Investment Summary

Yongyou is a leading provider of enterprise services in China, offering cloud, software and financial services. The result in first half was doing well, where the revenue grew by 10.2%, and continued its good cost control since the first quarter. Besides, the growth of revenue from cloud services remained robust, up by 114.6% YoY, and it has launched several new products, such as Yonyou Cloud Platform iuap V3.5.6, Yonyou NC Cloud 1903 and etc. We give a TP of RMB $30.64, 3.6% higher than previous TP, downgrading to ¡§Nentral¡¨ recommendation, with 7.2% potential downside. (Closing price at 27 Aug 2019)

Result update

The Group announced interim results with revenue of RMB 3.31 bn, up 10.2% YoY; net profit attributable to owners was RMB 480 mn, up 290.1% YoY; net profit attributable to shareholders to owners after deducting non-recurring gains and losses was RMB 260 mn, an YoY increase of 155.1%; net profit attributable to shareholders to owners excluding non-recurring gains and losses and equity incentive costs was RMB 320 mn, also increasing by 40.5%.

Good cost control

The Group continued its good cost control since the first quarter. Selling expense and administrative expenses as percentage of revenue accounted for 17.6% and 16.3%, respectively, down 2.2% and 2.7% YoY. However, R&D expenses as percentage of revenue increased to 22.7%, up 2.7% YoY, due mainly to the increase in the development of cloud products. In addition, gross profit margin also fell by 2.9% YoY to 66%. The overall gross profit margin fell due to the strong growth of business with lower gross profit margin.

Robust growth on Cloud; more products will be launched

The revenue from cloud service business (excluding financial cloud service business) was RMB 470 mn, a YoY increase of 114.6%. Based on the classification of enterprises, the revenue from the micro-enterprise cloud service business was RMB 45.27 million, an increase of 142.3%; revenue from the large and medium-sized enterprise cloud service realized RMB 430 mn, an increase of 112%. Based on the business model, revenue from SaaS business was RMB 290 million, an increase of 133.6%; revenue from BaaS business realized RMB 110 mn, an increase of 146.1%; revenue from PaaS busines was RMB 68.77 mn, an increase of 39.5%; revenue from DaaS business reached RMB 4.14 mn, an increase of 78.3%.

During the period, the Group released Yonyou Cloud Platform iuap V3.5.6, Yonyou NC Cloud 1903, U8 Cloud V 2.6 and U8 15.1, and also accelerated the development of Yonyou platform iuap5.0 and NC Cloud 1909. In addition, the company focused on strengthening business cooperation with strategic partners such as Huawei, China Telecom, and Industrial and Commercial Bank of China. The cloud market has grown steadily, in whcih its partners have exceeded 4,000, and its products and services have exceeded 6,200. Besides, the Group, together with China Software Association and Huawei, China Power Ke Puhua, Shanghai Zhaoxin, Loongson Zhongke, 360 Enterprise Security and other well-known domestic manufacturers, jointly launched the ¡§Enterprise Digital Self-Controlled Service Alliance¡¨ and actively promoted the enterprise digitalization and localization.

Valuation

Based on the net profit attributable to the owner in 2020, we derive a TP of RMB $30.64, 3.6% higher than the previous TP, reflecting a 75x P/E in light of the rapid growth in cloud services. Although increase in research and development on cloud services may reduce the net profit margin in the short term, but it is expected to create a long-term competitive advantage. Although we are positive on long term development, since the sharp rise in share prices recently, we have downgraded to the ¡§Neutral¡¨ rating, with a potential downside of 7.2%.

Risk

1. Slower-than-expected growth in cloud products

2. The economy of China slows down

3. Cloud ERP may take away the existing customers of traditional ERP, particularly SME

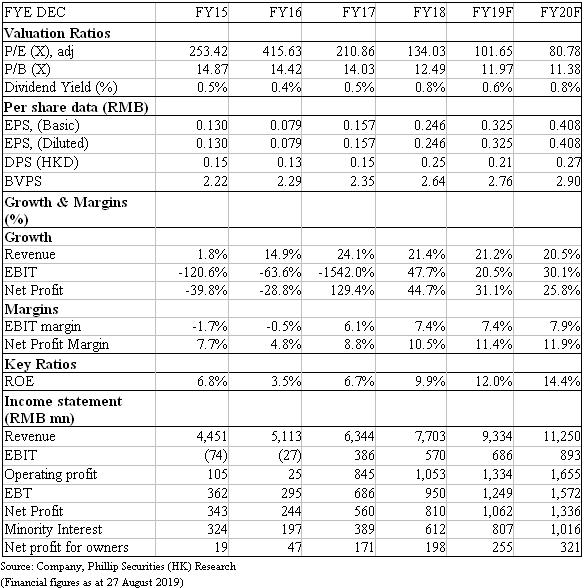

Financials

Click Here for PDF format...