|

|

BOC AVIATION(2588)

Analysis¡G

The group is a leading global aircraft operating leasing company in Asia. In the first half of 2019, the revenue was US$830 million, an increase of 10.5% year-on-year. The net profit for the first half of 2019 was HK$320 million, an increase of 8.1% year-on-year. The group serves 92 airlines in 40 countries and regions, with a total of 499 aircraft owned, managed and ordered, of which 314 aircraft are owned (as of June 30, 2019). The average age weighted by net book value is 3.1 years, and the average remaining lease term is 8.2 years. The order book includes 162 aircraft and will be delivered between 2019 and 2021. Although the current economic downside risks are getting higher, the outlook for the aviation industry is still generally optimistic. The International Air Transport Association (IATA) reported a passenger growth rate of 4.7% for the six months ended June 30, 2019. IATA expects passenger growth to maintain a projected 5% growth rate for passenger traffic over the remainder of 2019, and expects airline revenue to be $28 billion in 2019. In addition, even if the aviation industry is affected by the economic downturn, the group and sign long-term contracts with airlines and collect rents from them, so as long as the airlines are not bankrupt, the group`s income will remain stable.

Strategy¡G

Buy-in Price: $70.00, Target Price: $78.50, Cut Loss Price: $65.00

ARK Innovation ETF (ARKK)

ARK Innovation ETF is an actively-managed thematic ETF incorporated in the USA, with market cap of approximately USD 1.34 billion and expense ratio of 0.75%. The investment theme of ARKK is ¡§disruptive innovation¡¨. ARKK mainly focus on investing in companies introducing technologically advanced products or services which potentially changes the way the world works. The issuer of ARKK, ARK identifies 36 innovative companies from four themes: ¡§Genomic Revolution¡¨, ¡§Industrial Innovation¡¨, ¡§Next Generation Internet¡¨ and ¡§Fintech Innovation¡¨. For ¡§Genomic Revolution¡¨, the fund invests in healthcare companies based on R&D of DNA technologies including gene therapy and Molecular Diagnostics. For ¡§Industrial Innovation¡¨, the fund puts the emphasis on areas of autonomous vehicles, 3D printing and Robotics. For ¡§Next Generation Internet¡¨, the fund targets in companies from digital media, social platform, cloud computing, Internet of things and E-commerce. For ¡§Fintech Innovation¡¨, the fund offers exposure on technology which makes financial services more efficient such as big data& machine learning, Blockchain and P2P. Compared to mutual funds with true active management, ARKK is more cost effective, which offers investors exposure to innovation across sectors.Entry Price: USD 45.62Stop Loss: USD 42.3Target Price: USD 48.98

|

|

|

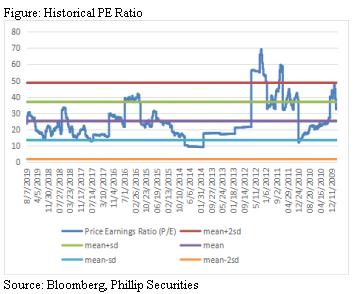

Ausnutria (1717.HK) - Own-branded goat milk powder business with fast growing trend; opening up elderly market with goat milk powder products

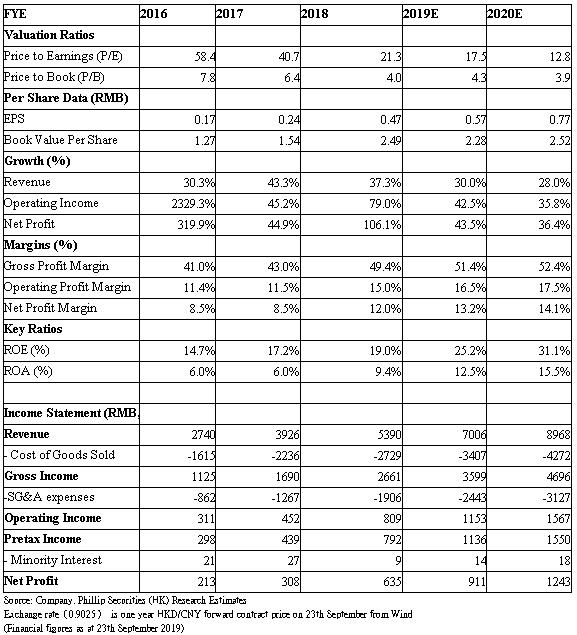

Investment SummaryShort seller Blue Orca has recently published reports about Ausnutria Dairy. The main allegations include overstating import data of infant milk formula, revenue and profits; understating its labor and staff costs; misleading Chinese consumers in relation to the ingredients of Kabrita infant goat milk formula; the acquisition of the 40% equity interest in Nutriunion HK was a sham transaction to unjustly enrich insiders, and the independence of the company's distributors. Apart from releasing voluntary announcement clarification, the independent review committee has been established and engaged the independent consultant to conduct the independent review. In responding to the allegation of overstating import data of infant milk formula, revenue and profits, Ausnutria denied and pointed out that all import data are supported by documents. The report only counts the number of shipments of import agents. The estimation was arrived after deducting the company's inventory level. such estimation did not take into account the overhead costs incurred and value-added processes conducted by the company after the imported infant milk products arriving the Changsha, and did not take into account of the purchase of imported base powder (mainly New Zealand) from local importers. The independent consultant also noted that the import volume of goat milk in 2017 as per the customs` records was 154% higher than the annualised import volume as estimated by the short seller reports. We are still optimistic about Ausnutria's medium and long-term business. Although China is facing a problem of declining birth rate, consumption upgrade continues in the infant milk industry. In 1H of 2019, the overall infant milk industry recorded a mid-single digit growth, which was mainly driven by ASP growth, and the trend is expected to continue. Ausnutria has conducted market research consistently with targeted consumers to raise the awareness of goat milk products. In view of the decline in birth rate, goat milk formula for kids has been launched. The company plans to also launch goat milk formula for the whole family, targeting adults and elderly. In 1H of 2019, in the imported formula milk milk powder market, Kabrita's market share in China reached 64.4%, accounting for 61.7% of the total imported goat milk powder. It is still the market leader. Its interim revenue increased by 21.9% y.o.y. to RMB565 million. The growth of its own-branded formula cow milk powder recorded a slowdown but still with a 20.7% increase, among which organic formula milk powder increased by 52.3%. The proportion of overall own-branded formula milk powder business increased by 6.3 ppt to 86.7%. Benefiting from the increase in the proportion of its own brands, the gross profit margin increased by 5.7 ppt y.o.y. to 52.1%. The ratio of sales and distribution expenses to revenue was basically maintained at 27.4% y.o.y.. We expect overall revenue growth in 2H of the year to be faster than 1H. The slowdown in the growth of its own-branded formula cow milk powder business in 1H was mainly due to the high base in the same period last year and the delay in the approval of registration. As for the private label and other business, the y.o.y. decline in 1H was mainly due to the strategic reorientation. As the new plant was completed, it is expected to gradually ease the problem of production capacity shortage. Ausnutria plans to terminate its butter business in the second quarter, and inventory will be cleared in 2H. We maintain buy rating, target price-earnings ratio 25 times, with target price HKD15.7. (current price as of September 23, 2019) Investment Thesis & ValuationWe give buy rating, target price-earnings ratio 25 times, with target price HKD15.7. Potential investment risks include policy change, market competition deterioration, and raw milk cost with huge volatility. (current price as of September 23, 2019)

Financials

Click Here for PDF format...

| Recommendation on 25-9-2019 | | Recommendation | Buy | | Price on Recommendation Date | $ 11.000 | | Suggested purchase price | N/A | | Target Price | $ 15.700 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|