Company Update

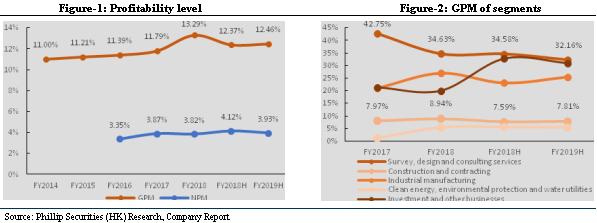

For the six months ended June 30, 2019, the company recorded revenue of RMB 110.045 billion, representing an increase of 8.40% YoY, the increase in revenue was mainly due to the growth in business volumes of both in construction and contracting segment and industrial manufacturing segment, etc. The company achieved gross profit of RMB 13.707 billion, showing an increase of 9.18% YoY, the increase in gross profit was mainly due to the increase in business scale and the increase in selling price of cement business. The net profit attributable to shareholders was RMB 2.158 billion, a YoY increase of 5.90%.

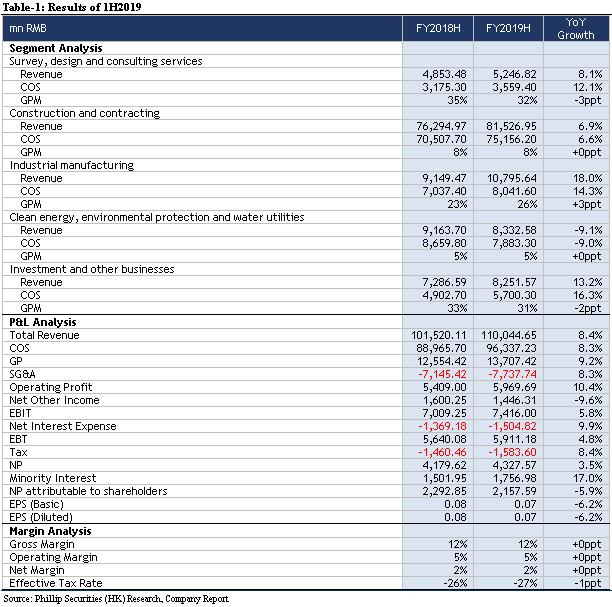

According to business segments, the revenue of survey, design and consulting services business amounted to RMB 5,246.8 million, representing an increase of 8.10% YoY, mainly due to the increase in power transmission and transformation business and non-power businesses such as municipal construction, etc.; segment gross profit amounted to RMB 1,687.4 million, representing an increase of 0.55% YoY; the gross profit margin was 32.16%, representing a slight YoY decrease, mainly due to the increase in labour cost, etc. The revenue of construction and contracting business amounted to RMB 81,526.9 million, representing an increase of 6.86% YoY, mainly due to the growth in the revenue of non-power businesses as a result of the large-scale production of PPP projects; the gross profit amounted to RMB 6,370.7 million, representing an increase of 10.08% YoY; the gross profit margin was 7.81%, representing a slight YoY increase, mainly due to the increase in proportion of revenue from non-power projects with higher gross profit margin. The revenue of industrial manufacturing business amounted to RMB 10,795.6 million, representing an increase of 17.99% YoY, mainly due to the increase in the sales volume and selling price of cement business and the growth of civil explosives business; the gross profit amounted to RMB 2,754.0 million, representing an increase of 30.39% YoY; the gross profit margin was 25.51%, representing a slight YoY increase, mainly due to the YoY increase of the selling price of cement products. The revenue of clean energy, environmental protection and water utilities business amounted to RMB 8,332.6 million, representing a decrease of 9.07% YoY, mainly due to the decrease in revenue of environmental protection business; the gross profit amounted to RMB 449.3 million, representing a decrease of 10.84% YoY; the gross profit margin was 5.39%, remaining steady on a YoY basis.

According to value of newly signed contracts, the company's value of newly signed contracts amounted to RMB 276.189 billion in 1H2019, up by 7.12% YoY. Among which, the value of domestic newly signed contracts amounted to RMB 171.342 billion, representing a YoY increase of 2.11%, which accounted for 62.04% of the value of newly signed contracts; the value of international newly signed contracts amounted to RMB 104.847 billion, representing a YoY increase of 16.45%, which accounted for 37.96% of the value of newly signed contracts. As of 30 June 2019, the outstanding contract value of the company was RMB 1,218.205 billion, representing an increase of 13.59% YoY.

Power business leads the development of the company, consolidate the leadership position

In 1H2019, newly signed contracts for domestic power engineering business of the company valued RMB 84.260 billion, up by 14.56% YoY, among which, the value of newly signed contracts of hydropower, power transmission and transformation, fossil-fuel power and nuclear power grew by 970.86%, 39.71%, 5.33% and 3.60%, respectively; subject to various factors such as adjustment to the PV policy, the value of newly signed contract for new energy decreased by 32.04% YoY. The company has signed a number of representative power project contracts including Shaanxi Fanhai Hongdunjie integrated coal-fired power plant project, Anhui Hefei Longquan Mountain incineration of municipal solid wastes power generation project, Xinjiang Kumul tower 50MW solar thermal power generation project, and Jiangsu Lianyungang Xuwei New Area 220 kV Kongqiao power transmission and transformation project. In 1H2019, the national power consumption in China was 3,398 billion KWh, representing a YoY increase of 5.0%. The national power consumption maintained growth momentum.We believe that the domestic power engineering business would keep stably growing on the basis of increasing investment in domestic power generation project in China.

Continue to promote non-power business, to achieve business transformation and development

In 1H2019, the value of newly-signed contracts for domestic non-power engineering business amounted to RMB 87.082 billion, representing a year-on-year decrease of 7.60%, which accounted for 50.82% of the total value of domestic newly signed contracts of the company, among which, the company continued to use new business models such as PPP to expand the domestic non-power engineering market, focused on enhancing the management and control of the sourced of PPP projects, elevated the quality of PPP project contracts, and the value of newly-signed contracts for the business of new business models amounted to RMB 32.684 billion, which accounted for 37.53% of total value of domestic newly signed contracts of the company. Businesses of new business models in four new construction investment companies rapidly grew, representing a YoY increase of 47.06% in the amount of newly signed contracts. The company signed a number of major non-power projects including Zhejiang Ningbo Fenghua transportation infrastructure construction and ecological culture city development cooperation project, Shaanxi Shangluo Xintai Company gravel aggregate project, Hebei's Third Garden Expo Park PPP project, and Henan Lingbao urban road network construction PPP project.

Continue to develop ¡§One Belt and One Road¡¨, international business breakthrough

In 1H2019, the value of international newly signed contracts amounted to RMB 104.847 billion, which set a new record in the history, representing a YoY increase of 16.45%, which accounted for 37.96% of the newly signed contracts of the company. The growth of China's foreign contracting construction enterprises topped the list. The vompany continued to explore the markets along the Ùqne Belt and One Road? The value of newly signed contracts with the countries along the Ùqne Belt and One Roadöá amounted to RMB 85.351 billion, representing a YoY increase of 39.73%, which accounted for 81.41% of the total value of international newly signed contracts of the company. We expect that the company will continue to benefit from ¡§One Belt and One Road¡¨ strategy and sign more infrastructure projects in 2H2019. The value of newly signed contracts for international power engineering and international non-power engineering were RMB 78.696 billion and RMB26.151 billion, respectively, both showing a lift, representing YoY increases of 4.22% and 80.08%, respectively, and achieved vital breakthroughs in non-power engineering markets in many countries; the value of newly signed contracts for international engineering procurement construction business increased by 5.81% YoY. In addition, the company has successfully signed a number of representative international contracts, including the Petrolex Combined Cycle Gas Turbine in Nigeria, the Ban Taen Coal-fired Power Station in South Sulawesi, Indonesia, the Kayang A Hydropower Project in Indonesia, the Mohmande Dam Project in Pakistan, the Biomass Power Station Group Project with a Total Capacity of 200 MW in Ukraine, Dongyu-Payaji 500 kV Transmission and Transformation Project in Myanmar, Civil explosives Project in Saudi Arabia, and the Mongolian Erdente to the Baobate Railway Project.

Maintain "BUY" Rating

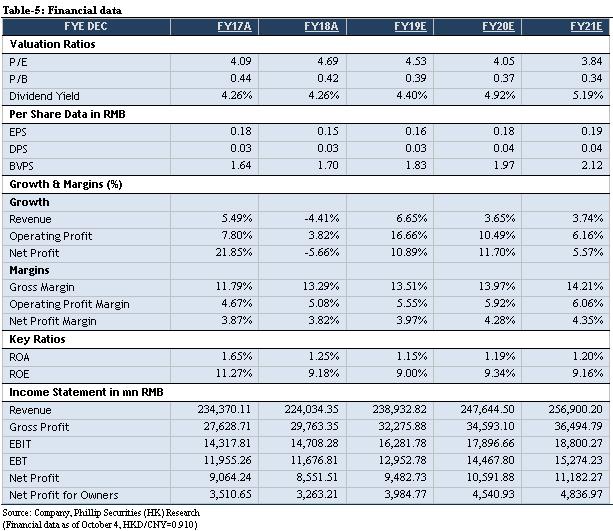

We adjusted our forecast for FY19/FY20/FY21 incomes to RMB 238.9/247.6/256.9 billion, showing increases of 6.65%/3.65%/3.74% YoY; net profit attributable to shareholders were RMB 4.7/5.3/5.6 billion, with increase of 3.44%/11.70%/5.57% YoY; the corresponding EPS was RMB 0.16/0.18/0.19. The target price was adjusted to HKD 1.02, corresponding to FY19/FY20/FY21 5.85x/5.24x/4.96x PE, which was +29.11% higher than the current price (HKD 0.79 as of October 4, 2019), maintaining a ÙYUY?rating.

Risk

1. International business fails expectations

2. China infrastructure investment fails expectations

3. China electricity investment fails expectations

�Financials

Click Here for PDF format...