Investment Summary

75% Large Increase in Net Profit in the First Three Quarters

Flat Glass recorded revenue of RMB3,381 million, up 49.71% yoy; net profit attributable to the parent company of RMB508 million, up 75% yoy, equivalent to EPS of RMB0.26, exceeding market expectation. The net profit attributable to the parent company in the first three quarters was RMB109 million, RMB152 million and RMB246 million, respectively; the growth was 11%, 33% and 220% yoy, respectively.

Capacity Expansion upon Industry Recovery

Since Q1 2019, driven by gradual recovery of domestic photovoltaic market, the price of photovoltaic glass increased from bottom. The market price of 3.2mm photovoltaic glass increased by RMB1.5 to RMB2 to RMB28 per square meter, up 8% approximately. Gradual production of capacity expanded by Flat Glass: Two new production lines of 1,000 tons of daily melting volume were put into production in 2017 and 2018, respectively; new production line of 1,000 tons of daily melting volume were put into production in 2019. High cost efficiency upon new production capacity will help the Company to offset the price downward pressure during industry adjust period, and to fully enjoy the price upward benefit upon industry recovery. The Company recorded gross margin of 27.87%, 27.57% and 32.84% in the first three quarters of 2019, respectively, up by -1.45, +1.69 and +10.57 ppts yoy.

The sales expenses in the first three quarters were RMB170 million, up 97% yoy; the administration expenses were RMB81 million, down 5.5% yoy; the financial expenses were RMB38 million, up 681.4% yoy; the R&D expenses were RMB142 million, up 75.68% yoy. The overall period cost rate increased by 1.85 ppts, mainly due to the large increase in sales volume, the overall increase in transportation costs, and the increase in R&D projects.

Continuous Capacity Expansion and Continuous Prosperity of Photovoltaic Industry Expected

The Company will put into production new capacity of photovoltaic grass in the future two years, including two production lines of 1,000 tons per day of Vietnam (expected to be put into production in June 2020 and September 2020), and fourth-tier and fifth-tier production lines of 1,000 tons per day of Anhui Fengyang (expected to be put into production in 2021). The capacity of photovoltaic grass of the Company will achieve 9800 tons per day by the end of 2021, double that of the end of 2018. In terms of industry prosperity, with the implementation of domestic photovoltaic subsidy project, the sustainable and rapid development of overseas photovoltaic market, and gradual increase of proportion of double-glass modules, the high prosperity of photovoltaic glass market is expected to continue. We always believe that the profitability of leading companies with economies of scale and technical capital will be future improved.

Investment Thesis

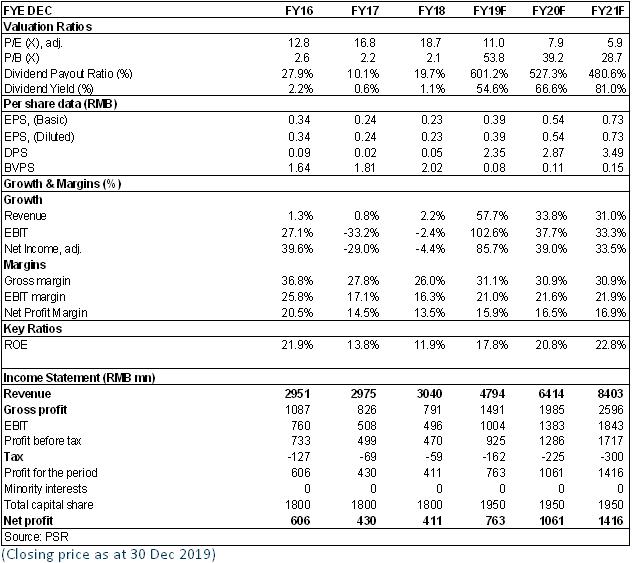

Given the better-than-expected data in report of the first three quarters, we decide to increase profit forecast and target price to HK$5.65 for the Company, equivalent to 2019/2020E 13/9x P/E, Accumulate rating. (Closing price as at 30 Dec 2019)

Financials

Click Here for PDF format...