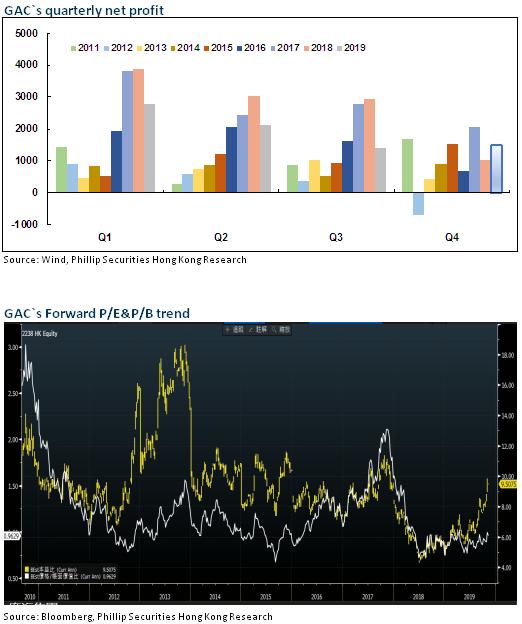

50% Decrease in Result in the Third Quarter

In Q3 2019, GAC recorded operating revenue of RMB14,561 million, down by 9.65% yoy; the net profit attributable to the parent company was RMB1,416 million, down by 52% yoy, and down by 34% qoq. During the first three quarters, GAC recorded operating revenue of RMB42,684 million, down by 19.2% yoy; the net profit attributable to the parent company was RMB6,335 million, down by 35.75% yoy. The decrease in result in Q3 was higher than that of Q1 and Q2by 29% and 30%, respectively.

Profitability Affected by De-inventory under Transformation of Emission Standards

The gross margin in Q3 was 6.1%, down by 12.5 ppts yoy, mainly due to the bigger promotion to clear the inventory of China V vehicles, the sharp decline of Trumpchi SUV affected by depression of domestic SUV market, as well as the loss of new energy vehicles business at the picking-up period. In Q3, the sales of Trumpchi was 90,000 units, down by 28.6% yoy, and worse than the average level of the industry. The Company strictly controlled the expenses. The sales/administration/financial expenses ratio decreased by 0.4 ppts to 11.43%, totalling RMB1.68 billion. Due to the large investment into new vehicles and new platforms, the R&D expenses increased by 100% to RMB0.38 billion.

Japanese Brands Exceed Expectation and American Brands are Weak, with the Same Return on Investment

The sales volume of GAC Toyota in Q3 was 185,000 units, up by 11.1% yoy; the sales volume of GAC Hongda was 179,000 units, down by 1.6% yoy; the sales momentum of hot models like Camry/Highlander/Accord was well. The sales volume of GAC Mitsubishi Motors increased by 3% yoy, and the sales volume of GAC FCA decreased by 39% yoy, but rebounded by 7% and 17% compared with Q2, respectively. The investment gain was RMB2.55 billion, down by 0.4% yoy, and up by 6.6% qoq.

The Upgrade of Self-owned Brands start again

The brand image and product reputation of Trumpchi of GAC have been established during ten yeas of development. Under the decline pressure of the economy, the domestic passenger vehicle market, especially the self-owned brands, will be increasingly difficult to continue the previous high growth. In order to adapt the competition of the vehicle market in the adjustment period in the next two or three years, the Management of the Company will make preparations and integrate resources to improve the competitiveness of Trumpchi from the following aspects: 1) focusing on the reliable quality and design of products, 2) strengthening the integration and linkage of R&D and production, 3) speeding up the construction of intelligent internet connection and new energy technology system, 4) improving the sales system comprehensively, 5) promoting the reform of professional manager and mixed ownership. The sales volume of new energy strategic model AionS was 14,000 units as of the end of September, with orders for 50,000 units in hand; in October, new vehicle AionLX will be launched with superiorities, such as position as a supercar SUV, installation with ADiGO (smart driving internet) ecosystem and L3 automatic assistance driving system, as well as comprehensive endurance exceeding 600 km, which is expected to promote GAC to win reputation and to improve product mix.

Production Expansion of Japanese Brands Imminently

We expect that the strong momentum of Japanese brands will continue, and the blockbuster models Haoying of GAC Hongda and Willanda of GAC Toyota to be launched at the end of the year will continue to enhance the product matrix of joint ventures. The production expansion project of GAC Toyota and GAC Hongda is expected to be put into production at the end of the year. Each of the production capacity will increase by 120,000 to 240,000 units, which will accumulate strength for the development in the next stage.

Investment Thesis

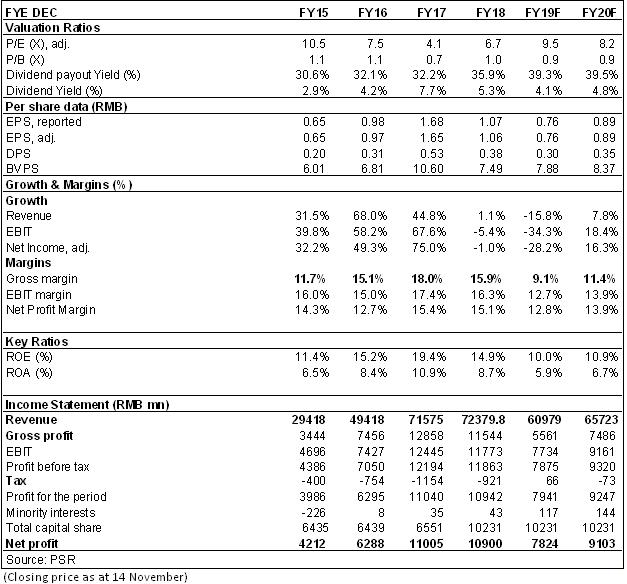

Thanks to the strong momentum of GAC Toyota/GAC Honda, the Company's result safety mat is thicker; the self-owned brands are expected to gradually stabilize and rebound under the help of the new generation models and new energy models. We revised the Company's 2019/2020 earnings forecast. We give the "Accumulate" rating with the target price to HKD 8.9, equivalent to 10.4/8.9x P/E and 1.0/0.9x P/B ratio in 2019/2020. (Closing price as at 14 November)

Financials

Click Here for PDF format...