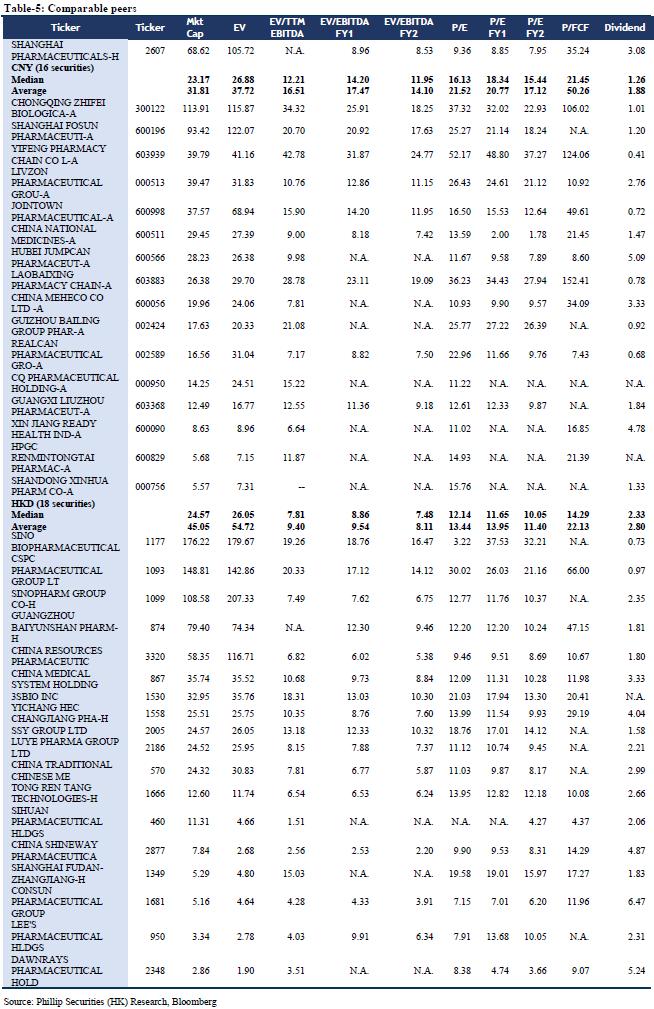

Financial Forecast and ValuationWe forecast that the company's FY19/FY20/FY21 income will be RMB 187.58/205.60/225.44 billion, representing an increase of 17.91%/9.61%/9.65% YoY; net profit attributable to shareholders will be RMB 4.35/4.93/5.60 billion, increasing 12.12%/13.24%/13.56% YoY; corresponding EPS will be RMB 1.54/1.74/1.98. We use DCF model and residual income model to value the company. Assuming equity cost is 10.49%, debt cost is 2.33%, and WACC is 7.19%. We get PT of HKD 18.06 and HKD 20.48 respectively. The lower valuation result corresponds to FY19/FY20/FY21 10.57x/9.33x/8.22x PE, which has an increase of +19.14% compared to the current price (HKD 15.16 as of December 31, 2019), giving an ¡§Accumulate¡¨ rating.

RiskThe launch of new products fails expectations; Industry policy risk. Financials

Click Here for PDF format...

| Recommendation on 7-1-2020 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 15.160 | | Suggested purchase price | N/A | | Target Price | $ 18.060 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2020 Phillip Securities (HK) Ltd. All Rights Reserved.

|