|

|

FOSUN TOURISM(1992)

Analysis¡G

It is the largest leisure tourism resorts group worldwide in terms of revenue in 2018. It operates through Club Med and Club Med Joyview resorts. Its principal activities also include tourism destinations, which it develops, operates and manages, as well as destinations it manages for other parties, services and solutions in various tourism and leisure settings. It currently owns Atlantis Sanya, and have started the design of the Lijiang and Taicang projects. In the first half of the year, the revenue in the first half of the year increased by 35.9% to RMB9.062 billion, and recorded a profit of RMB490 million. Last year, it recorded a loss of RMB254 million. Interim dividend of HK$0.07 per share. Revenue of the global tourism market increased at a CAGR of 4.9% from 2013 to 2017 and is expected to grow at a CAGR of 7.9% until 2022. The global leisure tourism market grew at a CAGR of 5.7% and is expected to grow at CAGR of 8.8% until 2022.

Strategy¡G

Buy-in Price: $9.76, Target Price: $12.00, Cut Loss Price: $8.00

Itochu Corp (8001)

A major general trading company founded in 1858 by Itoh Chubei. Has 110 bases in 63 countries / regions throughout the world. Engages in a wide range of businesses, including domestic trading, import/export, and overseas trading of various products such as textile, machinery, metals, energy, chemicals, food, general products, information technology, and finance, as well as business investment in Japan and overseas.For 1H (Apr-Sept) results of FY2020/3 announced on 1/11, revenue increased by 0.5% to 5,489.699 billion yen compared to the same period the previous year, operating income increased by 35.3% to 222.639 billion yen, and net income increased by 12.0% to 289.068 billion yen. The metal business increased its profits due to rising iron ore prices and dividends received from Brazil Japan Iron Ore Corp. There was also an improvement due to the absence of the impairment loss on investment in CITIC in the same period the previous year.For its full year plan, current income is expected to decrease by 0.1% to 500.0 billion yen compared to the previous year. Details announced on 26/4 remain unchanged. The profit ratio of non-resource business in 1H fell from 84% in the same period the previous year to 78% due to an increase in profit in the metal business. However non-resource profits achieved a record high of 224.9 billion yen. Domestic consumption-related business may continue to be a driving force.Target Price : 2,550 yenBuy Price : 2,360 yenCut-Loss : 2,200 yen

|

|

|

CR PHARMA (3320.HK) - Develop Segments Cooperation, Improve Business Synergy

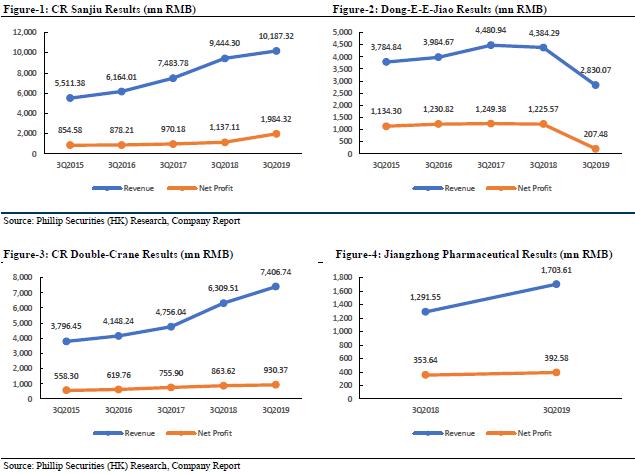

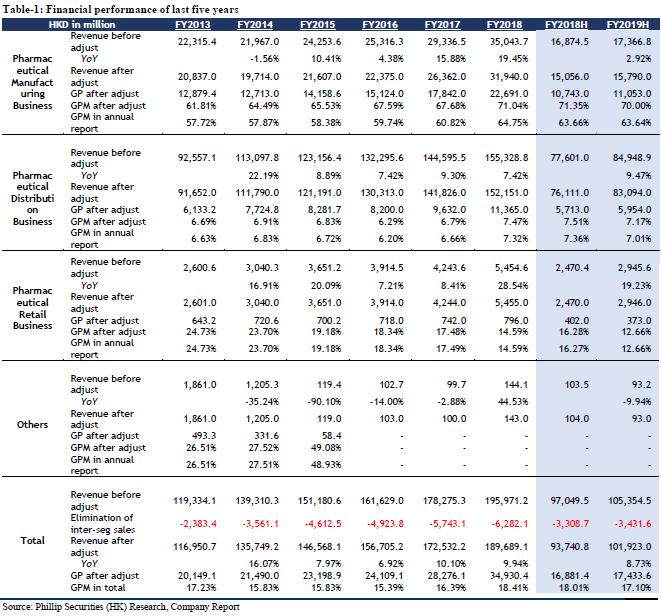

Subsidiaries Maintained Growth in 3Q2019For the nine months ended September 30, 2019, the operating revenue of CR Pharmaceutical Holdings, a wholly-owned subsidiary of the company, was RMB 135.022 billion (3Q2018: RMB 116.795 billion), representing an increase of 15.6% YoY; the net profit attributable to shareholders was RMB 2.465 billion (3Q2018: RMB 1.804 billion), a YoY increase of 36.6%. For the nine months ended September 30, 2019, the revenue of Dong-E-E-Jiao, a subsidiary of the company, was RMB 2.83 billion (3Q2018: RMB 4.394 billion), a YoY decrease of 35.59%; the net profit was RMB 207 million (3Q2018: RMB 1.226 billion), a YoY decrease of 83.12%. The revenue of CR Sanjiu, a subsidiary of the company, was RMB 10.187 billion (3Q2018: RMB 9.444 billion), a YoY increase of 7.87%; the net profit was RMB 1.984 billion (3Q2018: RMB 1.137 billion), a YoY increase of 74.49%; based on preliminary assessment by the management of CR Sanjiu, the unaudited net profit attributable to the shareholders of CR Sanjiu for the year ended 31 December 2019 are estimated to be RMB 2.11 to 2.25 billion (FY2018: RMB 1.432 billion), an expected increase of 47.34% to 57.11% YoY; the significant increase in the net profit attributable to the shareholders is primarily attributable to the completion of disposal of its 82.89% equity interest in Shenzhen Sanjiu Hospital Co., Ltd. in January 2019, resulting in a net gain (after tax) of approximately RMB 680 million to CR Sanjiu. The revenue of CR Double-Crane, a subsidiary of the company, was RMB 7.407 billion (3Q2018: RMB 6.31 billion), a YoY increase of 17.39%; the net profit was RMB 930 million (3Q2018: RMB 864 million), a YoY increase of 7.64%. The revenue of Jiangzhong Pharmaceutical, a subsidiary of the company, was RMB 1.704 billion (3Q2018: RMB 1.292 billion), a YoY increase of 31.89%; the net profit was RMB 393 million (3Q2018: RMB 354 million), a YoY increase of 11.02%. In general, apart from Dong-E-E-Jiao, the performance of the company's subsidiaries has maintained steady growth, and with the gradual progress of Dong-E-E-Jiao, we are still optimistic about the company's performance as the industry leader in the future. Continue to Increase and Optimize Product portfolio in the Pharmaceutical SectorRecently, the company pointed out that it will use the channel advantage in the pharmaceutical sector to continuously increase and optimize its product portfolio in "CICC Forum 2019". The manufacturing business of the company encompasses the research and development, manufacturing and sale of pharmaceutical products. The company manufactured more than 540 products in 1H2019, of which morethan 300 were included in NRDL. The products comprise chemical drugs, Chinese medicines and biopharmaceutical drugs as well as nutritional and healthcare products, covering a wide range of therapeutic areas including cardiovascular, alimentary tract and metabolism, large-volume IV infusion, pediatrics, respiratory system etc.. The company had approximately 200 R&D projects in the pipeline, including 45 projects in the pipeline on innovative drugs. In addition, on October 3, 2019, NIP292, an innovative drug developed by the China Pharmaceutical Research and Development Center directly under the company's research and development platform, was approved by the US Food and Drug Administration (FDA) clinical trial and conducted a phase I clinical trial in the United States. NIP292 is primary treatment of pulmonary fibrosis (IPF), it is a new small molecule drug with multiple functions such as anti-inflammatory, anti-fibrosis, dilation of blood vessels, and repair of vascular endothelial injury. In addition to IPF, NIP292 has great potential for the treatment of autoimmune diseases, other fibrotic diseases, and malignant tumors. On October 23, CR Sanjiu, a subsidiary of the company, and Japan's Takeda Consumer Health Co., Ltd. signed an ALINAMIN product cooperation agreement in Beijing. CR Sanjiu will be responsible for the commercialization and sales of ALINAMIN in the Chinese market, and the two sides will also reach a consensus on other product portfolios and cross-border e-commerce business in the future. The company continues to improve R&D capability, enrich pipeline and access to products, and forge advantages of brand clustering, which is believed to benefit future development. Market Share of the Circulation Sector is Expected to Further Increase As at the end of 1H2019, distribution network of the company covered 28 provinces, reached 141 cities in total, serving over 100,000 downstream customers, including 6,862 Class II & III hospitals, and 53,640 primary medical institutions competitiveness in the Eastern China. The company continuously enhanced efficiency of the integrated and modernized intelligent logistics system, as at the end of 1H2019, the company operated 185 logistics centers in total. The company enhanced capability in providing value-added services to downstream customers, provided Hospital Logistic Intelligence (HLI) services to over 300 hospitals, and commenced Network Hospital Logistics Intelligence (NHLI) projects. In 1H2019, the company operated 842 retail pharmacies, of which 150 are DTP pharmacies covering 76 cities nationwide. The company continues to deepen the layout of pharmaceutical circulation sector, and enhances strength of the company through endogenous expansion and outreach acquisition, its market share is expected to further increase.

Maintain "BUY" RatingWe maintain the expected EPS of HKD 0.75/0.83/0.90. The target price was HKD 11.22, corresponding to FY19/FY20/FY21 14.95x/13.51x/12.48x PE, which was +66.51% higher than the current price (HKD 6.74 as of November 22, 2019), maintaining a ¡§BUY¡¨ rating. RiskIndustry policy risk; M&A fails expectations. Financials

Click Here for PDF format...

| Recommendation on 26-11-2019 | | Recommendation | BUY | | Price on Recommendation Date | $ 6.740 | | Suggested purchase price | N/A | | Target Price | $ 11.220 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|