|

SHIRBLE STORE(312)

Analysis¡G

As at 30 June 2019, Shirble Store (312) owned and operated 17 department stores with total gross floor area of 330,627 sq.m. The Group has been actively transforming its business model. In the process, the Group has come to realise the huge business potential of integrating online and offline platforms via cooperation with business partners, such as the partnership with Hema of Alibaba group to introduce ¡§Hema Fresh Supermarket¡¨ at Shirble premises. In the first half of 2019, eight of the 11 Shirble supermarkets had been transformed into ¡§Hema Fresh Supermarket¡¨. The remaining three is expected to complete transformation by second half of 2019. Additionally, the Group has diversified into the property and food & beverages business segments) to better position the ¡§Shirble¡¨ brand for targeting the middle-class and the young generation customers. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $1.25, Target Price: $1.40, Cut Loss Price: $1.15

|

CHINA OVS PPT(2669)

Analysis¡G

The Group is principally engaged in the provision of property management and value-added services, and the parent company is China Overseas Development (688). The Group announced its interim business with revenue of RMB 2.4 billion, up 25.9% year-on-year. The profit for the period also reached RMB 250 million, up 11.8% year-on-year. The Group's annualized return on equity remained high at around 41%. The Group received a new or renewed property management contract amounting to approximately HK$359.1 million. As of June 2019, the total gross floor area of the Group's properties under management increased by 7.9% or 10.5 million square meters to 142.2 million square meters. However, the direct operating cost increased rapidly, up 39.1% year-on-year, causing the gross profit margin to fall by 20.1% from 27.7%. However, sales and administrative expenses also fell by 36.6% year-on-year, which caused the operating profit margin to fall only 1.9% year-on-year. The Group started its parking lot trading business in 2018. It recorded revenue of about 5 million in the first half of 2019. It is believed that it will become another growth driver of the Group in the future.

Strategy¡G

Buy-in Price: $3.60, Target Price: $4.50, Cut Loss Price: $3.00

iShares U.S. Medical Devices ETF (IHI)

iShares U.S. Medical Devices ETF tracks the performance of the Dow Jones US Select Medical Equipment Index, with market cap of approximately USD 2.56 billion and expense ratio of 0.43%. The ETF holds 58 health care stocks of varying cap sizes. Its investments are focused in health care equipment and supplies. Some of the top 10 holdings of IHI include ABBOTT LABORATORIES, MEDTRONIC PLC, STRYKER CORP, DANAHER CORP and BOSTON SCIENTIFIC CORP.U.S. medical devices companies have a substantial competitive advantage due to significant innovations in microelectronics, biotechnology and software. The demand for medical devices is expected to increase throughout the world due to the aging population. Hence, IHI is poised to take advantage of the future growth prospects in this sector.In 2019, S&P 500 Healthcare Equipment Index generated 23.41% total return , which was greater than that of S&P 500 Index (21.30%) and that of S&P Healthcare Index (6.63%). Within health care sector, large-cap medical device stocks were the best performers in 2018. Although medical device stocks` P/E ratio is at decade high (19x for 2019), the organic growth of the sector is likely to remain strong due to new product cycles, strong emerging-market demand and better operating margin in 2019. Additionally, the sector is also benefiting from Trump tax reform policy, which encourages increased M&A activities and R&D activities. Heading into 2019 of expected economic slowdown and US-China trade war, investor can invest in IHI ETF as health care stocks have historically been considered non-cyclical, defensive stocks.Entry Price: USD 250.03Stop Loss: USD 245.58Target Price: USD 265.80

|

|

|

Ausnutria (1717.HK) - Own-branded goat milk powder business with fast growing trend; opening up elderly market with goat milk powder products

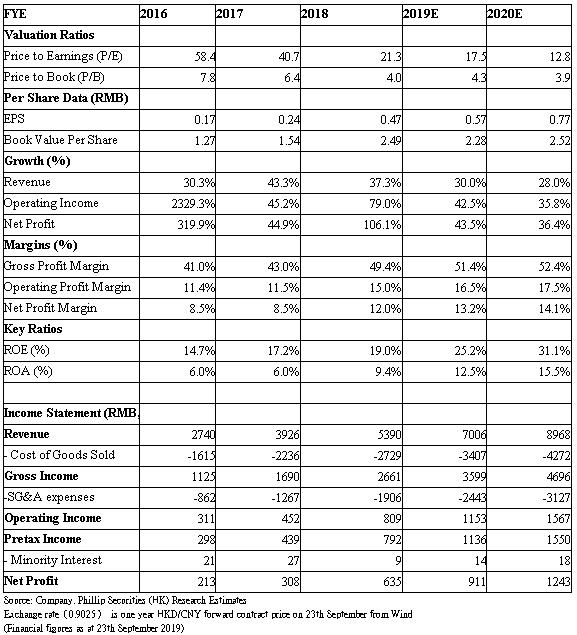

Investment SummaryShort seller Blue Orca has recently published reports about Ausnutria Dairy. The main allegations include overstating import data of infant milk formula, revenue and profits; understating its labor and staff costs; misleading Chinese consumers in relation to the ingredients of Kabrita infant goat milk formula; the acquisition of the 40% equity interest in Nutriunion HK was a sham transaction to unjustly enrich insiders, and the independence of the company's distributors. Apart from releasing voluntary announcement clarification, the independent review committee has been established and engaged the independent consultant to conduct the independent review. In responding to the allegation of overstating import data of infant milk formula, revenue and profits, Ausnutria denied and pointed out that all import data are supported by documents. The report only counts the number of shipments of import agents. The estimation was arrived after deducting the company's inventory level. such estimation did not take into account the overhead costs incurred and value-added processes conducted by the company after the imported infant milk products arriving the Changsha, and did not take into account of the purchase of imported base powder (mainly New Zealand) from local importers. The independent consultant also noted that the import volume of goat milk in 2017 as per the customs` records was 154% higher than the annualised import volume as estimated by the short seller reports. We are still optimistic about Ausnutria's medium and long-term business. Although China is facing a problem of declining birth rate, consumption upgrade continues in the infant milk industry. In 1H of 2019, the overall infant milk industry recorded a mid-single digit growth, which was mainly driven by ASP growth, and the trend is expected to continue. Ausnutria has conducted market research consistently with targeted consumers to raise the awareness of goat milk products. In view of the decline in birth rate, goat milk formula for kids has been launched. The company plans to also launch goat milk formula for the whole family, targeting adults and elderly. In 1H of 2019, in the imported formula milk milk powder market, Kabrita's market share in China reached 64.4%, accounting for 61.7% of the total imported goat milk powder. It is still the market leader. Its interim revenue increased by 21.9% y.o.y. to RMB565 million. The growth of its own-branded formula cow milk powder recorded a slowdown but still with a 20.7% increase, among which organic formula milk powder increased by 52.3%. The proportion of overall own-branded formula milk powder business increased by 6.3 ppt to 86.7%. Benefiting from the increase in the proportion of its own brands, the gross profit margin increased by 5.7 ppt y.o.y. to 52.1%. The ratio of sales and distribution expenses to revenue was basically maintained at 27.4% y.o.y.. We expect overall revenue growth in 2H of the year to be faster than 1H. The slowdown in the growth of its own-branded formula cow milk powder business in 1H was mainly due to the high base in the same period last year and the delay in the approval of registration. As for the private label and other business, the y.o.y. decline in 1H was mainly due to the strategic reorientation. As the new plant was completed, it is expected to gradually ease the problem of production capacity shortage. Ausnutria plans to terminate its butter business in the second quarter, and inventory will be cleared in 2H. We maintain buy rating, target price-earnings ratio 25 times, with target price HKD15.7. (current price as of September 23, 2019) Investment Thesis & ValuationWe give buy rating, target price-earnings ratio 25 times, with target price HKD15.7. Potential investment risks include policy change, market competition deterioration, and raw milk cost with huge volatility. (current price as of September 23, 2019)

Financials

Click Here for PDF format...

| Recommendation on 26-9-2019 | | Recommendation | Buy | | Price on Recommendation Date | $ 11.000 | | Suggested purchase price | N/A | | Target Price | $ 15.700 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|