Investment Summary¡G

Half-year results decreased by 15%

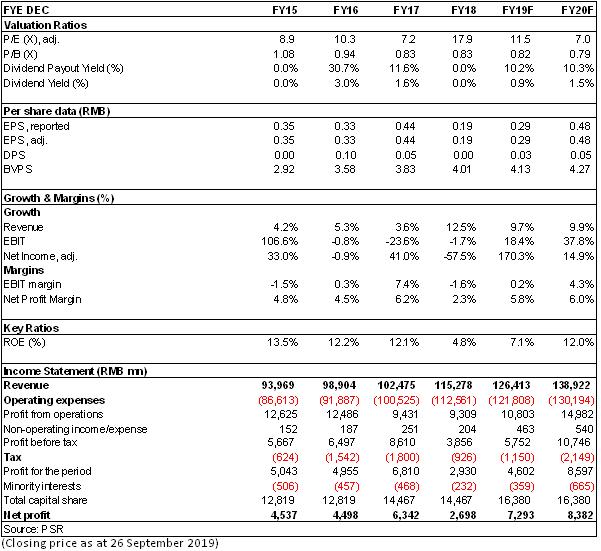

In 2019 H1, China Eastern Airlines (CEA) recorded a revenue of RMB62.3 billion, up by 8% yoy, a net profit attributable to the parent company of RMB1.94 billion, down 14.89% yoy, and a net profit excluding non-recurring items of RMB1.56 billion, a decrease of 26% yoy.

In 2019 Q1 and Q2, the Company recorded a revenue of RMB30.1 billion and RMB28.7 billion, respectively, an increase of 12.3% and 3.84% yoy, while it also recorded a net profit attributable to the parent company of +RMB2.01 billion in Q1, an increase of 1.2%, and -RMB63 million in Q2, an increase of RMB360 million in loss.

The fuel cost was stable and the net exchange loss was narrowed

During the period, the operating costs increased by 9% yoy, faster than revenue growth, and thus the gross margin decreased by 1.2 ppts yoy. Specially, the fuel cost was RMB16.63 billion, an increase of 9% yoy, due to small fluctuations in fuel prices. Oil withholding cost increased by 9.4%, while unit oil withholding cost decreased slightly by 1%, reflecting the continuous improvement of cost control measures by the Company. Due to the different changes in the RMB exchange rate, the Company's net exchange loss in 2019 H1 was approximately RMB200 million, down 64% from RMB550 million in the same period last year.

Under the macro environment, domestic routes were the main drag

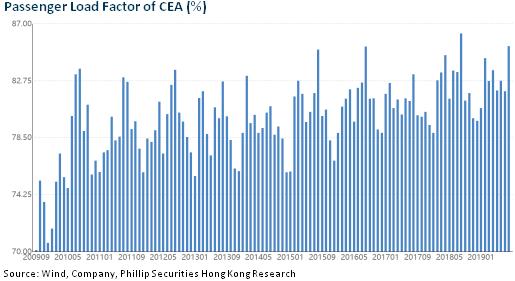

In 2019 H1, CEA added a net of 24 aircraft, with the growth rate of capacity delivery at the top of the three major airlines. ASK increased by 10.4% and RPK increased by 10.6% yoy. The P L /F increased by 0.19 ppts to 82.66% yoy, the highest among the three major airlines, and the P L /F of domestic routes decreased by 0.39 ppts due to the large capacity. The yield was RMB0.513, a decrease of 1.35% yoy, mainly due to the low level of fares for domestic routines, which reduced the yield of domestic routes by 2.38%. International and regional routes recorded good growth due to the booming demand for Japanese and Korean routes and Taiwan routes.

The impact of new accounting standards and exchange rate fluctuations on the Company was the lowest among peers

As at the end of June 2019, the amount of interest-bearing liabilities under the new lease term was RMB170.5 billion, compared with RMB139 billion under the original term, of which USD interest-bearing liabilities were RMB48.9 billion, accounting for 29%, accounting for 14% under the original term. RMB fluctuated 1% against USD, affecting a net profit of RMB300 million, the lowest among the three major airlines.

Future focus

In August, CEA completed its cross-shareholding with Juneyao Airlines in Hong Kong. After the A-share issuance is completed, CEA will hold 15% of Juneyao Airlines and Juneyao Airlines (JuneYao Group) will hold approximately 10% of CEA in total. Together, the two sides account for more than 50% of Shanghai's aviation market. Under a closer enterprise strategic cooperation model of cross-shareholding, they will fully integrate resources and bring into play synergies in the future. After the opening of the S1 satellite hall at Pudong International Airport in September, the improvement of the Company's transfer connection efficiency at Pudong International Airport will help enhance the Company's competitiveness in Shanghai's core hub.

Investment Thesis

We believe that under the double pressure of China-US trade disputes and weak domestic economy, the uncertainty of demand is increasing, but the favorable trend of capacity regulation, market-oriented reform of routine fares and the reduction of government burdens and taxes is still expected to continue.

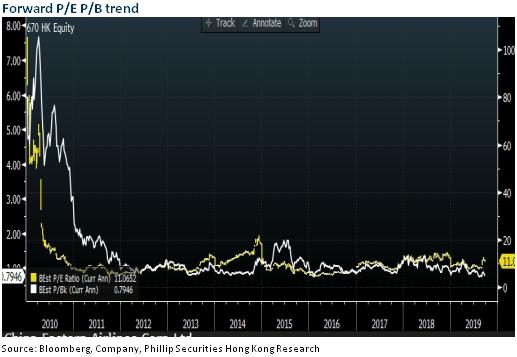

We expect the company's 2019/2020 EPS of RMB0.29/0.48. Given that possible improvement on efficiency after the mix reform, and the expected better ticket price in the future, we are optimistic about the Company's future result flexibility. Therefore, we set the target price at HK$4.4, equivalent to 13.5/8.2X estimated P/E, and 0.96/0.93X estimated P/B for 2019/2020. Also, the "Accumulate" rating is given. (Closing price as at 26 September 2019)

Risk

Traffic demand languished for the deterioration of macro-economy;

The depreciation of the RMB against USD would bring exchange loss;

Oil prices rose exceeded forecast;

War, terrorist attacks, SARS and other emergencies;

Highspeed railway diversion;

Boeing 737MAX deteriorate

Financials

Click Here for PDF format...