|

UNI MEDICAL(2666)

Analysis¡G

Genertec Universal Medical Group (2666) continues to carry out its business layout for hospital group on all fronts. Firstly, the Group continuously pushes forward integration and takeover of medical institutions of SOEs. Secondly, the Group steadily integrates the management of cooperating medical institutions to establish a conglomerate management system. Thirdly, the Group continues its hospital investment and construction and solid implementation of its operating projects. To date, the Group`s nationwide medical services network has been gradually established, and an advanced modern hospital group has begun to take shape in China. Regarding its finance and advisory business, the operation results of the Group maintained a steady growth. In the first nine months of 2019, net interest margin and net interest spread both increased as compared to those of 2018, still remaining a leading position in the industry. In the meantime, the Group maintained good assets quality. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $5.70, Target Price: $6.30, Cut Loss Price: $5.40

|

COFCO MEAT(1610)

Analysis¡G

COFCO Meat`s business includes feed production, pig breeding, slaughtering, production and distribution of fresh pork and meat products, and import and sale of frozen meat products. The company is one of the first companies in China to adopt large-scale pig farming. COFCO Meat released the 2019Q3 Operational Express¡G live pig production was 265,000 heads, down 60.4% year-on-year; fresh pork sales were 35,000 tons, down 28.1% year-on-year. Although the amount of live pigs fell sharply, in the third quarter of 2019, the company`s average price of commercial pigs was 22.22 yuan / kg, much higher than the company`s average pork price of 11.41 yuan / kg in the first quarter of this year and the average price of pork in the second quarter of 13.9 yuan. /kg. It is expected that the performance of the company in the third quarter will be significantly better than the first half.

Strategy¡G

Buy-in Price: $2.00, Target Price: $3.00, Cut Loss Price: $1.40

Kobe Bussan Co., Ltd. (3038)

Established in 1981. Carries out the manufacture, wholesale and retail of industrial use foodstuffs, etc. Expands the foodstuff supermarket ¡§Gyomu Super¡¨, which targets industrial-use customers via the franchise method. Also manages ready-made meals and food service chains such as ¡§Kobe Cook World Buffet¡¨, ¡§Green's K¡¨ and ¡§Green's K Teppanyaki Buffet¡¨, etc. as well as renewable energy, etc.For FY2019/10 results announced on 13/12, net sales increased by 12.1% to 299.616 billion yen compared to the previous period, operating income increased by 22.4% to 19.239 billion yen and net income increased by 16.3% to 12.056 billion yen. Company has been working towards reinforcing their domestic group factories and their own import products, etc. and is focusing their efforts on developing PB products. Their PB products being featured in the media have also led to an increase in customers.For its FY2020/10 plan announced together with FY2019/10, net sales is expected to increase by 4.1% to 311.8 billion yen compared to the previous year, operating income to increase by 5.5% to 20.3 billion yen and net income to increase by 10.3% to 13.3 billion yen. Company also newly announced their 3-year plan from FY2020/10 to FY2022/10. FY2022/10 target net sales is at 346.7 billion yen and operating income at 23 billion yen.Target Price : 4,000 yenBuy Price : 3,665 yenCut-Loss : 3,370 yen

|

|

|

Tuopu Group (601689.CH) - Lightweight and Automotive Electronics Business See Opportunities

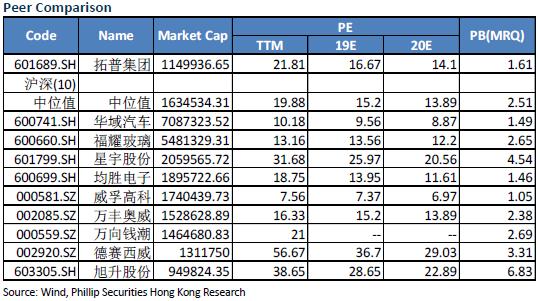

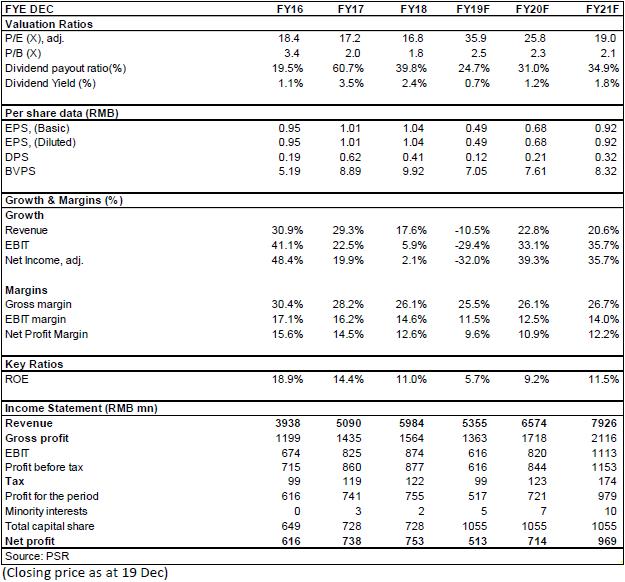

Investment SummaryDecline Slowed in the Third Quarter Tuopu Group recorded a revenue of RMB3766 million in the last three quarters, a 15.50% fall compared with the same period of last year. Among which, Q3 revenue was RMB1328 million, signaling a 3.90% Y-o-Y decrease and a M-o-M increase of 11.30%. Compared with the 25% decrease in the second quarter, the decrease has significantly shrunk. In terms of net profit attributable to the parent company, it was RMB340 million in the last three quarters, decreasing by 30% year-on-year. Among the RMB340 billion, RMB130 million was in the third quarter, which represented a 30% year-on-year decrease and a 30% month-on-month increase. Compared with the same period of last year, gross profit margin and net profit margin down 1.55 and 3.5 ppts, respectively, mainly attributed to the decline in industry prosperity and the increase in depreciation. Recovery of Sales Volume of Major Customers Leads to the Improvement of Capacity Utilization Ratio The improvement in results in the third quarter is resulted from the improved demand from downstream customers. The output of the company's major customers Geely Motor and SAIC GM increased by 9.3% and 3.8%, respectively in the third quarter over the previous quarter. The production of SAIC self and Chang`an Ford also improved compared with the previous quarter, leading to a rebound in the company's capacity utilization. Gross profit margin increased by 0.6 ppts to 26.4% compared with the second quarter, and net profit margin also increased by 1.4 ppts to 9.55% compared with the second quarter. We expect that with the further improvement in sales of major customers in the fourth quarter, the company's profitability will continue to pick up, and net profit growth is expected to be positive. The company continued to reduce costs and increase efficiency in adversity, and the sales, management and R&D expenses accounted for 14.76% of revenue in the third quarter, which fell by 0.92 ppts compared with the second quarter. The company has a good cash flow with a RMB226 million net flow from its operating activities. Inventories fell 12.9% year-on-year to RMB1.14 billion. Lightweight and Automotive Electronics Business See Opportunities for Development The construction of Tesla's Shanghai plant was faster than expected. The trial production began in October and nearly 20,000 vehicles will be produced by the end of the year. As capacity climbs, production will reach 150,000 in 2020 and is expected to exceed 250,000 in 2021. Tuopu supplies Tesla with more than RMB5,000 for each vehicle, and it is estimated that the Model 3 vehicles will bring the company a net profit increment of RMB93 million and RMB180 million in the next two years, respectively, accounting for about 12% and 24% of the company's net profit in 2018. In the field of automotive electronics EVP and IBS, the company's visionary layout brings it a leading position among domestic manufacturers. Tuopu is expected to break through the technological monopoly of foreign giants and realize domestic substitution in the future. Overall, the Company's lightweight chassis and automotive electronics business are in line with the trend of industry upgrading, which will inject momentum into the company's new round of development. Investment ThesisWe estimate that the company's net profit in 2019/2020/2021 will reach RMB513 /714/969 million, respectively, with the corresponding EPS being RMB0.49/0.68/0.92. Although the results in 2019 are under pressure, under the acceleration of Tesla's localization, the company's results will usher in an inflection point and we are optimistic about the development prospects of the company's lightweight business and automotive electronics. So, we lift the Company's target price to RMB19, respectively 26/21 x P/E for 2019/2020/2021, a "Accumulate" rating. (Closing price as at 19 Dec) RiskPrice war among peers Raw material price increase New business risk

Financials

Click Here for PDF format...

| Recommendation on 31-12-2019 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 17.440 | | Suggested purchase price | N/A | | Target Price | $ 19.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|