|

HOPE EDU(1765)

Analysis¡G

In July and August this year, Hope Education Group (1765) successively completed four major acquisitions, including four schools, and its schools expanded from nine to thirteen. Its student enrollment has exceeded 100,000. The student enrollment of the Group as of 20 September 2019 totaled 48,789, representing an increase of 57.26% as compared to the corresponding period in 2018. The Group will conduct screening and analysis on the existing hundreds of potential targets, promote in-depth negotiation of high-quality projects that are coming to fruition as appropriate, to ensure the continuous implementation of merger and acquisition projects. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $1.35, Target Price: $1.47, Cut Loss Price: $1.28

|

COFCO MEAT(1610)

Analysis¡G

COFCO Meat`s business includes feed production, pig breeding, slaughtering, production and distribution of fresh pork and meat products, and import and sale of frozen meat products. The company is one of the first companies in China to adopt large-scale pig farming. COFCO Meat released the 2019Q3 Operational Express¡G live pig production was 265,000 heads, down 60.4% year-on-year; fresh pork sales were 35,000 tons, down 28.1% year-on-year. Although the amount of live pigs fell sharply, in the third quarter of 2019, the company`s average price of commercial pigs was 22.22 yuan / kg, much higher than the company`s average pork price of 11.41 yuan / kg in the first quarter of this year and the average price of pork in the second quarter of 13.9 yuan. /kg. It is expected that the performance of the company in the third quarter will be significantly better than the first half.

Strategy¡G

Buy-in Price: $2.40, Target Price: $3.50, Cut Loss Price: $1.80

|

|

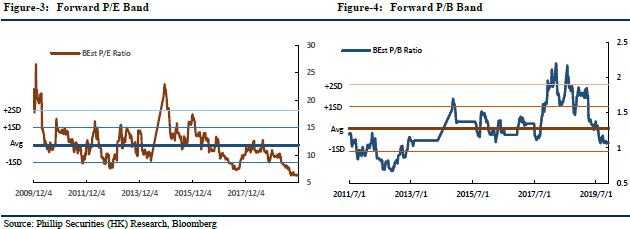

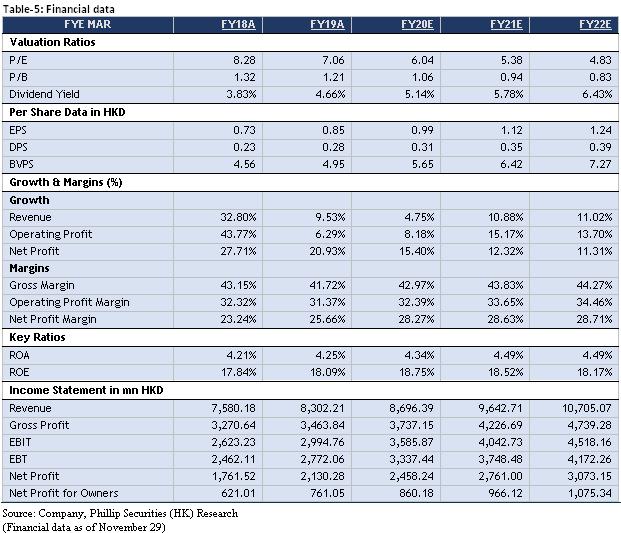

CHINA WATER AFFAIRS (855.HK) - 1H20 performance roughly in line with expectations, core business continues to develop

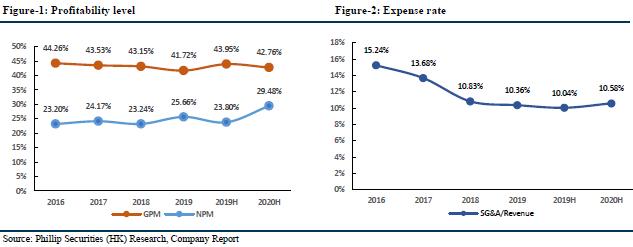

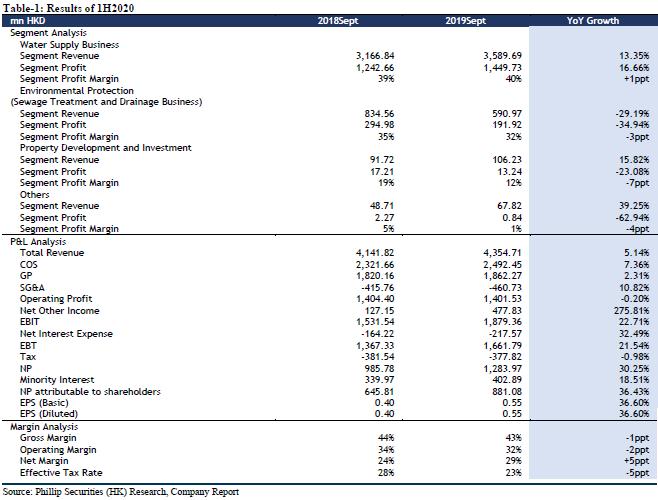

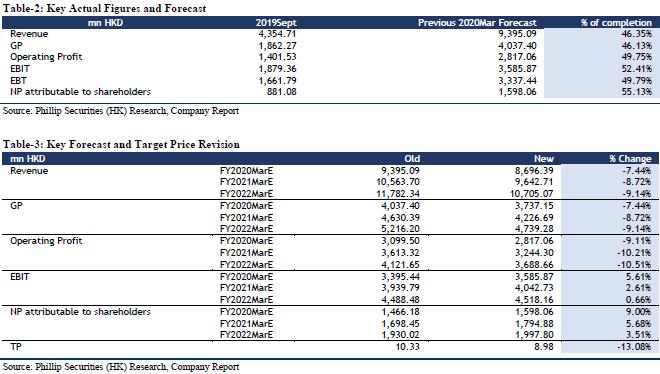

Result UpdateFor the six months ended 30 September 2019, the company recorded a revenue of HKD 4,355 million, representing a steady increase of 5.14% YoY. Gross profit was HKD 1,862 million, representing an increase of 2.31% YoY. Gross profit margin was 42.76%, representing a decrease of 1.19 ppts. Profit attributable to owners of the company was HKD 881million, representing a significant increase of 36.4% YoY. The interim dividend of the company was HK 14 cents per share, representing a steady increase of 16.7% YoY. It was mainly attributable to the successful strategy of the company through procurement of more construction and connection work, increase in operating efficiency and tariff of the water supply and sewage treatment plants and various mergers and acquisition. According to segments, the revenue from city water supply operation and construction segment amounted to HKD 3,590 million, representing a steady increase of 13.35% YoY, which represented approximately 82.4% of the total revenue, increasing 5.9 ppts; amongst which the revenue contributed from water supply operation services and water supply connection income was HKD 2,010 million, representing a steady increase of 10.46% YoY; revenue contributed from water supply construction services was HKD 1,537 million, representing a steady increase of 18.24% YoY. The city water supply segment profit amounted to HKD 1,450 million, representing a steady increase of 16.66% YoY; segment profit margin was 40.39%, representing an increase of 1.15 ppts. The increase of the performance of the city water supply segment was mainly due to increase in volume of water sold, procurement of more construction and connection work driven by the continuation of urban-rural integration and the promotion of the Public-Private Partnership model in the water sector and the additional contribution from the new water projects. The revenue from environmental protection segment amounted to HKD 591 million, representing a significant decrease of 29.19% YoY, which represented approximately 13.6% of the total revenue, decrease of 6.5 ppts; amongst which the revenue contributed from sewage treatment and drainage operation services was HKD 174.4 million, representing a steady increase of 18.6% YoY; revenue contributed from sewage treatment and water environmental renovation construction services was HKD 351.8 million, representing a significant decrease of 46.3% YoY. The environmental protection segment profit amounted to HKD 192 million, representing a significant decrease of 34.9% YoY; segment profit margin was 32.48%, representing a decrease of 2.87 ppts. The decrease was mainly due to the decrease in the work for upgrade of facilities for higher operating standard and water environmental renovation construction services. Focus on core business, promising in direct drinking businessThe core business of the company maintained stable development. The revenue from water supply business was 3.59 billion HKD, which increased by 17.4% year-on-year excluding the impact of fluctuations in RMB. The CAGR of the company's water supply business in the past 6 years has reached 20% to 30%. Rising prices and volumes brought stable growth to the company. As of September 2019, the company's comprehensive daily capacity was 14.81 million tons/day, of which the existing capacity was 8.92 million tons/day, 2.08 million tons/day under construction and 3.81 million tons/day planned. The increasing water supply capacity from M&A is 130,000 tons/day, and the organic growth water supply capacity is 165,000 tons/day. After the period, the newly acquired water supply capacity was 231,000 tons/day, and there will be multiple expansion projects. Regarding the increase in water price, the price of tap water in Jingzhou, Jiangling and Anxiang has been significantly increased, and the treatment price of four sewage treatment projects including Wannian and Fenyi have also been increased. The number of water supply units increased by 700,000, exceeding 5.4 million in total. In addition, the company cashed out 240 million HKD by disposing of non-core assets to further strengthen the development of its main business. It is expected that the disposable non-core assets will exceed 500 million HKD in the near future. In terms of direct drinking water business, in February 2019, the company with Orix and Toray formed Jiangxi Yinli Direct Drinking Water Equipment Co., Ltd. to actively expand the direct drinking water business. During the period, the company added more than 140 direct drinking water projects and realized revenue of 27.27 million HKD, of which water sales income was 5.68 million HKD and connection income was 17.05 million HKD. As of September, the total population of direct drinking water services was close to 500,000. We believe that the company focuses on the development of core water supply business, and develops two core strategies around the integration of urban and rural water supply and supply and drainage integration. It promotes the growth of its main business through acquisition of high-quality projects and upgrading of existing projects. At the same time, it will accelerate the expansion of value-added services such as secondary water supply and direct drinking water, and pilot intelligent water services to deploy an intelligent pipe network system to seize future strong performance growth points. Re-affirm ¡§BUY¡¨ Investing RatingWe adjusted the TP of HKD 8.98, corresponding to FY20/FY21/FY22 9.03x/8.04x/7.22x PE with a +49.40% potential upside compared with CP of HKD 6.01 as of November 29, 2019, we maintain ¡§BUY¡¨ investment rating.

RiskCapacity increase fail expectations; Industry policy; M&A fails expectations. �Financials

Click Here for PDF format...

| Recommendation on 3-12-2019 | | Recommendation | BUY | | Price on Recommendation Date | $ 6.010 | | Suggested purchase price | N/A | | Target Price | $ 8.980 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|