Investment Summary

Leading integrated water environmental solutions provider in the PRC with a strong project pipeline

The company is a leading integrated water environmental solutions provider in the PRC, providing a comprehensive range of environmental water services. Its business spans wastewater treatment, water environment treatment, integrated utilization of water resources and water ecological protection. According to Frost & Sullivan, the company is the largest Central State-Owned Enterprise operating in the wastewater treatment industry in the PRC, as well as the third largest wastewater treatment service provider in the Bohai Economic Rim in terms of treatment capacity in 2017. It's also one of the top 10 integrated water resources solutions providers in the PRC in terms of 2017 market share, and one of only three companies in the PRC that is ranked top ten in both the municipal wastewater treatment market and the water environment management market in terms of market share.

The water industry is less concentrated and huge space for M&A opportunity

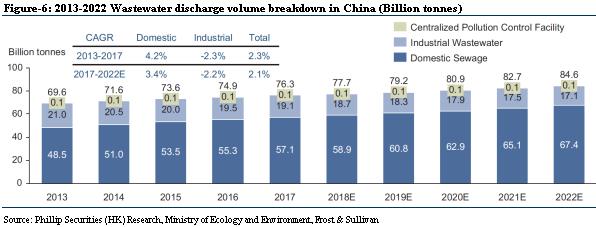

The growth of urbanization in China has created long-term demand for water and sewage treatment business. The discharge volume of domestic sewage has continued to grow since 2013, increasing from 48.5 billion tonnes in 2013 to 57.1 billion tonnes in 2017, representing a CAGR of 4.2%. By the end of 2016, China had built 3,552 sewage treatment plants in urban and rural cities, with the sewage treatment capacity of about 190 million m3/day, and the growth rate was between 4%-6% in recent years. In terms of water supply, by the end of 2016, the urban water penetration rate has reached 98.4%, and the county water penetration rate has also reached 90.5%. In recent years, the construction of water supply facilities has approached saturation, and the total urban water supply in China has remained basically stable, maintaining a growth rate of 1%-3%.

Strong potential for organic growth as well as expansion through acquisitions as supported by ¡§Everbright¡¨ brand

The company's controlling shareholder, CEIL, is a market leader in the environmental protection industry in China. The parent company of CEIL, China Everbright Group, is a large-scale conglomerate among the Fortune Global 500 and has a well- recognized brand image. China Everbright Group has a diversified business portfolio covering banking, securities, insurance, funds, finance leasing and industries, and has an outstanding track record for its business performance with a national presence. As a member of China Everbright Group, the company has benefited from the reputation, business network and the strong track record of China Everbright Group and CEIL, and has been able to grow in the environmental protection service industry. The company believes that it is able to offer a range of environmental services to the local governments and customers by working alongside other members of China Everbright Group, which creates synergy between the company and the other members of the China Everbright Group..

Initial coverage with TP of HKD 2.64 and investment rating of ¡§BUY¡¨

Based on our residual income valuation model, we initiate coverage on CEB Water with a TP of HKD 2.64, corresponding to FY19/FY20/FY21 9.42x/8.18x/7.72x PER with a 49.79% potential upside compared with CP of HKD 1.76 as of September 20, 2019, and recommend ¡§BUY¡¨ investment rating.

Industry Analysis

The current status of water quality in China

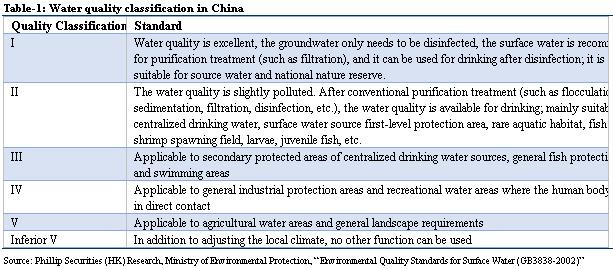

According to the ¡§Environmental Quality Standards for Surface Water (GB3838-2002)¡¨ issued by Ministry of Environmental Protection, the water quality in China is divided into six grades: I, II, III, IV, V and inferior V, of which I-III is good water quality.

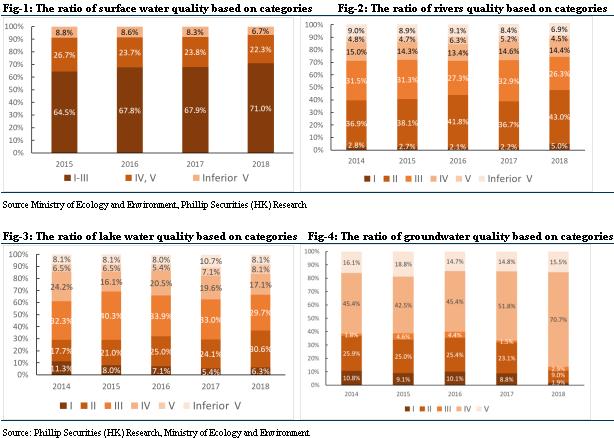

According to the China Ecological Environment Bulletin" issued by the Ministry of Environmental Protection, the water quality of surface water and rivers in China has gradually improved in 2018, but the water quality of lake water and groundwater is not optimistic. The current status of water quality is shown as follows based on the classification:

-For surface water, the proportion of I~III was 74.3%, up 3.1% YoY; the proportion of inferior V was 6.9%, down 1.6% YoY.

-For rivers, the proportion of Class I was 5.0%, up 2.8% YoY; the proportion of Class II was 43.0%, up 6.3% YoY; the proportion of Class III was 26.3%, down 6.6% YoY; the proportion of Class IV was 14.4%, down 0.2% YoY. The proportion of V is 4.5%, down 0.7% YoY; the proportion of inferior V is 6.9%, down 1.5% YoY.

-Among the 111 important lakes (reservoirs), there are 7 lakes (reservoirs) with Class I water quality, accounting for 6.3%, up 0.9% YoY; 34 of Class II, accounting for 30.6%, up 6.5% YoY; 33 of Class III, accounting for 29.7%, down 3.3% YoY; 19 of Class IV, accounting for 17.1%, down 2.5% YoY; 9 of both Class V and inferior V, accounting for 8.1%, up 1% YoY and down 2.6% YoY, respectively. The main pollution indicators are total phosphorus, chemical oxygen demand and permanganate index.

-Among the 10,168 national groundwater quality monitoring points in China, Class I water quality monitoring points accounted for 1.9%, down 6.9% YoY; Class II accounted for 9.0%, down 14.1% YoY; Class III accounted for 2.9%, up 1.4% YoY; Class IV Accounted for 70.7%, an increase of 18.9% YoY; Class V accounted for 15.5%, an increase of 0.7% YoY. The over-standard indicators are manganese, iron, turbidity, total hardness, total dissolved solids, iodide, chloride, "tri-nitrogen" (nitrite nitrogen, nitrate nitrogen and ammonia nitrogen) and sulfate.

The current status of water industry in China

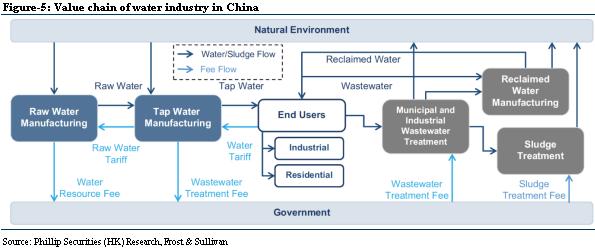

The value chain of water industry in China is as follow: Tap water manufacturers pay tariff to and obtain raw water from raw water manufacturers. Then tap water is delivered to end users through pipe networks, and the water tariff paid by end users is usually composed of tap water tariff and wastewater treatment fee. Wastewater treatment separates all kinds of pollutants through physical, chemical, and biological processes or transforms them into non-toxic substance. Reclaimed water generated through certain treatment processes are delivered to end users, primarily for applications such as irrigation, roadway sanitation, car washing, etc. Treatment of wastewater generates sludge, which contains a massive amount of pollutants. Sludge treatment and disposal is one of the key segments after wastewater treatment, which includes a series of processes that stabilize and reduce sludge, make it environmentally safe (sludge treatment), and utilize the treated sludge (sludge disposal).

The growth of urbanization in China has created long-term demand for water and sewage treatment business. The discharge volume of domestic sewage has continued to grow since 2013, increasing from 48.5 billion tonnes in 2013 to 57.1 billion tonnes in 2017, representing a CAGR of 4.2%. By the end of 2016, China had built 3,552 sewage treatment plants in urban and rural cities, with the sewage treatment capacity of about 190 million m3/day, and the growth rate was between 4%-6% in recent years. In terms of water supply, by the end of 2016, the urban water penetration rate has reached 98.4%, and the county water penetration rate has also reached 90.5%. In recent years, the construction of water supply facilities has approached saturation, and the total urban water supply in China has remained basically stable, maintaining a growth rate of 1%-3%.

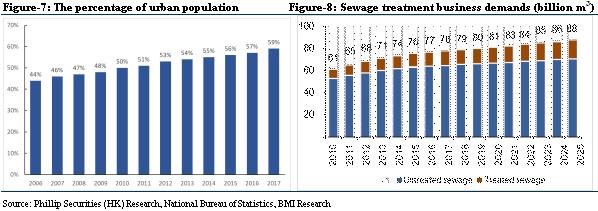

According to the statistics from National Bureau of Statistics, from 2013 to 2017, China's urban population increased from 731.1 million to 813.5 million, with a CAGR of 2.7%. During the same period, the urbanization rate in China increased by 4.8%, from 53.7% to 58.5%. By 2022, China's urban population is expected to reach 934.5 million and China's urbanization rate is likely to reach 65.8%. Correspondingly, according to BMI Research, the sewage treatment demand in China will reach 88 billion m3 by 2025. The sewage treatment market in China has strong demand and insufficient supply, and there are many long-term opportunities in the future sewage treatment business.

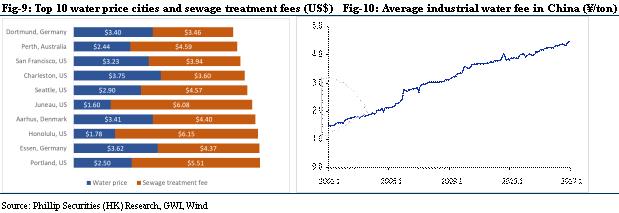

According to the 2017 Global Water Price White Paper released by GWI, water price in China is much lower than that of other countries in the world. The highest water price in China is less than one tenth of the most expensive city in the world, and sewage treatment fees are also much lower than that of the top ten cities with the most expensive water prices in the world. There is still much space for improvement in the water price and sewage treatment fees in China.

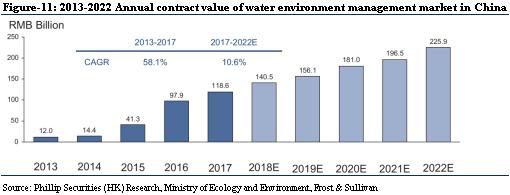

Policy promotion, water environment treatment market still has huge room for development

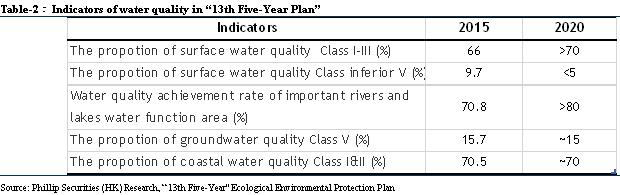

According to the ¡§13th Five-Year Plan for Ecological Environmental Protection¡¨ issued by the State Council in November 2016, by 2020 the proportion of the water quality of centralized drinking water sources at or above the prefecture level reaching or exceeding Class III will be more than 93%; the trend of increasing pollution will be initially curbed, the proportion of groundwater with extremely poor quality is controlled at around 15%; the proportion of black and odorous water in urban built-up areas is controlled within 10%, and other cities strive to eliminate heavy black and odorous water bodies; rivers near coastal provinces (districts, cities) into the sea basically eliminate the inferior V water; all county towns and key towns have sewage collection and treatment capacities, urban and county sewage treatment rates reach 95% and 85%, respectively; prefectural and above cities basically realize the complete collection and treatment of sewage; improving the level of sewage recycling and sludge disposal, vigorously promote sludge stabilization, harmlessness and resource treatment and disposal, and achieves harmless treatment and disposal rate of municipal sludge at prefecture level at 90%, the Beijing-Tianjin-Hebei region reach 95%; the utilization rate of reclaimed water in the water-deficient city reaches more than 20%, and the Beijing-Tianjin-Hebei region reaches more than 30%; promote the construction of sponge city, which can reach the area of utilizing 70% of the rain more than 20% of the total area, and the water-deficient cities of the prefecture level and above all meet the national water-saving city standard requirements, Beijing-Tianjin-Hebei, the Yangtze River Delta and Pearl River Delta regions should complete one year ahead of schedule. The ¡§13th Five-Year Plan¡¨ of ecological environmental protection water environment quality mainly includes the following indicators:

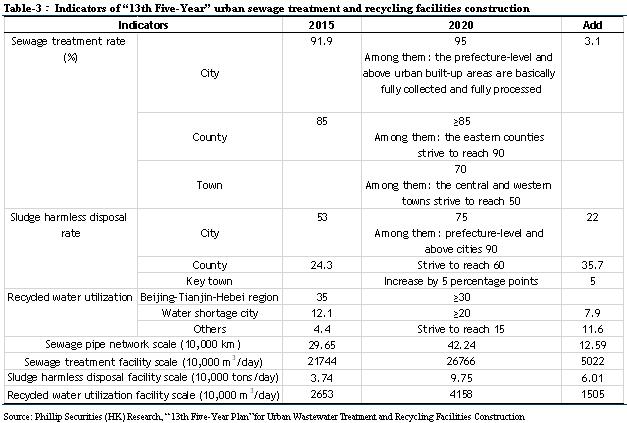

According to the ¡§13th Five-Year Plan for Urban Wastewater Treatment and Recycling Facilities Construction¡¨ jointly prepared by the National Development and Reform Commission and the Ministry of Housing and Urban-Rural Development in December 2016, as of 2015, the national urban sewage treatment capacity has reached 217 million cubic meters/day, the urban sewage treatment rate reached 92%, and the county sewage treatment rate reached 85%. During the ¡§13th Five-Year Plan¡¨ period, the newly added sewage pipe network was 125,900 kilometers, including 66,200 kilometers of city and 29,200 kilometers of county and 30,500 kilometers of town; the old sewage pipe network transformation is 27,700 kilometers, including 15,800 kilometers of city, 0.73 million kilometers of county, 0.46 million kilometers of town; 28,800 kilometers of merged pipe network, 17,000 kilometers of city, 11,700 kilometers of county seat. The newly-added sewage treatment facilities have a scale of 50.22 million cubic meters per day, of which the city has a scale of 28.56 million cubic meters per day, the county has 10.71 million cubic meters per day, and the town has 10.95 million cubic meters per day. the scale of the sewage treatment facilities was upgraded to 42.2 million cubic meters per day, including 36.39 million cubic meters per day in the city and 5.81 million cubic meters per day in the county; new sludge (water-containing 80% wet sludge) has a harmless disposal scale of 60,100 tons/day, including 45,600 tons/day for the city, 9,200 tons/day for the county, and 5,300 tons/day for the town; The newly-added reclaimed water utilization facility has a scale of 15.05 million cubic meters per day, of which 12.14 million cubic meters per day of the city and 2.91 million cubic meters per day of the county.

In terms of investment, the ¡§13th Five-Year¡¨ urban sewage treatment and recycling facilities construction has invested a total of about RMB 564.4 billion. Among them, the investment in various types of facilities construction was RMB 560 billion, and the investment in supervision capacity building was RMB 4.4 billion. In the construction investment, the newly-built supporting sewage pipe network was invested RMB 213.4 billion, the old sewage pipe network transformation investment was RMB 49.4 billion, the rain-sewage pipe network transformation investment was RMB 50.1 billion, and the newly added sewage treatment facility investment was RMB 150.6 billion. The investment in sewage treatment facilities was RMB 43.2 billion, and the investment in new or modified sludge treatment and disposal facilities was RMB 29.4 billion, and the investment in newly added reclaimed water production facilities was RMB 15.8 billion. During the ¡§13th Five-Year Plan¡¨ period, the investment in construction of cleaning the black and odorous water body at the prefecture level and above was about 170 billion yuan, which has been included in the planned key construction task investment.

The water industry is less concentrated and the market capacity is still expanding

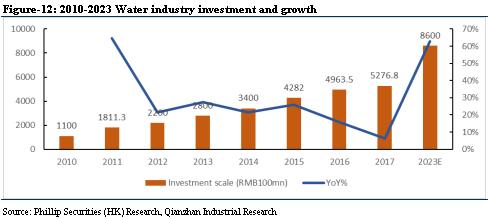

According to research by the Qianzhan Industrial Research, there are more than 4,000 waterworks in China, more than 3,500 sewage treatment plants, and many water companies. However, the industry concentration is quite low: the operating scale market share of CR5 is 11%, and CR10 is 16.5%, and the market concentration in the water distribution is relatively low. In the sewage treatment industry, the market share of CR5 wastewater treatment enterprises is 19%, and the market share of CR10 is 27.2%. Compared with the water distribution market, the concentration of the sewage treatment market is relatively high. Excessive market fragmentation restricts the technological progress of the water industry and the intensification of services. It is expected that the industry leaders will carry out more mergers and acquisitions in the future, break the technical and geographical restrictions and form a competitive landscape dominated by several major water groups through the expansion.

As a weak cyclical industry, the water industry is highly correlated with factors such as economic growth level, population size and urbanization process. In recent years, the regulatory requirements for industry have been continuously strengthened, and the fields of black-odorous water treatment, construction of sponge cities, and township sewage treatment have grown rapidly. Overall, the scale of investment in the water industry has continued to increase, and there still have space for development in market capacity. According to Qianzhan Industrial Research, the annual growth rate of investment in the water industry during the ¡§Twelfth Five-Year Plan¡¨ period was 24%. It is estimated that by 2023, the annual investment amount of water industry in China will exceed RMB860 billion.

Company Analysis

Company Profile

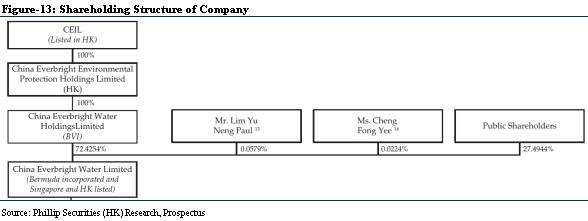

The company is an environmental protection company focusing on water environment management. It is listed on the Mainboard of Singapore Exchange Securities Trading Limited and the Main Board of The Stock Exchange of Hong Kong Limited (stock codes: U9E.SG & 1857.HK) with its direct controlling shareholder being China Everbright International Limited (stock code: 257.HK). According to Frost & Sullivan, the company is the largest Central State-Owned Enterprise operating in the wastewater treatment industry in China, as well as the third largest wastewater treatment service provider in the Bohai Economic Rim in terms of treatment capacity in 2017. The company is also one of the top ten integrated water resources solutions providers in China in terms of 2017 market share, and one of only three companies in China that is ranked top ten in both municipal wastewater treatment market and water environment management market in terms of market share. The company is listed on the Mainboard of SGX-ST and recognized by international stock market index providers, being a constituent of both the MSCI (China Small Cap Index).

The company is one of the leading water environment management enterprises in China. It is principally engaged in water environment treatment, sponge city construction, river-basin ecological restoration, water supply, waste water treatment, reusable water, waste water source heat pump, sludge treatment and disposal, research and development of water technologies, and engineering and construction, etc. The company's geographical footprint spans across East, Central, South, North, Northeast and Northwest China, including Beijing, Jiangsu, Zhejiang, Shandong, Shaanxi, Henan, Hubei, Guangxi Zhuang Autonomous Region, Liaoning and Inner Mongolia Autonomous Region.

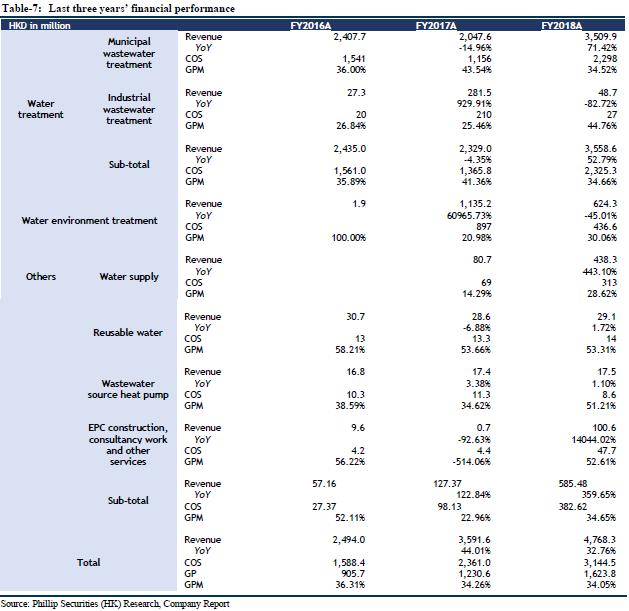

As at 30 June 2019, the revenue of the company was HKD2.485 billion, with a YoY increase of 5%; gross profit was HKD920 million, an increase of 17% YoY; net profit contributed to owners was HKD420 million, an increase of 13% YoY. The revenue and net profit of the company increased from HKD2,494.0 million and HKD372.6 million, respectively, for 2016 to HKD4,768.3 million and HKD736.8 million, respectively, for 2018, representing a CAGR of 38.3% and 40.6%, respectively.

Key Business Analysis

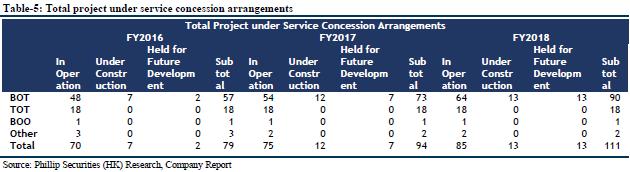

The company is a leading integrated water environmental solutions provider in China, providing a comprehensive range of environmental water services. The business spans wastewater treatment, water environment treatment, integrated utilization of water resources and water ecological protection. As at the end of 2018, the company had a scalable project portfolio of an aggregate of 94 wastewater treatment projects, 6 water environment treatment projects and 11 other projects in operation, under construction and held for future development.

1. Wastewater treatment services

The company focuses on the treatment of municipal wastewater and industrial wastewater. As at the end of 2018, the company had 79 wastewater treatment projects in operation under service concession arrangements, with a total designed capacity of 3,875,000 tonnes/day. Wastewater treatment projects comprise municipal wastewater treatment projects and industrial wastewater treatment projects. In municipal wastewater projects, the company engages in the design, construction and/or operation of wastewater treatment plants under service concession arrangements with local governments. Municipal wastewater treatment plants treat and discharge municipal wastewater in compliance with the ¡§Discharge Standard of Pollutants for Municipal Wastewater Treatment Plant¡¨ (GB18918-2002) as well as other relevant requirements stated in the environmental impact assessment reports approved by the relevant government authorities in China. The company charges customers, who are primarily local governments in China, wastewater treatment fees, mainly based on the volume of discharged wastewater and the agreed tariff during the relevant concession period, in accordance with the terms of the relevant service concession arrangements. For most of the municipal wastewater treatment projects, the service concession agreements set out a guaranteed minimum volume of wastewater to be treated and a guaranteed minimum unit price. In industrial wastewater treatment projects, the company generally provide industrial wastewater treatment services to industrial parks. The company also undertakes sludge treatment and disposal projects, which treat sludge, a by-product of the wastewater treatment process. The company mainly developed and, operated wastewater treatment projects through the BOT and TOT project models. According to Frost & Sullivan, in 2017 the company ranked fifth in China's municipal wastewater treatment market, in terms of treatment capacity.

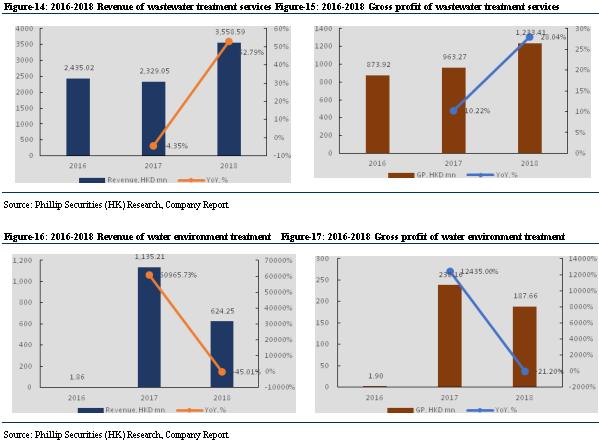

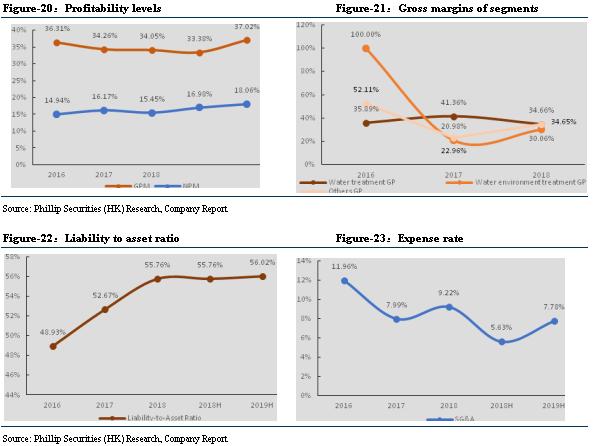

The company mainly developed and operated wastewater treatment projects through the BOT and TOT project models. For the years ended December 31, 2016, 2017 and 2018, the wastewater treatment line of business accounted for 97.6%, 64.9% and 74.7%, respectively, of the revenue and 96.5%, 78.3% and 75.9%, respectively, of gross profit.

2. Water environment treatment services

The company engages in the design, construction and operation of water environment treatment projects, which involve black-odor river treatment, watershed management, sponge city construction and a series of ecological restoration works, under service concession arrangements with the local governments in China. As at the end of 2018, the company had 2 water environment treatment projects under construction, of which the expected total designed capacity is 240,000 tonnes/day. Under these projects, the company provides a number of different services such as wastewater treatment projects, rainwater pump stations, drainage networks and rainwater storage facilities, and the company performs various types of operation and maintenance works such as source pollution control of waste vents along the river, river dredging, river widening, river training, river water ecology remediation, river water quality improvement, riverbank greening and riverside environmental management. The company charges customers, who are primarily local governments in China, service fees based on a combination of factors, including the extent to which the facility meets the relevant contractual requirements and its expected return. The company had developed and constructed water environment treatment projects through the BOT project model.

The company had developed and constructed water environment treatment projects through the BOT project model. For the years ended December 31, 2016, 2017 and 2018, water environment treatment projects accounted for 0.1%, 31.6% and 13.1%, respectively, of the revenue, and 0.2%, 19.4% and 11.5% respectively, of gross profit.

3. Others

The company also engages in the design, construction, operation and maintenance, where applicable, of (i) water supply projects, which include replenishment of reservoirs, water plant construction and water supply, urban-rural water supply, reservoir construction and water supply pipeline network construction, (ii) reusable water projects, which utilize the water processed by wastewater treatment plants for water resources recycling for power plants or produce ultra-pure water from power plants for industrial recycling and (iii) wastewater source heat pump projects, which extract low-grade thermal energy from the water discharged by wastewater treatment plants to power heating and air-conditioning in winter and summer for buildings for energy conservation and environmental protection. The company undertakes these projects under service concession arrangements with the local governments in China. As at the end of 2018, the company had 6 other projects, comprising 4 reusable water projects and 2 wastewater heat source pump projects, respectively, in operation, with a total designed capacity of 81,600 tonnes/day. The company developed and operated these projects through the BOT, BOO and self-operation project models.

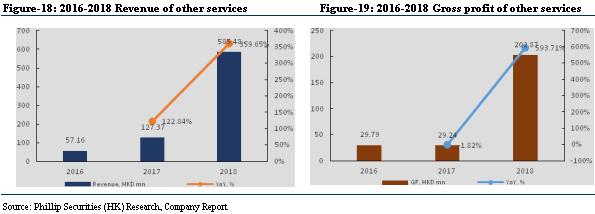

For the years ended December 31, 2016, 2017 and 2018, other projects accounted for an aggregate of 1.9%, 3.5% and 10.1%, respectively, of revenue and 2.7%, 2.6% and 9.3%, respectively, of gross profit. Other than integrated water management services, the company also provided EPC construction, consultation work and other services, which accounted for approximately 0.4%, nil and 2.1% of revenue for the years ended December 31, 2016, 2017 and 2018, respectively.

Business Model

As at the end of 2018, the company had a total of 111 projects, including 86 projects in operation, 13 projects under construction and 12 projects held for future development. For most of service concession arrangement projects, the company adopted the BOT or TOT project model according to the relevant service concession arrangements, and the company also adopted the BOO, self-operation and BT Project Models for some of projects.

-BOT model: As at December 31, 2018, under the service concession arrangement projects, the company had 68 municipal and industrial wastewater treatment projects, three water environment treatment projects, and six other projects under the BOT project model (in operation and under construction).

-TOT model: As at December 31, 2018, under the service concession arrangement projects the company had 18 municipal and industrial wastewater treatment projects under the TOT project model (including projects in operation and under construction).

-BOO model: As at December 31, 2018, the company had one reusable water project under the BOO project model in operation.

-Self-operation model: self-operation projects are largely similar to BOT or BOO projects, except that the service concession agreements do not specify whether the project shall be handed over to the relevant municipal authority or enterprise client on expiry of the terms of the contract. As at December 31, 2018, the company had two self-operation projects in operation.

-BT model: In 2016, the company adopted the BT project model for the project. As the BT project model is no longer adopted in China due to legal restrictions, the company had not adopted the BT project model for any of new projects since December 31, 2016.

Investing Highlights

Leading integrated water environmental solutions provider in the PRC with a strong project pipeline

The company is a leading integrated water environmental solutions provider in the PRC, providing a comprehensive range of environmental water services. Its business spans wastewater treatment, water environment treatment, integrated utilization of water resources and water ecological protection. According to Frost & Sullivan, the company is the largest Central State-Owned Enterprise operating in the wastewater treatment industry in the PRC, as well as the third largest wastewater treatment service provider in the Bohai Economic Rim in terms of treatment capacity in 2017. It's also one of the top 10 integrated water resources solutions providers in the PRC in terms of 2017 market share, and one of only three companies in the PRC that is ranked top ten in both the municipal wastewater treatment market and the water environment management market in terms of market share. The company's revenue and net profit increased from HK$2,494.0 million and HK$372.6 million, respectively, for 2016 to HK$4,768.3 million and HK$736.8 million, respectively, for 2018, representing a CAGR of 38.3% and 40.6%, respectively. According to Frost & Sullivan, from 2015 to 2017, the growth rates of revenue and net profit are one of the highest among all of those companies which are listed on the Hong Kong Stock Exchange with a similar business scope of providing water management solutions.

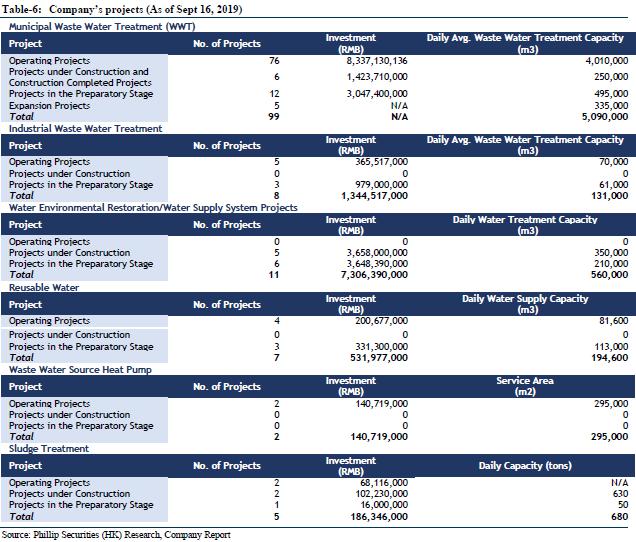

As of 1H2019, the company has implemented 121 environmental protection projects with a total water treatment capacity of over 6 million cubic meters per day, involving a total investment of approximately RMB 22.416 billion. The projects are located in 10 provinces, municipalities and autonomous regions such as Beijing, Shandong, Jiangsu, Shaanxi, Liaoning, Inner Mongolia, Henan, Hubei, Guangxi and Zhejiang, covering more than 40 districts and counties. Among them, 91 projects were completed and put into operation, involving a total investment of about RMB 11.579 billion; one completed project involving an investment of about RMB 38 million; 8 projects under construction involving a total investment of about RMB 3.525 billion; 21 preparatory projects involving a total investment of RMB 7.274 billion. In addition, the company also undertakes 2 EPC projects and 1 commissioned operation project with a total contract value of approximately RMB 146 million. In terms of market expansion, while consolidating its market position in Shandong, Jiangsu, Hubei and Liaoning provinces, the company expanded to the environmental protection market in Zhejiang Province and obtained the first drinking water source wetland project.

As of 1H2019, the company obtained 11 environmental protection projects and signed one supplementary agreement for an existing project involving an investment of RMB 3.674 billion. These include 6 sewage treatment projects, 3 water reuse projects, 1 water supply project, 1 sewage pipe network project, and 1 supplementary agreement for existing project. At the same time, the company undertakes 2 EPC projects and 1 commissioned operation project, involving contract amount of about RMB 146 million. The newly added daily sewage treatment capacity was 405,000 cubic meters, the newly added daily water supply capacity was 85,000 cubic meters, the newly added daily water supply capacity was 600,000 cubic meters, and the newly added daily sludge treatment and disposal capacity was 200 tons.

Strong potential for organic growth as well as expansion through acquisitions as supported by ¡§Everbright¡¨ brand

The company's controlling shareholder, CEIL, is a market leader in the environmental protection industry in China. The parent company of CEIL, China Everbright Group, is a large-scale conglomerate among the Fortune Global 500 and has a well- recognized brand image. China Everbright Group has a diversified business portfolio covering banking, securities, insurance, funds, finance leasing and industries, and has an outstanding track record for its business performance with a national presence. As a member of China Everbright Group, the company has benefited from the reputation, business network and the strong track record of China Everbright Group and CEIL, and has been able to grow in the environmental protection service industry. In expansion, the company will continue to focus expansion on areas where China Everbright Group has an existing presence and the ¡§Everbright¡¨ brand has been well recognized by the local governments, as well as in areas with better economic development and higher per capita income that the company has not yet established a presence in. The company believes that it is able to offer a range of environmental services to the local governments and customers by working alongside other members of China Everbright Group, which creates synergy between the company and the other members of the China Everbright Group.

The company achieves growth through three major ways: (i) obtaining new projects from local governments; (ii) project enhancement and expansion and (iii) acquisitions. In 2014, the company's shares were listed on the SGX-ST through the acquisition of HanKore by way of a reverse takeover, which involved the acquisition of 17 existing projects with an aggregate designed wastewater treatment capacity of approximately 795,000 tonnes/day and the further addition of seven new projects after the acquisition. In 2015, the company acquired 90% of the equity interests in Dalian Dongda, which boosted aggregate designed wastewater treatment capacity by approximately 835,000 tonnes/day and elevated market position. In addition, the company has also established a technology center, which focuses on the research of applied technologies and acquired the Xuzhou Design Institute in June 2018 which focuses on the survey, mapping, design and consultation of projects relating to roads, bridges, tunnels, water supply, drainage, heat, gas, electricity, construction, landscape, sanitation, highways and water conservancy, as well as the consultation of project costs, review of construction drawings, bidding agency and project management. Upon completion of the acquisition of the Xuzhou Design Institute, it was integrated into the technology center, which is now the Technology and Design Center. Further, in February 2018, in order to enhance research and development capabilities, the company together with RBH Reinhold Brenner Holding GmbH, an environment protection company in Germany which has a number of key water technologies and rich industry resources in the water industry, incorporated E+B Umwelttechnik GmbH, which will focus on the research and development of technologies relating to the design, construction and management of municipal and industrial wastewater treatment projects, sludge treatment projects, desalination projects, including the third generation biological aerated filter, SL inclined-tube sedimentation tank, membrane fouling, etc.

In the future, the company will continue to consolidate its position in the Bohai Rim Economic Circle and the Yangtze River Delta, and expand its services to other economically developed regions such as Guangdong, Hong Kong, Macao Districts, the Pearl River Delta and its surrounding suburbs and rural areas. The company will use its own integration capabilities and actively explore new opportunities such as sponge cities, watershed ecological restoration, industrial wastewater treatment, water reuse and sewage source heat pumps, and seek business expansion. In addition, relying on the company's strong R&D capabilities and technology reserves, the company will strive to develop ¡§light assets¡¨ business models such as project planning and design, engineering consulting, technical services and commissioned operations management, and strive to become an important growth point in the water environment comprehensive management business.

Financial Forecast and Valuation

Financial Performance

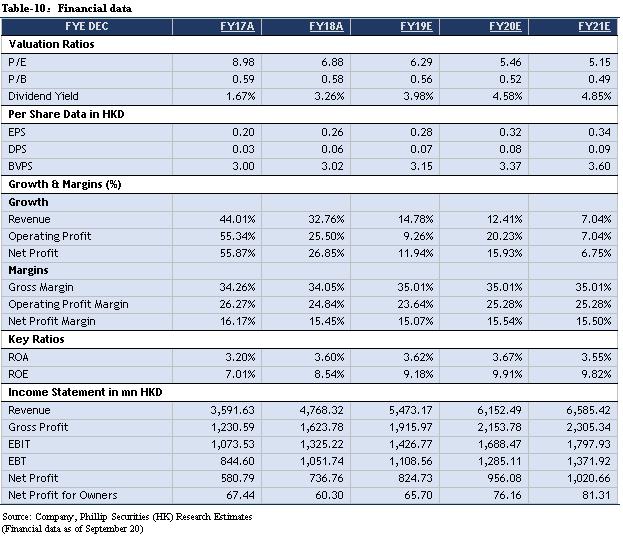

The company's revenue in 1H2019 was HKD 2.485 billion, representing an increase of 5.29% YoY; gross profit was HKD 0.92 billion, increasing by 16.76% YoY; gross profit margin was 37.02%, showing an increase of 3.64pts; net profits attributable to shareholders was HKD 0.42 billion, increasing by 13.42% YoY. From the historical data, the company's profitability level maintained a relatively steady growth. The gross profit margin increased from 33.38% in 1H2018 to 37.02% in 1H2019, which is mainly due to the increases of water treatment price and gross margin of construction services.

Financial Forecast

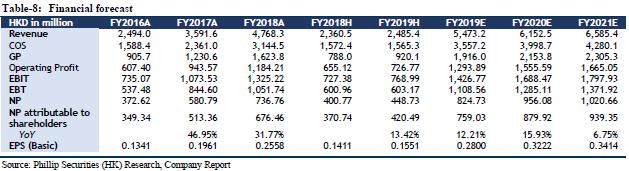

It is estimated that the company's revenue in FY19/FY20/FY21 will be HKD 5.47/6.15/6.59 billion, representing increases of 14.78%/12.41%/7.04% YoY; gross profit will be HKD 1.92/2.15/2.31 billion, representing increases of 17.99%/12.41%/7.04% YoY; net profit attributable to shareholders will be HKD 0.76/0.88/0.94 billion, representing increases of 12.21%/15.93%/6.75% YoY; corresponding EPSs are HKD 0.28/0.32/0.34. As the leading water environmental treatment company, the company's capacity is growing steadily, we are optimistic about the future development of the company.

Valuation

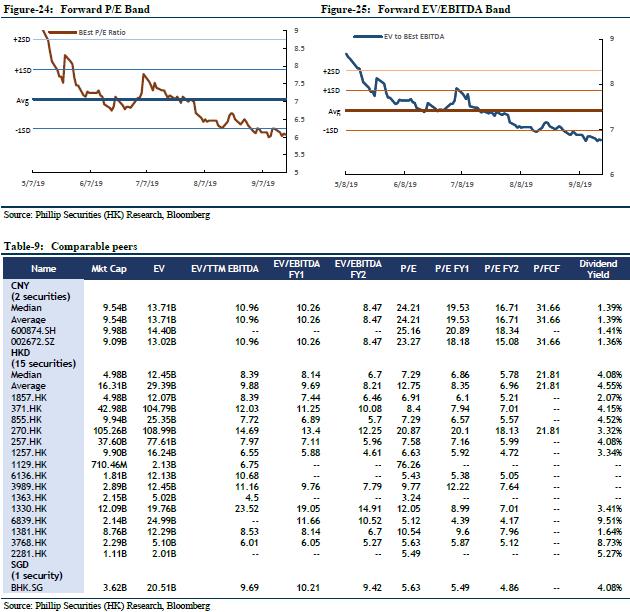

Based on our residual income valuation model, assuming the cost of equity is 6.01% and resistance factor is 0.2, we give a TP of HKD 2.64, corresponding to FY19/FY20/FY21 9.42x/8.18x/7.72x PER with a 49.79% potential upside compared with CP of HKD 1.76 as of September 20, 2019. We initiate coverage on Everbright Water and recommend ¡§BUY¡¨ investment rating.

Financials

Click Here for PDF format...