|

|

Q TECH(1478)

Analysis¡G

Q Tech record a consolidated profit attributable to the Shareholders of RMB181 million for the six months ended 30 June 2019, as compared to a loss of RMB51.29 million over a year ago, due to the following factors: (i) the gross profit margin of overall products improved apparently due to a significant increase of sales volumes of camera modules and the enhancement of product mix of fingerprint recognition module products; (ii) the labour cost has improved, which was mainly attributable to the upgrading of the production automation that has gradually demonstrated results; and (iii) Newmax Technology Co., Ltd., an associated company of the Company, has significantly improved its managing situation for the period from January 2019 to April 2019 and has recorded a profit. The gross profit margin of the integrated products increased significantly compared with the same period of last year, increasing by 7pcts to 8.2% year-on-year, and the net profit margin increased by 5.2pcts to 3.6%. In the second half of the year, driven by customer demand and product structure upgrades, profit growth is expected to continue to maintain high speed.

Strategy¡G

Buy-in Price: $11.00, Target Price: $14.00, Cut Loss Price: $9.00

Toyota Motor Corp (7203)

Established in 1937. Conducts financial and other businesses even while focusing on the automotive business. Besides providing cars such as sedans, minivans, 2BOX, SUVs, trucks, etc, and related components and supplies, also offers automotive sales financing and housing, pleasure boats, etc. Group companies include Hino Motors (7205) and Daihatsu Motor.For 1H (Apr-Sept) results of FY2020/3 announced on 7/11, net sales increased by 4.2% to 15,285.595 billion yen compared to the same period the previous year, operating income increased by 11.3% to 1,404.336 billion yen, and net income increased by 2.6% to 1,274.976 billion yen. Vehicles sold increased by 220,000 units to 4.639 million units. Sales of new models for RAV4 and Corolla were strong. Cost improvement initiatives had also contributed.For its full year plan, net sales is expected to decrease by 2.4% to 29,500.0 billion yen compared to the previous year, and current income to increase by 14.2% to 2,150.0 billion yen. Sales forecast is 8.95 million units, a reduction of 50,000 units from the original plan. The decline in Asia due to the worsening markets in India and Indonesia will impact results, but Japan and other countries with strong markets will see increase in sales.Target Price : 8,110 yenBuy Price : 7,600 yenCut-Loss : 7,240 yen

|

|

|

CEB WATER (1857.HK) - Results of 3Q2019 in Line, M&A Projects Enhance Businesses

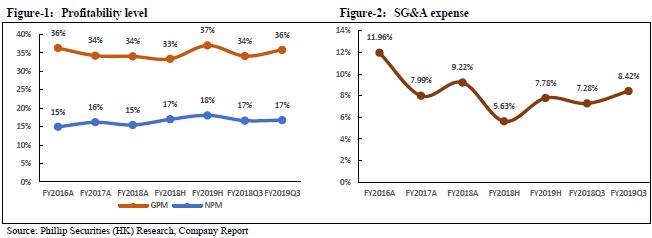

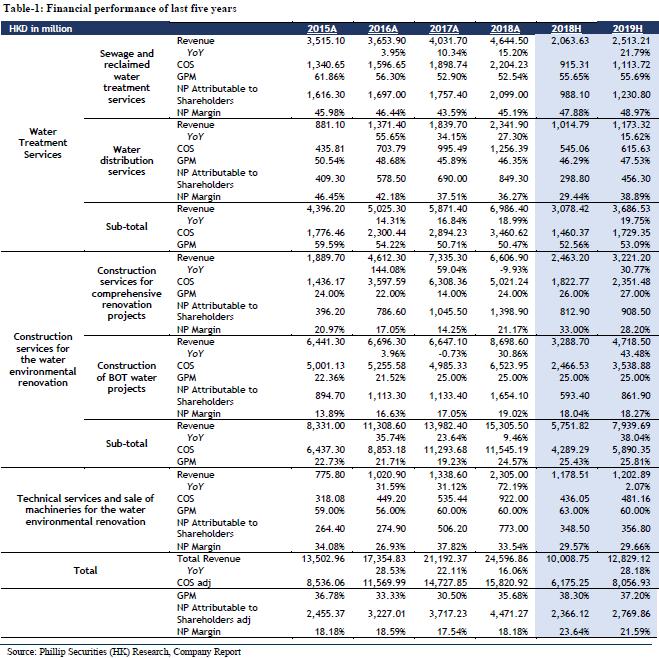

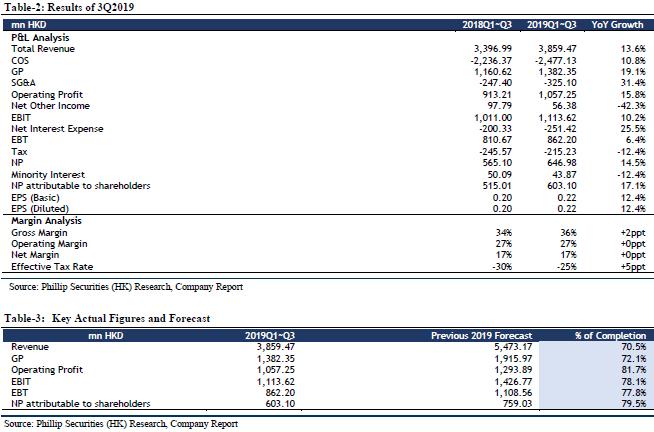

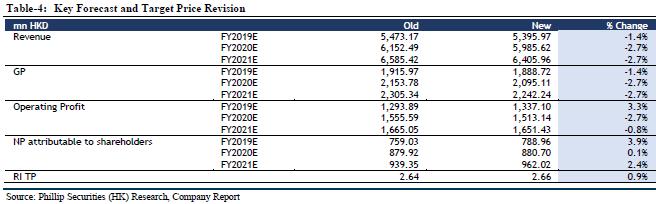

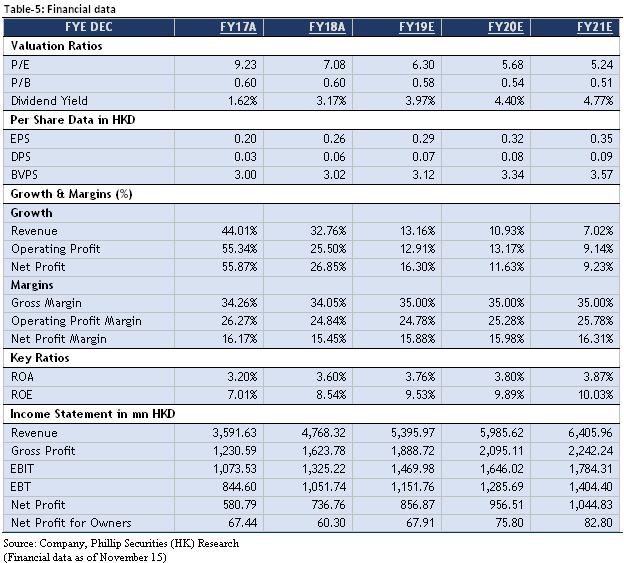

Company UpdateFor the nine months ended 30 September 2019, the company's revenue was HKD 3.859 billion (corresponding period in 2018: HKD 3.397 billion), representing an increase of 13.61% YoY and 8.3 pts compared with 2019H; among which the revenue of 3QFY2019 was HKD 1.374 billion (corresponding period in 2018: HKD 1.037 billion), representing an increase of 33% YoY, which is slightly lower than our expectation; the increase was mainly attributable to the increase of HKD 193.07 million in construction revenue, HKD 85.85 million in operation revenue, HKD 23.20 million in finance income and HKD 35.47 million in other kind of revenue. The increase in construction revenue was mainly attributable to the construction of river-basin ecological restoration projects in addition to the expansion and upgrading of several waste water treatment plants. The increase in operation revenue was the result of the commencement of operation of new projects and the tariff hikes for several projects effected. The increase in finance income was due to the increase in contract assets. The gross profit was HKD 1.382 billion (corresponding period in 2018: HKD 1.161 billion), representing an increase of 19.1% YoY and 2.3 pts compared with 2019H; among which the gross profit of 3Q2019 was HKD 462 million (corresponding period in 2018: HKD 373 million), representing an increase of 24% YoY. Direct costs and operating expenses in 3Q2019 was HKD 911.84 million (corresponding period in 2018: HKD 663.93 million), representing an increase of 37% YoY; the increase was mainly due to the increase in construction cost arising from the increased construction services, which contributed to a construction revenue of HKD 684.78 million in 3Q2019 as compared to HKD 491.71 million in 3Q2018. The GP margin was in 3Q2019 decreased to 34% (corresponding period in 2018: 36%), it was mainly due to a slightly larger proportion of construction revenue recognized in the mix of the total revenue of 3Q2019 as compared with 3Q2018; construction revenue comprised approximately 57% of total revenue in 3Q2019 (corresponding period in 2018: 54%). The net profit attributable to shareholders in 9M2019 was HKD 603 million (corresponding period in 2018: HKD 515 million), increase of 17.1% YoY and 3.7 pts compared with 2019H; among which in 3Q2019 was HKD 183 million (corresponding period in 2018: HKD 144 million), representing an increase of 27% YoY. The net profit attributable to shareholders exceed our expectations, which is mainly due to effective control of costs. Secures two waste water treatment projects in Shandong province, stable growth in production capacityAs at November 2019, the company has secured Shandong Ji`nan Tangye New Area Waste Water Treatment PPP project, which will be invested in, constructed and operated by a project company jointlyestablished and led by the company based on a PPP (Public-private Partnership) model, with a concession period of 30 years. The company holds a 99.9% stake in the project company. The project has a total designed daily waste water treatment capacity of 45,000 m3, with a total investment of approximately RMB 313 million. Additionally, the company entered into an agreement with the Management Committee of Shandong Zibo Economic Development Zone and secured Zibo Northern Expansion Project. The project will be invested in and constructed based on a BOT (Build-Operate-Transfer) model, with an investment of approximately RMB 83 million for a concession period of 30 years. Its designed daily waste water treatment capacity is 20,000 m3. The waste water treatment capacity remain growing stably, which is expected to enhance businesses through outstanding M&A projects. Maintain "BUY" Rating We adjusted our forecast for FY19/FY20/FY21 incomes to HKD 5.396/5.986/6.406 billion, showing increases of 13.16%/10.93%/7.02% YoY; net profit attributable to shareholders were HKD 789/881/962 million, with increase of 16.63%/11.63%/9.23% YoY; the corresponding EPS was HKD 0.2874/0.3185/0.3453. The target price was adjusted to HKD 2.66, corresponding to FY19/FY20/FY21 9.26x/8.35x/7.70x PE, which was +46.98% higher than the current price (HKD 1.81 as of November 15, 2019), maintaining a ¡§BUY¡¨ rating.

RiskProject progress fail expectations; Industry policy; M&A fails expectations. �Financials

Click Here for PDF format...

| Recommendation on 21-11-2019 | | Recommendation | BUY | | Price on Recommendation Date | $ 1.810 | | Suggested purchase price | N/A | | Target Price | $ 2.660 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|