|

CONCORD NE(182)

Analysis¡G

Concord New Energy Group (182) is principally engaged in the investment and operation of wind power plants and PV power plants in China. For the six months ended 30 June 2019, the Group recorded a total income of RMB 963 million, representing 19% increase as compared to the same period of last year. Profit attributable to shareholders amounted to RMB399 million, representing 44.8% increase. Power generation output and profit of the Group were both higher than expected. The Group will continue developing and constructing quality wind power projects in the southern regions without power curtailment and also aggressively developing grid parity projects, which have better resources and stable revenue, in the northern regions. In the first half of 2019, the Group newly signed contracts for wind resources of 3,682MW and PV resources of 868MW in total, assuring construction and sustainability development of the Group`s subsequent projects. (I do not hold the above stock)

Strategy¡G

Buy-in Price: $0.37, Target Price: $0.41, Cut Loss Price: $0.35

|

COUNTRY GARDEN(2007)

Analysis¡G

In the first half of 2019, Country Garden realized operating income of 202.01 billion yuan, a year-on-year increase of 53.2%. Gross profit was 54.86 billion yuan and net profit was 23.06 billion yuan, a year-on-year increase of 56.9% and 41.3% respectively. The real estate industry in Mainland this year is more challenging than in the past, especially in the first half of the year, because the supervision has become stricter and financing has tightened. Under such a circumstance, Country Garden`s core indicators such as operating income, gross profit, and net profit have all achieved substantial growth. When revenue growth strengths, Country Garden also held 222.8 billion yuan in the first half of 2019, which realized positive net cash flow in the middle of the year for three consecutive years after 2017 and 2018. The ratio of the net cash flow to total assets reached 12.8% and reached 2 times the short-term interest-bearing liabilities. As a leading company in real estate industry, such coverage makes it unnecessary to worry about short-term debt. Continuously maintaining net operating cash flow positive indicates that Country Garden can achieve a virtuous cycle of cash through the operation itself, and dependence on external financing to support cash flow is greatly reduced.

Strategy¡G

Buy-in Price: $10.00, Target Price: $13.00, Cut Loss Price: $7.00

ETFMG Prime Mobile Payments ETF ( IPAY )

is the first and only ETF to track the performance of the mobile payment industry, with market cap of approximately USD 841.64 million and expense ratio of 0.75%. IPAY is a thematic ETF which enables investors to capitalize on the shift from credit card & cash transactions to digital & electronic. There are several factors supporting the growth of the industry. First, the penetration rate of smartphones has increased greatly over the past few years due to affordable prices for customers. With the evolving global 4G connection, thousands of smartphone users can make electronic payment conveniently. Besides, the adoption rate of mobile payments in emerging market is huge. Particularly, consumers in china embrace mobile payments at a faster rate than rest of the world According to a PWC report, the current share of Chinese Internet users making mobile digital payments is about 68 % compared to that of the US ( about 15% ). Chinese consumers appreciate the convenience from mobile payment and don`t concern its data privacy & security issue as the American consumers do. The explosive growth of global e-commerce business helps promote the use of mobile payment as well. Not only online retail, it is expected that mobile payment will increase its penetration rate towards other areas of our daily life such as financial and healthcare area. Non-commerce payment digitization also boosts the growth of digital-payment market. Electronic person to person (P2P) payments, which aren`t captured in consumer-spending data or GDP, but are surging, along with funds disbursed to consumers by governments and businesses. According to Allied Market Research, the global mobile payments market reached $601.3 billion in 2016, and is expected to reach $4,573.8 billion by 2023, registering a CAGR of 33.8% from 2017 to 2023.Entry Price: USD 47.93 Stop Loss: USD 46.01Target Price: USD 52.51

|

|

|

SINOPHARM ACCORD (000028.SZ) - Distribution Business Exceeds Expectations, Retail Stores Continue Expanding

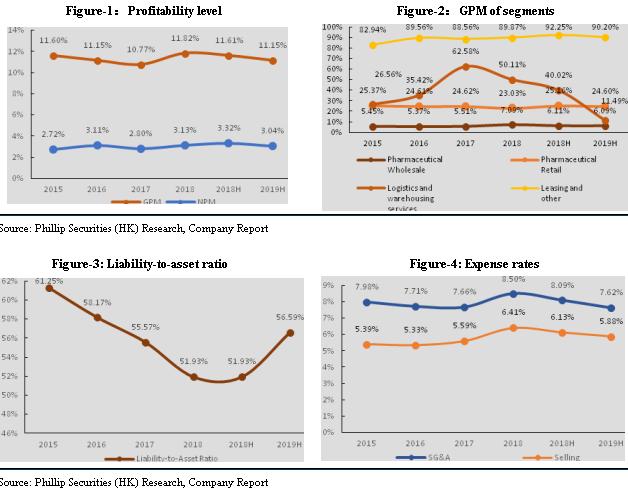

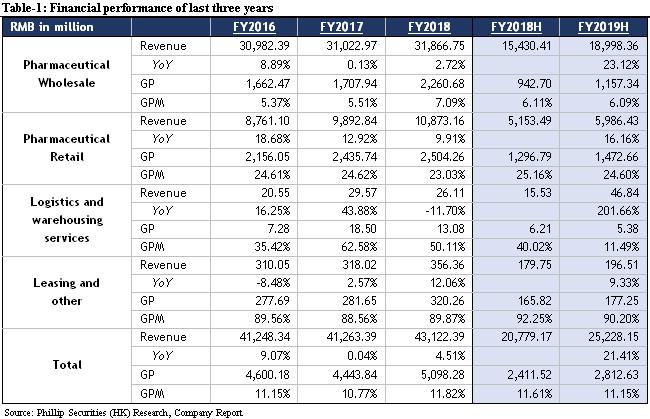

Company UpdateAs of 30 June 2019, the company's revenue was RMB 25.228 billion, representing an increase of 21.42% YoY; net profit attributable to shareholders was RMB 651 million, with a YoY increase of 1.42%. Revenue from pharmaceutical distribution business was RMB 19.477 billion, representing an increase of 22.66% YoY; segment net profit attributable to shareholders was RMB 382 million, representing an increase of 15.41% YoY. Revenue from Guoda Drugstore was RMB 6.108 billion, representing an increase of 18.75% YoY; segment net profit attributable to shareholders was RMB 150 million, representing an increase of 7.81% YoY. Basic earnings per share was RMB 1.52 (corresponding period in 2018: RMB 1.50). The company's performance of core business is basically consistent with our forecast, in the first half of 2019, the company expanded the scale, and growth rate was better than the overall level of the industry, and achieved steady and rapid growth in performance; related performance increase in total revenue was mainly contributed by the acceleration of the company resource integration and expansion of store network layout. As of the first half of 2019, the company had a total of 107 subsidiaries, and the number of retail outlets of Guoda Drugstore was 4,593, with a net increase of 318 stores, 228 of which was direct-sales shops. During the reporting period, the company invested in the establishment of the Sinopharm Guoda Drugstore Bayannao`er Co., Ltd., Inner Mongolia Guoda Pharmaceuticals Co., Ltd., and Sinopharm Guoda Drugstore Yongxingtang Chain (Chaoyang) Co., Ltd. Investment HighlightsDistribution business continues to integrate and promote the synergy of wholesale and retail In the pharmaceutical distribution field, the company continues to integrate the distribution and logisticsbusiness, deeply penetrates into the end markets, improves the multistep distribution network, creates intelligent supply chain, developed a clustered and large-scale industrial advantages, and commit to becoming a leading provider of medical health products and services in Southern China. In the first half of 2019, the distribution launched the logistics planning of wholesale and retail integration, and the sales of wholesale and retail synergies increased by 54% YoY, and the part outside of Guangdong and Guangxiprovinces increased by 64% YoY. In the first half of 2019, the hospital direct selling market distributed in 30 cities at prefecture level and above in Guangdong and Guangxi ranked the top three; the distribution of customers was mainly including retail medical treatment, grass-root medical institutions, and small-scale social medical services: 1,804 medical institutions at the first level or above, 3,783 primary care customers (excluding 836 first-level hospitals), and 1,587 retail terminal customers (chain drugstores, single tores). The company has complete pharmaceutical distribution networks in Guangdong and Guangxi, achieve comprehensive coverage of the second and third-level medical institutions in Guangdong and Guangxi, scale and growth rate have achieved rapid growth. In the first half of 2019, traditional business grew by 22% YoY, retail direct sales increased by 30% YoY, equipment consumables increased by 52% YoY, retail medical treatment increased by 80% YoY, and primary care increased by 34% YoY. Retail business's performance stably increased, store network gradually expanded In the pharmaceutical retail field, Guoda Drugstore is a pharmaceutical retail enterprise that ranks the first in the sales volume throughout the country, and is one of the few enterprises in China with national direct sales drug retail network. As of the end of June 2019, Guoda Drugstore had established 28 regional chain enterprises, had 4,593 stores, covering 19 provinces, autonomous regions, and municipalities directly under the central government, which formed a network of pharmacies covering the urban agglomerations of East China, North China, and coastal region of South China, and gradually spread into the Northwest, Central Plains, and inland city clusters; 3,470 direct-operated stores, with sales revenue of RMB 5.381 billion, a YoY growth of 11.82%; 1,123 franchise stores with distribution revenue of RMB 622 million, an increase of 7.64% YoY. The "New Concept" pilot pharmacy jointly launched by Guoda Drugstore and Walgreens Boots Alliance opened on January 20th at Shangnan Road, Pudong New District of Shanghai. Up to now, sales have increased by 34.8% YoY, and the number of transactions has increased by 31.5% YoY. In addition, Guoda Drugstore built an Internet + medical e-commerce model, improved the value-added service system, optimized the self-operated OTO platforms such as WeChat Mall and APP, created a pharmacy + Internet O2O model, enhanced the front-end customer experience, and launched the e-commerce national customer service. In the first half of 2019, the number of effective members nationwide was 11.436 million, an increase of 8% YoY. In 2019, the company promoted brand upgrade, implemented the new brand strategy, successively completed the "Guoda" upgrades and "Guozhi" brand integration plan, and continue to promote brand upgrades in the second half of the year. The leading scale of Guoda Drugstore was one of the core competitiveness, and the scale advantage reduced the company's procurement cost and enhanced the company's bargaining ability. Financial Forecast and ValuationFinancial Performance In the first half of 2019, the company realized gross profit of RMB 2.81 billion, representing an increase of 21.41% YoY as compared to RMB 2.41 billion in 2018. The increase in gross profit was mainly attributable to the increase of distribution and retail businesses. Gross profit margin of the company decreased from 11.61% in 2018 to 11.15% in 2019. The decrease was mainly due to the larger proportion of distribution business.

Financial Forecast and Valuation We adjust the company's revenue in FY19/FY20/FY21 to be RMB 50.5/55.1/60.1 billion, representing increases of 17.01%/9.11%/9.17% YoY; gross profit will be RMB 5.7/6.3/7.0 billion, representing increases of 11.89%/10.44%/10.57% YoY; net profit attributable to shareholders will be RMB 1.3/1.5/1.7 billion, representing increases of 4.59%/17.12%/16.62% YoY; corresponding EPSs are RMB2.958/3.646/4.040. Based on our residual income valuation model, we adjust a TP of RMB 54.12, corresponding to FY19/FY20/FY21 18.30x/15.62x/13.40x PE with a +13.79% potential upside compared with CP of RMB 47.56 as of August 30, 2019, we give ¡§ACCUMULATE¡¨ investment rating.

Risk1. Industry policy risk 2. Guoda Drugstore's business fails expectations 3. Distribution business transformation fails expectations Financial

Click Here for PDF format...

| Recommendation on 5-9-2019 | | Recommendation | ACCUMULATE | | Price on Recommendation Date | $ 47.560 | | Suggested purchase price | N/A | | Target Price | $ 54.120 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the ¡§Group¡¨) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products¡¦ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

ª©Åv©Ò¦³¡A ½¦L¥²¨s¡C

Copyright(C) 2019 Phillip Securities (HK) Ltd. All Rights Reserved.

|