|

LIFETECH SCI(1302)

Analysis¡G

LifeTech Scientific Corporation (1302) is a developer, manufacturer and marketer of advanced minimally invasive interventional medical devices for cardiovascular, peripheral vascular diseases and disorders. It has three main product lines, including structural heart diseases business, peripheral vascular diseases business and cardiac pacing and electrophysiology business. The Group recently announced that it had entered into the Capital Increase Agreement and the Shareholders Agreement with Shenzhen Xinyuan, pursuant to which Lifetech Shenzhen and Shenzhen Xinyuan have agreed to jointly increase the registered capital of the JV Company which was originally a wholly subsidiary of Lifetech Shenzhen. It is expected that the establishment of the JV Company will be conducive to accelerating research and development of bioabsorbable materials project and further broadening the product mix of the Group. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $1.59, Target Price: $1.75, Cut Loss Price: $1.49

|

Q TECH(1478)

Analysis¡G

Q Tech record a consolidated profit attributable to the Shareholders of RMB181 million for the six months ended 30 June 2019, as compared to a loss of RMB51.29 million over a year ago, due to the following factors: (i) the gross profit margin of overall products improved apparently due to a significant increase of sales volumes of camera modules and the enhancement of product mix of fingerprint recognition module products; (ii) the labour cost has improved, which was mainly attributable to the upgrading of the production automation that has gradually demonstrated results; and (iii) Newmax Technology Co., Ltd., an associated company of the Company, has significantly improved its managing situation for the period from January 2019 to April 2019 and has recorded a profit. The gross profit margin of the integrated products increased significantly compared with the same period of last year, increasing by 7pcts to 8.2% year-on-year, and the net profit margin increased by 5.2pcts to 3.6%. In the second half of the year, driven by customer demand and product structure upgrades, profit growth is expected to continue to maintain high speed.

Strategy¡G

Buy-in Price: $8.70, Target Price: $10.30, Cut Loss Price: $7.50

Tokyo Dome Corporation (9681)

Established in 1936 as Korakuen Stadium. Operates various business facilities in Tokyo Dome City, such as Tokyo Dome, LaQua, Tokyo Dome City Attractions, MEETS PORT, Yellow Building, and Tokyo Dome Hotel. Also handles the real estate business, Matsudo Velodrome, integrated resorts and the cosmetic specialty shop, ¡§shop in¡¨, etc.For 1H (Feb-Jul) preliminary figures of FY2020/1 announced on 29/8, net sales increased by 8.3% to 45.3 billion yen compared to the same period the previous year, operating income increased by 6.3% to 6.3 billion yen, and net sales increased by 10.3% to 4.6 billion yen. Sales related to baseball such as the MLB opening game, etc. and sales of products related to concert events are favourable. Gain on sale of fixed assets and investment securities have also contributed.Company has revised their full year plan upwards on 29/8. Net sales is expected to increase by 3.6% to 90.2 billion yen compared to the previous year (original plan: 89 billion yen), operating income to increase by 6.3% to 12.2 billion yen (original plan: 11.5 billion yen), and net sales to increase by 2.0% to 7.1 billion yen (original plan: 6 billion yen). Although a profit decrease was predicted in the original plan, prospects have been reversed to a profit increase. The 1H announcement is scheduled for 11/9.

|

|

|

CHINA WATER AFFAIRS (855.HK) - Kangda's Reforms Have Seen Initial Results, Synergy Effects Need Time to Reflect

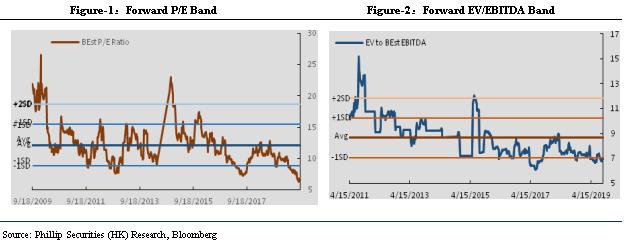

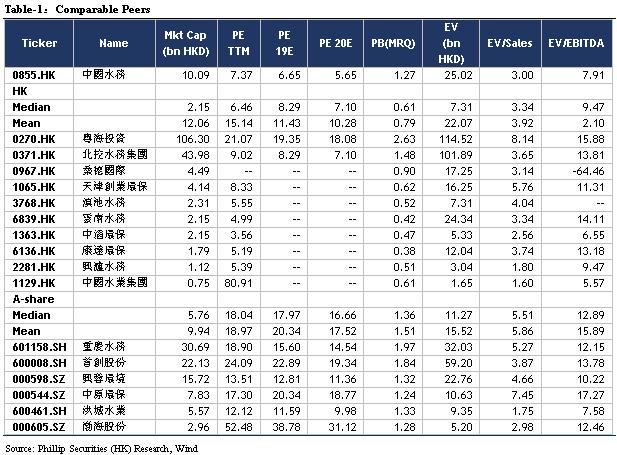

Event UpdateOn April 3, 2019, CWA spent HKD 1.2 billion to acquire a 29.52% stake in Kangda International. Upon completion of the acquisition, CWA will nominate 4 and 1 candidates respectively to serve as executive directors and independent non-executive directors of Kangda International, which holds the majority of the board of directors of Kangda International, and CWA will become the single largest shareholder of Kangda International. Kangda International will be accounted as an associate company of CWA. Kangda International is mainly engaged in Urban Water Treatment, followed by the Water Environment Comprehensive Remediation and the Rural Water Improvement. As at 1H2019, the company had entered into a total of 108 service concession arrangements projects, including 100 wastewater treatment plants, 3 water distribution plants, 3 sludge treatment plants and 2 reclaimed water treatment plant, amounting to a total designed daily treatment capacity of 4,243,350 tonnes, which comprised daily wastewater treatment services capacity of 3,966,500 tonnes, daily water distribution services capacity of 211,300 tonnes, daily reclaimed water treatment services capacity of 65,000 tonnes and daily sludge treatment services capacity of 550 tonnes. The projects spread over Shandong, Henan, Heilongjiang, Zhejiang, Anhui, Guangdong, Shanxi, Jiangsu and other provinces/municipalities in the PRC. For 1H2019, the annualized utilization rate for wastewater and reclaimed water treatment plants in operation was approximately 85% (1H2018: 85%). The actual average water treatment tariff for 1H2019 was approximately RMB1.46 per tonne (1H2018: approximately RMB1.39 per tonne). For 1H2019, construction revenue was recognized for 27 projects, including 22 wastewater treatment plants, 2 water distribution plants, and 3 sludge treatment plants. For 1H2019, the company recorded a revenue of RMB1,412.6 million, representing a decrease of approximately 12% as compared to the previous corresponding period of RMB1,607.5 million. The decrease was mainly due to the decrease in construction revenue of RMB251.5 million caused by the partial completion of the company's EPC projects. Total operation revenue of the company's Urban Water Treatment services recorded for 1H2019 was RMB433.7 million, representing an increase of approximately 7%. Total construction revenue for urban water treatment services was RMB574.4 million, representing a YoY increase of approximately 5%. Total revenue of water environmental comprehensive remediation was RMB72.6 million, representing a YoY decrease of approximately 79%. Gross profit was RMB595.3 million, representing an increase of approximately 7%. Gross profit margin was approximately 42%, representing an increase of 7 percentage points, the increase was mainly due to the higher construction margin recognized when the EPC projects finished and the increase in the proportion of financial income. Profit attributable to owners of the parent was RMB183.6 million, basically the same with the corresponding period last year. The company's selling and distribution expenses for 1H2019 was RMB3.4million, representing a climb decrease of approximately 56% as compared to RMB7.8 million of the previous corresponding period, which was a result of stringent management and cost control. Administrative expenses for 1H2019 was RMB120.3 million, representing a decrease of approximately 16% as compared to the previous corresponding period of RMB143.0 million. The decrease was mainly due to the decrease in staff costs and traveling and entertainment expenses which was caused by the stringent management and cost control. Kangda's Reforms Have Seen Initial Results, Synergy Effects Will Gradually ReflectIn the 2019 Interim Results meeting, Kangda International Management stated that they will integrate the company's resources, focus on the core business municipal sewage treatment business, and tighten the water environment comprehensive remediation business, and the 1H2019 company's municipal sewage revenue accounted for 92.3%. And they will streamline the company level, flatten the management structure, improve the company's operational efficiency, the company's 2Q2019 salary and benefits fell by RMB 11 million, travel and hospitality reduced by RMB 8.5 million, management cost fell by RMB 7.5 million. They will also optimize asset structure, revitalize inefficient assets, sell the equity-type assets, and increase the recovery of the corresponding collections. It is estimated that approximately RMB 400 million will be recovered for the subsequent capital expenditures. In addition, the company's operating income occupation increased by 10 percentage points to 51.9%, for the first time it exceeds 50%, and the income structure is more stable. In 1H2019, it completed the price increase of 5 projects, with a total scale of 440,000 tons per day, and another 8 projects are pending. The company's actual total treatment capacity of urban water services in 1H2019 was 496.4 million tons. At the end of 2019, the newly added operation is estimated to be 665,000 tons per day, based on the yield of 65% (the average yield of 1H2019 was 85%), 1H2020 newly added treatment capacity is expected to be 77.8 million tons, totaling approximately 572 million tons. The company expects a revenue of RMB 3 billion in 2019 and capital expenditures of RMB 1.15 billion. We believe that, on the one hand, Kangda International could maintain a net profit same with last year on the basis of a 12% decline in revenue, and refinanced more than RMB 2 billion through CWA's financing network, reflecting the continuous improvement of the company's performance and increasing communications with CWA. However, at present, there is only partial synergy between the two sides, and more potential synergy remains to be released. With the further strengthening of the reforms of Kangda, we believe that more synergies will gradually be reflected. And on the other hand, CWA will further promote the integration of water supply and drainage through Kangda International, expand the project coverage area, and the regional influence of coincident areas will be further enhanced. The construction of urban-rural water supply integration will be further strengthened, and the market's worries about CWA will gradually fade away. Re-affirm ¡§BUY¡¨ Investing RatingWe adjust the TP of HKD 10.33, corresponding to FY20/FY21/FY22 11.58x/10.22x/9.18x PE with a +64.76% potential upside compared with CP of HKD 6.27 as of September 13, 2019, we maintain ¡§BUY¡¨ investment rating.

Risk1. Capacity increase fail expectations; 2. Industry policy; 3. M&A fails expectations. �Financials

Click Here for PDF format...

| Recommendation on 17-9-2019 | | Recommendation | BUY | | Price on Recommendation Date | $ 6.270 | | Suggested purchase price | N/A | | Target Price | $ 10.330 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|