Investment Summary

Decreased Sales Volume of New Energy Vehicles in July/August Due to Many Factors

The advance consumption caused by the subsidy decline overdraws the demand for China NEVs in H2. The macro-economy is weak. The China-US trade dispute has suppressed the potential purchase demand of some consumers. The wait-and-see atmosphere is strong. The rapidly developing NEV market in recent years has also begun to be affected. BYD, as the industry leader, is also facing an impact. On the other hand, the subsidy policy changes in the last year led to ¡§low before and high after¡¨ of its NEVs sales. We expect that the yoy growth rate from H2 will hardly improve under the trend of ¡§high before and low after¡¨ this year. BYD's sales of NEVs decreased by 11.8% in July and 23.4% in August to 16,567 and 16,719, respectively.

Facing Fierce Competition, but Negative Marginal Effect of Subsidy Decline is Diminishing

We believe that the negative effects on vehicle enterprises will be further reduced by 2020, as the state subsidy for NEVs has been reduced to between RMB10,000 and RMB25,000 at present. Enterprises with scale advantages win the battery cost, output efficiency and component cost, and have stronger anti-risk capability.

Short-term Profit under Pressure, and Long-term Growth Potential

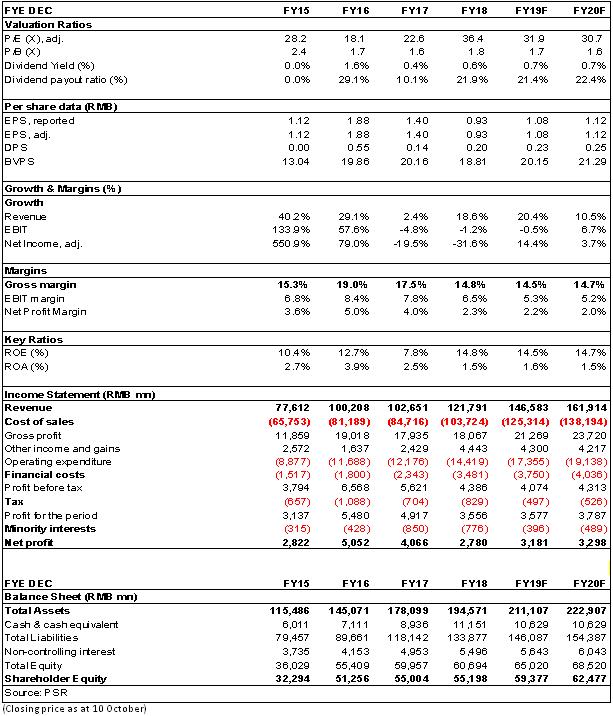

In 19H1, the Company recorded a net profit of RMB1,455 million, up 203.61% yoy, mainly due to the large increase in sales of NEVs. In H1, the Company sold 228,000 vehicles, up 1.6% yoy, including 141,000 new energy passenger vehicles, up 98% yoy, and its market share in NEVs rose from approximately 20% in 2018 to 24% in the period. The Company simultaneously announced that the performance range for 2019 Q3 was between RMB100 million and RMB300 million, down 71% to 90% yoy, mainly due to the subsidy decline and the decline in the automobile market, which affected the demand for NEVs.

Facing the increasing number of competitors, BYD started to accelerate the introduction of new models and continue to open up its supply chain system to enhance its competitiveness with ten years of deep cultivation in the local market. In H1, the Company introduced a new generation of Tang EV, Song MAX plug-in, Yuan EV, and e-series products "e1" and SUV models "S2", which mainly focus on the middle and low-end market. In H2, the Company will successively introduce models such as e2, e3 and new Qin EV to further improve the product layout.

In July 2019, BYD has reached a cooperation with Toyota to jointly develop electric vehicles for the Chinese market. As domestic and international leaders in electric vehicles, both sides have their own unique technological advantages and rich R&D experience in the fields of automobiles and energy batteries, motors, and electric controls. This cooperation will have a far-reaching impact on the Company's long-term development and the competitive pattern of the industry.

Investment Thesis

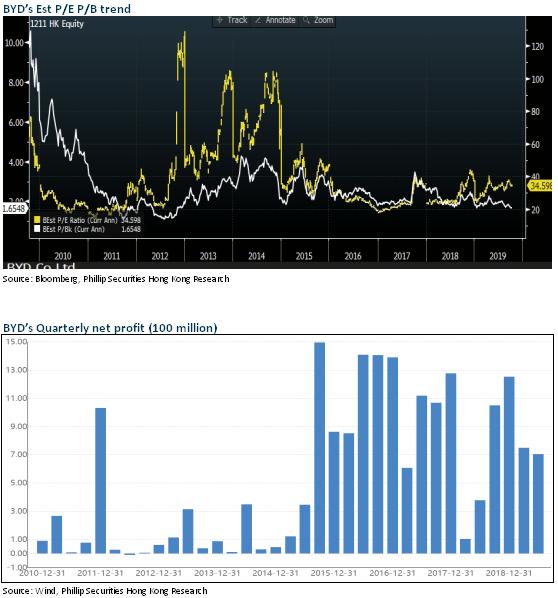

Although the results of BYD in 2019Q3 are below expectation, the technological improvement, transformation and implementation of BYD in recent years have activated its overall competitiveness again. We are optimistic about the more stable and sustainable growth of the Company in the future. As the latest estimates, we revise the target price to HKD44, which corresponded to 2.0/1.9x P/B 36.8/35.5 x P/E ratio for 2019/2020. We give the rating of ¡§Accumulate¡¨. (Closing price as at 10 October)

2019H result

Revenue Increased by Approximately 15%, and Contribution of NEVs Increased to 42%

BYD recorded a revenue of RMB59,215 million in 2019 H1, up 14.06% yoy. Among the revenue components, the business of automobiles and related products was RMB32,238 million, up 16.06% yoy; mobile phone components and assembly business amounted to RMB23,002 million, up 15.15% yoy; revenue from rechargeable batteries and photovoltaic business was approximately RMB3,975 million, down 4.46% yoy. The three major businesses accounted for 54.45%, 38.84% and 6.71% of the total revenue, respectively. Specially, the NEV business recorded a revenue of approximately RMB25,111 million, up 38.84% yoy, accounting for 42.41% of the revenue.

Doubled Profits with Increased Volatility in Performance

In H1, the Company recorded a net profit of RMB1,455 million, up 203.61% yoy, mainly due to the large increase in sales of NEVs. In H1, the Company sold 228,000 vehicles, up 1.6% yoy, including 141,000 new energy passenger vehicles, up 98% yoy, and its market share in NEVs rose from approximately 20% in 2018 to 24% in the period. The Company simultaneously announced that the performance range for 2019 Q3 was between RMB100 million and RMB300 million, down 71% to 90% yoy, mainly due to the subsidy decline and the decline in the automobile market, which affected the demand for NEVs.

Overall Improved Gross Margin and Decreased Period Expense

In H1, the Company's comprehensive gross margin was 17.14%, increased by 1.21 ppts yoy. The increase in gross margin in the automobile sector was partially offset by the decrease in gross margin in the mobile phone sector. Benefiting from the large increase in sales volume driven by NEVs and the obvious scale effect, as well as the low base caused by policy changes in the same period last year, the gross margin of the automobile business was 23.2%, increased by 4.5 ppts yoy; mobile phone business was affected by fierce competition and declining demand from some customers, with gross margin decreased by 3.9 ppts to 8.6%; rechargeable batteries and photovoltaic business still have losses.

The Company's cost control was good, with a period cost rate of 13.38%, decreased by 1 ppts yoy. The sales expense rate, administration expense rate and financial expense rate were 3.7%, 3.33% and 2.34%, respectively, down 1.15%, up 0.08% and down 0.17 ppts yoy, respectively.

Cash flow from operating activities recorded a net outflow of RMB2,064 million, mainly due to increased accounts receivable and increased purchases of goods. In H2, cash flow is expected to improve as state subsidies are in place. The Company expanded against the trend, with R&D investment and capital expenditure increasing continuously. During the reporting period, the R&D investment was approximately RMB4 billion, with a capital expenditure of RMB10.9 billion, mainly for the expansion of battery capacity and the development of automobile projects.

Risk

Sales of NEVs is not as good as expected

Cloud Rail business risk

Slow-down of Hand-set components business

Financials

Click Here for PDF format...