Sectors:

Air & Automobiles (Zhang Jing),

Pharmaceuticals, Technology & Environment (Leon Duan)

Retail & Consumption (Tracy Ku)

Automobile & Air (ZhangJing)

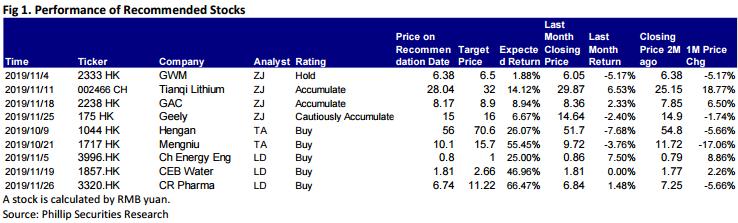

This month I released 4 updated reports of Great Wall Motor(2333.HK), Tianqi Lithium (002466.CH), GAC (2333.HK) and Geely (175.HK), which got success by their unique Competitive edge. Among them, we recommend Tianqi Lithium first.

Currently, the price of lithium carbonate is below RMB60,000 per ton, which is lower than the cost line of many companies. The industry is on the eve of high-cost capacity clearing. On the demand side, the power battery will usher in the peak season in the short term. In the medium and long term, the new European emission standards and the electric vehicle subsidy policy will support the demand for raw material lithium. In general, the future decline of lithium prices is limited, and the upward elasticity will gradually emerge.

As a leading enterprise with high-quality resources, Tianqi Lithium is expected to continue to benefit from the volume and price recovery brought by the acceleration of global electrification by virtue of the technological and scale advantages. The Company's Phase I of lithium hydroxide project of 24,000 tons in Kwinana is expected to enter the continuous production and capacity improvement by the end of the year; the Phase II expansion of Talison has been commissioned. The operation was initiated in an all-round way.Tianqi Lithium not only holds shares of companies with the world's largest scale and best lithium ore resources in production, but also has the world's largest processing capacity on extracting lithium from ores, which make Tianqi Lithium the best investment object in upstream sectors of domestic new energy vehicle industry chains..

Pharmaceuticals, Technology & Environment (Leon Duan)

I released three reports on CN Energy Eng(3996.HK), CEB Water(1857.HK), CR Pharma (3320.HK). We highly recommend CEB Water. For the nine months ended 30 September 2019, the company's revenue was HKD 3.859 billion (corresponding period in 2018: HKD 3.397 billion), representing an increase of 13.61% YoY and 8.3 pts compared with 2019H; among which the revenue of 3QFY2019 was HKD 1.374 billion (corresponding period in 2018: HKD 1.037 billion), representing an increase of 33% YoY, which is slightly lower than our expectation; the increase was mainly attributable to the increase of HKD 193.07 million in construction revenue, HKD 85.85 million in operation revenue, HKD 23.20 million in finance income and HKD 35.47 million in other kind of revenue. The increase in construction revenue was mainly attributable to the construction of river-basin ecological restoration projects in addition to the expansion and upgrading of several waste water treatment plants. The increase in operation revenue was the result of the commencement of operation of new projects and the tariff hikes for several projects effected. The increase in finance income was due to the increase in contract assets. The net profit attributable to shareholders in 9M2019 was HKD 603 million (corresponding period in 2018: HKD 515 million), increase of 17.1% YoY and 3.7 pts compared with 2019H; among which in 3Q2019 was HKD 183 million (corresponding period in 2018: HKD 144 million), representing an increase of 27% YoY. The net profit attributable to shareholders exceed our expectations, which is mainly due to effective control of costs.

As at November 2019, the company has secured Shandong Ji`nan Tangye New Area Waste Water Treatment PPP project, which will be invested in, constructed and operated by a project company jointly established and led by the company based on a PPP (Public-private Partnership) model, with a concession period of 30 years. The company holds a 99.9% stake in the project company. The project has a total designed daily waste water treatment capacity of 45,000 m3, with a total investment of approximately RMB 313 million. Additionally, the company entered into an agreement with the Management Committee of Shandong Zibo Economic Development Zone and secured Zibo Northern Expansion Project. The project will be invested in and constructed based on a BOT (Build-Operate-Transfer) model, with an investment of approximately RMB 83 million for a concession period of 30 years. Its designed daily waste water treatment capacity is 20,000 m3. The waste water treatment capacity remain growing stably, which is expected to enhance businesses through outstanding M&A projects.

Consumption & Retail (Tracy Ku)

This month I released the report of Hengan(1044) and Ausnutria(1717). Ausnutria has announced financial results for the nine months ended 30th September 2019, with revenue increased by 23.9% y.o.y, mainly due to the growth of its own-branded formula goat milk powder and cow milk powder, which increase by 40.3% and 30.6% respectively. The percentage share of own-branded business to total revenue increased by 7.3ppt. y.o.y. to 87.7%. Revenue growth recorded 28.3% y.o.y. during Q3. Nutrition products and private label and others businesses, decreased by 23.1% , as a result of the company's strategy to prioritise more of its resources to better serve its own-branded business.

The gross profit margin during the first nine months and Q3 remained at 52%. The adjusted EBITDA during the first nine months increased by 60.9% y.o.y. The fair value of derivative financial instruments recorded a loss of RMB37.6 million. Net profit increased by 37.1% y.o.y. to RMB624 million, adjusted net profit increased by 67.6% to RMB662 million.

The board of the company has announced that it has resolved to conduct repurchase of shares in the open market from time to time at an initial aggregate consideration of HK$100 million. Depending on market conditions, it may resolve to further increase the scale of the share repurchase as and when considered appropriate.

Short seller Blue Orca has recently published reports about Ausnutria. IRC has been established and engaged the independent consultant to conduct the independent review. According to the first phase report, the customs` records and the company's import records are consistent in all material aspects. The independent consultant further noted that the import volume of goat milk in 2017 as per the customs` records was 154% higher than the annualised import volume as estimated by Blue Orca in the short seller reports. Thus the allegations of exaggerating income and profits are not valid. In addition, the independent consultant did not find any direct evidence that shows the acquisition of 40% of the equity interest in Nutriunion HK was a sham transaction.

According to the second phase of the report, the allegations of the short-selling institutions providing misleading marketing information to consumers are caused by the differences in disclosure requirements in different jurisdictions, the IT deficiency, the translation error and the customer representatives misunderstanding, which do not have a material impact on the description of Kabrita's goat infant formula products. The independent consultant has not identified any evidence supporting Blue Orca's claim that the named distributors were ¡§secretly¡¨ controlled by current or former executive of the company. As for the allegation that the packaging materials and resource consumption published in the ESG report did not increase correspondingly to the growth in infant formula revenue, the independent consultants found that the general trend has been consistent and there is no evidence that the revenue is exaggerated.

Click Here for PDF format...