Investment Summary

Wholesale Sales Volume Stopped Falling in October yoy

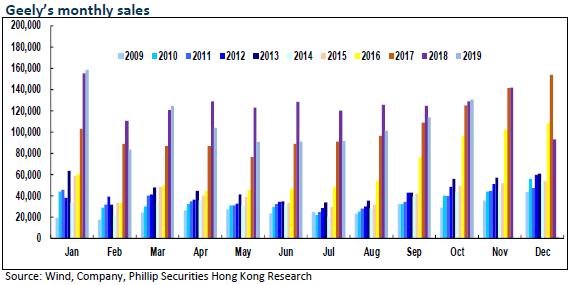

In October, the wholesale sales volume of Geely reached 130,000 units, up 1% yoy. The overseas sales volume of the sub-market was 2,986 units, up 123% yoy; the domestic sales volume was 127,000, down 0.4% yoy, a sharp decrease compared with 9% last month. From January to October this year, the total sales volume of Geely was 1,088,290, down 14% from 1,265,844 units in the same period last year, reaching 80% of the annual sales target of 1.36 million units. In view of this year's peak season ahead of schedule and the usual year-end sales promotion of the car companies, we believe that the company is quite sure to achieve the annual goal.

Compared with the previous month, sales volume of Geely in October continued the recovery trend since June, up 14% mom. Among them, overseas sales rose 11% mom, while domestic sales rose 14% mom.

The trend of product mix upgrading continued with the newly-launched models grow steadily

Influenced by the slowdown of market growth and other factors, many models of Geely have seen a year-on-year decline in sales, but still rank good in peers. The Company sold more than 10,000 units per month for five models, and the upgrading trend of the product line continues. Compared with the same period last year, sales growth mainly comes from new models BinYue/LYNK03/ Jihe/JiaJi/XingYue (+23,636 units yoy), and old models BoYue/Vision X3 (+1,725 units). BoYue, which has widened its price range with its new model Bo Yue pro, has saw more than 20,000 units again for two consecutive months.

The sales decrease mainly comes from DihaoGL/ Vision sedan/LYNK0102/ Vision SUV/ BoRui/ Dihao (-26,213 units): the sharp decline in sales volume of DihaoGL is mainly caused by the sales diversion of BinRui, which has the similar positioning to DihaoGL, and the total share is not reduced. The larger decline in Vision sedan is due to the older models and the price reduction of competitors.

Benefited from the sinking of channels, the short-term old models improved significantly on a month on month basis

Compared with last month, the new models BinRui and BinYue grew faster (+ 3,328 units mom). It is worth noting that the old models including Vision SUV/Vision X3/Dihao/ DihaoGS have contributed to the main mom increase (+10,777 units). We believe that the main reasons are as follows: 1) the sinking of channels and the recovery of demand in tier 3, 4 and 5 cities. 2) benefited from the launch of Dihao GSe, although it is diversified by BinYue, DihaoGS still leads the sales trend of crossover SUV for domestic selfbrands; 3) the bottleneck problem of the production capacity of the Luqiao Factory for Vision X3 has been solved.

Unlike the past, the Company is cautious in stock, and the inventory of dealers is maintained at a healthy level of about 1.5 to 2 months.

Integration of engine business and platform strategy will help to further reduce costs and increase efficiency

The Company plans to merge its engine business with Volvo as an independent business sector, focusing on fuel and hybrid power, while providing engines and hybrid power systems for Volvo, Geely, Proton, Lotus, London electric vehicles and LYNK & Co to enhance the technical competitiveness of the Company's products. Volvo Auto China will focus on the R&D of electric products, with a clearer division of research and development, and the scale effect will be further improved.Between the end of the year and the first half of next year, Geely is expected to release 5-6 new models, including the new SUV "ICON" from the BMA platform, the LYNK & CO 04/05 from the CMA platform, the Preface sedan, the second geometric series model from the PMA platform, and the business MPV model VF12.It is expected that with the launch of more new modular platform products, the R & D and production costs will be greatly reduced.

Investment Thesis

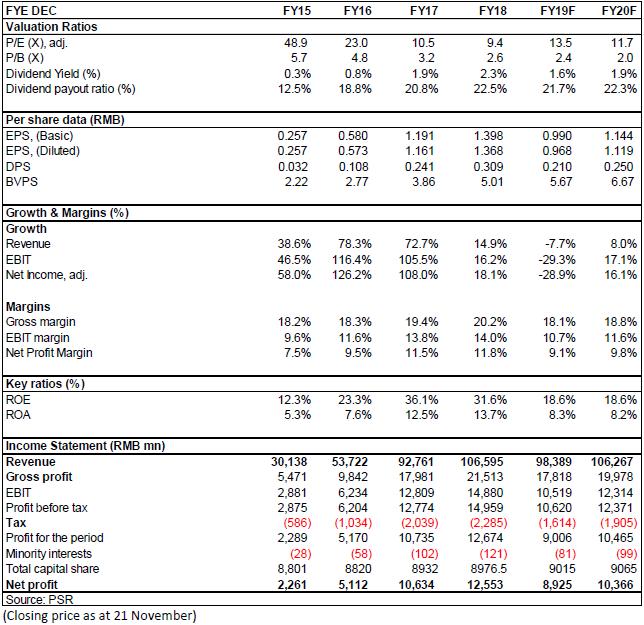

We think the current domestic car market has obvious signs of slow recovery, but the fierce price competition in the car market will still be the main pressure affecting the profitability of car companies in the future. As the leader of the self-owned brands, Geely Auto has strong advantages in cost control, model development and other aspects. We adjusted the Company's valuation multiple to reflect the improvement in sentiment after the car market trough. We revised our target price to HK$16, equivalent to 14.4/12.5 P/E ratio in 2019/2020, and we give the rating of Cautiously Accumulate. (Closing price as at 21 November)

Financials

Click Here for PDF format...