|

|

SHINEWAY PHARM(2877)

Analysis¡G

For 1H2019, the company recorded a revenue of RMB1,368,280,000, an increase of 4.8% YoY, gross profit margin was 71.3% as compared to 71.2% of 1H2018 and profit for the period amounted to RMB287,656,000, an increase of 11.9% YoY. Earnings per share amounted to RMB36 cents, an increase of 16.1% YoY. The pandemic outbreak of flu in last year`s winter pushed up the comparative base sales figures of last year`s first quarter of anti-influenza drugs of the company, such as Qing Kai Ling Injection and Qing Kai Ling Soft Capsule, to a relatively high level. In addition, the company had commenced to adjust the product management and sales strategies for retail pharmacy products in the first quarter of this year and at the same time reduced channel inventory, leading to declining sales of certain retail pharmacy store products. At the same time, production and shipment for Huamoyan Granule were still cut back for strategic reasons. The aforementioned matters caused negative growth to the company`s overall turnover of the first quarter of this year. Nonetheless, overall turnover had returned to positive growth for the second quarter. For 1H2019, the company`s turnover increased by 4.8% and the increase was mainly attributable to the soft capsules products and Traditional Chinese Medicine (¡§TCM¡¨) Formula Granules.

Strategy¡G

Buy-in Price: $7.50, Target Price: $10.00, Cut Loss Price: $6.40

Sosei Group Corporation (4565)

Established in 1990 as a biomedicine corporation. Carries out the research and development of medicine that fulfills important unmet medical needs. Focuses on drug development of antibodydrugs, peptides, and new low molecules that target G protein-coupled receptors (GPCR), which are a super family of internal membrane proteins of cells and tissues in the body.For 1H (Jan-Jun) results of FY2019/12 announced on 13/8, sales revenue increased by 2.8 times to 5.056 billion yen compared to the same period the previous year, operating income and netincome both returned to profit at 731 million yen and 395 million yen respectively, with ¡¶3.753 billion yen and ¡¶3.327 billion yen respectively to compared to the same period the previous year. Contributed by the milestone profit received from AstraZeneca (AZN), Pfizer (PFE), and Norvatis (NVS).For its full year plan, research and developmental costs are expected to be 4.32-4.86 billion yen (last year: 5.38 billion yen), and cash expenditures involving general administrative expenses to be 1.62-2.16 billion yen (last year: 5.187 billion yen). Presumed exchange rate of 108 yen/USD. In 1H, clinical trials will begin for the mGlu5 antagonist. Partnership programmes such as A2a andM4, etc. have shown significant progress, and we can look forward to future developments.

|

|

|

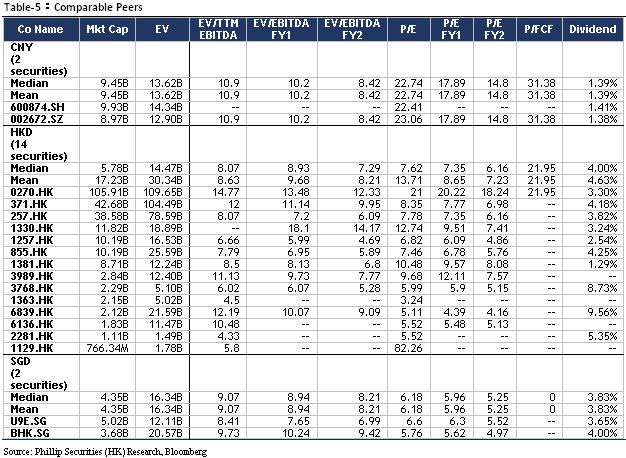

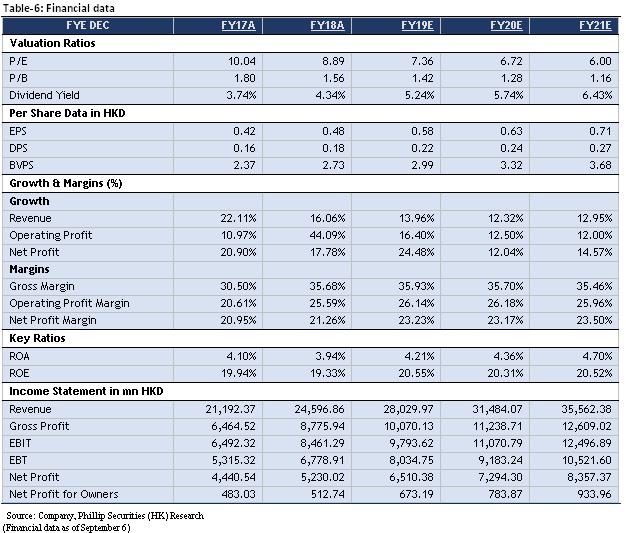

BJ ENT WATER (371.HK) - Results of 1H2019 in Line, Asset-Light Transformation is Expected

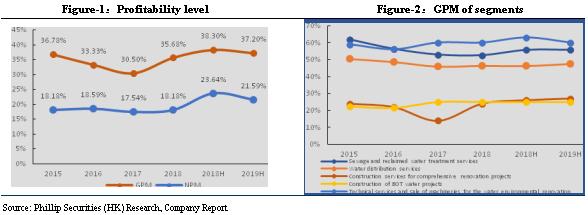

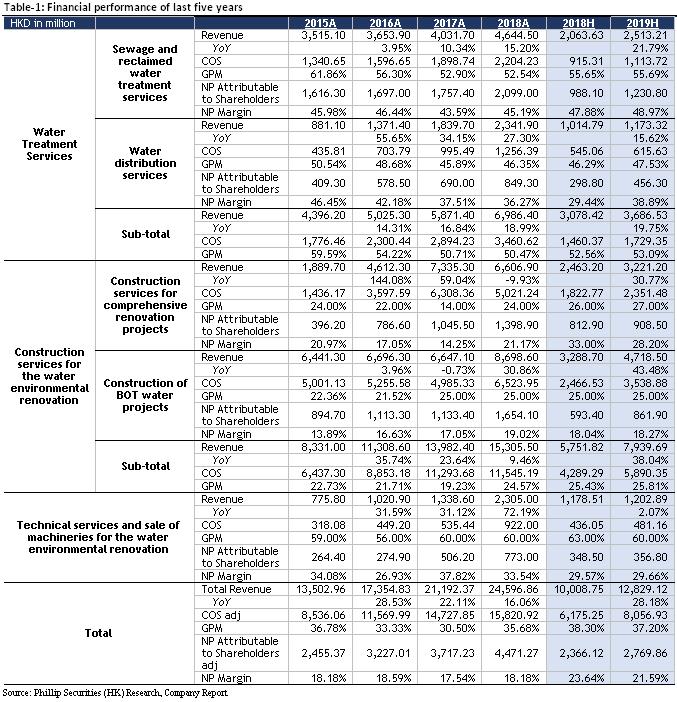

Company UpdateFor the six months ended 30 June 2019, the company's revenue was HKD 12.829 billion (corresponding period in 2018: HKD 10.009 billion), representing an increase of 28.18%. Revenue from Sewage and reclaimed water treatment services was HKD 2.513 billion (corresponding period in 2018: HKD 2.064 billion), representing an increase of 21.79%. Revenue from Water distribution services was HKD 1.173 billion (corresponding period in 2018: HKD 1.015 billion), representing an increase of 15.62%. Revenue from Construction services was HKD 7.94 billion (corresponding period in 2018: HKD 5.752 billion), representing an increase of 38.04%. Revenue from Construction services for comprehensive renovation projects was HKD 3.221 billion (corresponding period in 2018: HKD 2.463 billion), representing an increase of 30.77%. Revenue from Construction of BOT water projects for comprehensive renovation projects was HKD 4.719 billion (corresponding period in 2018: HKD 3.298 billion), representing an increase of 43.48%. Revenue from Technical services and sale of machineries for the water environmental renovation for comprehensive renovation projects was HKD 1.203 billion (corresponding period in 2018: HKD 1.179 billion), representing an increase of 2.07%. The gross profit was HKD 4.771 billion (corresponding period in 2018: HKD 3.834 billion), representing an increase of 24.49%. The GP margin was 37.10%, decreasing by 1.1 ppt compared with 1H2018, which is mainly due to the change of revenue portfolios. Profit attributable to equity holders of the company was HKD 2.77 billion (corresponding period in 2018: HKD 2.366 billion), representing an increase of 17.06%. Basic and diluted earnings per share were HK28.68 cents and 28.25 cents respectively. The interim dividend of HK10.7 cents per ordinary share for the six months ended 30 June 2019 (six months ended 30 June 2018: HK9.5 cents per ordinary share), showing an increase of 12.63%, the payout ratio is 37%, same as 1H2018. The company's performance of core business is basically consistent with our forecast, related performance increase in total revenue was mainly contributed from the increase of water treatment services and construction services for the water environmental renovation. Total daily design capacity for new projects secured for the period was 1,355,925 ton, the net increase in total daily design capacity of the period was 936,925 tons, less than the company's guidance of 4 million tons additional for the full 2019. But the company maintain the above new capacity target, believing there will be more opportunities of M&A in 2H2019. Stable growth in production capacity, waiting for high quality M&A opportunitiesAs at 30 June 2019, the company entered into service concession arrangements and entrustment agreements for a total of 1,047 water plants including 875 sewage treatment plants, 140 water distribution plants, 30 reclaimed water treatment plants and 2 seawater desalination plants. Total daily design capacity for new projects secured for the period was 1,355,925 tons including BOT projects of 130,000 tons, PPP projects of 882,925 tons, entrustment operation projects of 263,000 tons, and 80,000 tons through mergers and acquisitions. Due to different reasons such as expiration of projects, the company exited projects with aggregate daily design capacity of 419,000 tons during the period. As such, the net increase in daily design capacity of the period was 936,925 tons. As at 30 June 2019, total daily design capacity was 37,761,558 tons. The company's production capacity has maintained a compound annual growth of 35.96% since 2008. Although the progress of new projects in 1H2019 has slowed down, we are still optimistic about the company's capacity growth in 2H2019. We expect that the company will achieve the goal of adding 4 million tons of new capacity in 2019 through more M&A projects. Continue asset-light transformation, closely cooperate with the Three Gorges GroupOn January 18, 2019, the company entered into a subscription agreement with China Yangtze Power International, which has conditionally agreed to subscribe for 470,649,436 new ordinary shares. This means that the company will further deepen its partnership with China Three Gorges Corporation, to develop water environmental protection business in the Yangtze River area. In addition, the company also adheres to the ¡§dual-platform strategy¡¨ and asset-light business model. It is expected that there will be a new signed RMB 20 billion water environment renovation projects and a capital expenditure of HKD 12 billion for the whole year. The interest expense for 1H2019 has also increased 42.73% to HKD 1.193 billion, the gearing ratio dropped from 114% to 110%. However, we expect that as the company's asset-light model continues to promote, the future capital expenditure will gradually decline, and the financial situation will further improve.

Financial Forecast and ValuationWe adjust the company's revenue in FY19/FY20/FY21 to be HKD 28.0/31.5/35.6 billion, representing increases of 13.96%/12.32%/12.95% YoY; net profit attributable to shareholders will be HKD 5.6/6.3/7.2 billion, representing increases of 25.05%/12.04%/14.57% YoY; corresponding EPSs are HKD 0.58/0.63/0.71. We adjust the TP of HKD 5.83, corresponding to FY19/FY20/FY21 10.06x/9.19x/8.21x PE with a +36.76% potential upside compared with CP of HKD 4.26 as of September 6, 2019, we maintain ¡§BUY¡¨ investment rating.

Risk1. Project progress fail expectations; 2. Industry policy; 3. Interest rate; 4. M&A fails expectations. Financials

Click Here for PDF format...

| Recommendation on 10-9-2019 | | Recommendation | BUY | | Price on Recommendation Date | $ 4.260 | | Suggested purchase price | N/A | | Target Price | $ 5.830 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|