Investment Summary

Net Profits in the First Three Quarters Increase by near 20%

During the third quarter2019, Weichai Power recorded revenue of RMB35.8billion, down 0.2% yoy; the net profit attributable to the parent company was RMB1.77billion, up 10% yoy. The revenue of the first three quarters was RMB126.7 billion, up 7.3% yoy; the net profit attributable to the parent company was RMB7.06billion, up 17.6% yoy.

The Sales Structure Is Improved and Gross Margin Increases Markedly

The economy of heavy truck industry in China in the first three quarters of this year kept on moving and the growth rate of industry sales volume from the high base reduced by 0.7% yoy, among which the growth rate in the third quarters rebounded to 4%. Sales volume may reach 1.1 million vehicles in this year. The performance of its sales volume and the revenue were better than those of the industry. Due to increasing proportion of large-displacement engine and the smaller proportion of nature gas engine with lower gross margin and other factors, the overall gross margin in the third quarter markedly increased by 1.6 ppts yoy and that in the first three quarters by 0.42 ppts yoy.

Nonetheless, in the headquarters, influenced by the switch of the National VI Emission Standard on natural gas engine, the revenue slightly dipped by 0.2% yoy, putting a drag on the growth of the overall revenue in the third quarter and increasing the cost during the third quarter. The cost in third quarter accounted for 15% in the income, increasing by 1.64 ppts yoy, among which the sales cost rate, administration expenses rate, R&D cost rate increased by 0.48 ppts,0.56 ppts, 0.71 ppts, respectively, and the financial cost rate decreased by 0.12 ppts.

Asset-liability ratio slightly declined by 1.5 ppts to 70.2% compared to the mid-year. The inventory reached RMB21.2 billion, up by RMB130 million yoy, but down by RMB2.6 billion qoq. Value of projects in progress amounted to RMB5.52billion, up RMB1 billion compared to the mid-year. Projects like industrial power engines, Linde Hydraulics Chinese factory and the technology upgrade of the assembly line have been under continuous investment. The company kept on increasing investment on R&D, and the R&D cost increased by 27% yoy.

With the Continuous Development of the Industry, the Company Benefits from the Increase of Market Share

It is expected that the engineering machinery industry will enter the recovery cycle thanks to the rebound of investment growth rate in real estate and infrastructure and increasing demands of weeding out III emission standard vehicles and other preferable factors. However, the stricter environmental regulations and overload punishment will push the industry to reform accordingly. The heavy truck industry is likely to maintain prosperity. Weichai is furthering cooperation with Sinotruk and will benefit from the scale effects brought from increasing market share. From the middle term, the clear strategic framework of ¡§power engine + hydraulics + new energy¡¨ and the access to both the foreign and domestic market cam help the original business to offset the period fluctuation in domestic heavy truck industry and build a more balanced business system.

Investment Thesis

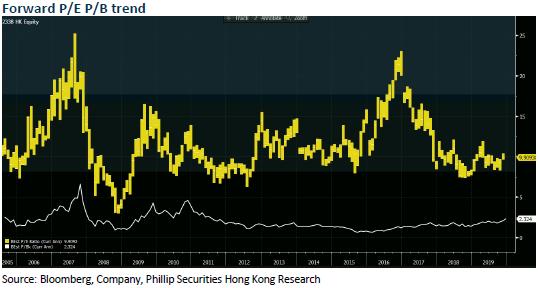

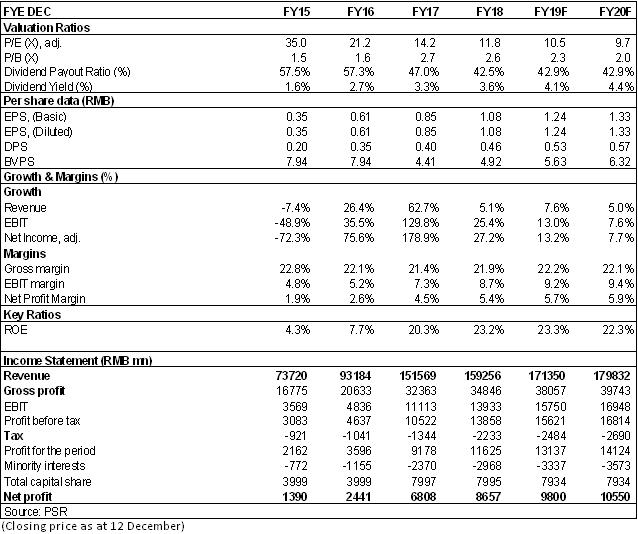

We revise the profit forecast of the company in 2019/2020 to EPS of RMB 1.24/1.33. We will also revise target price to 16.3 HKD (11.7/10.9x for 2019/2020 P/E) and Accumulate rating. (Closing price as at 12 December)

Financials

Click Here for PDF format...